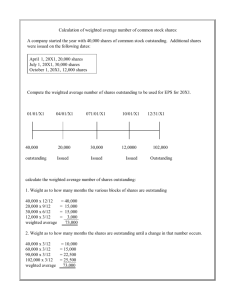

Ch16

advertisement