A. Standard Costs are

advertisement

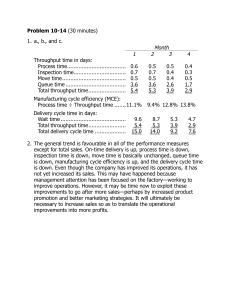

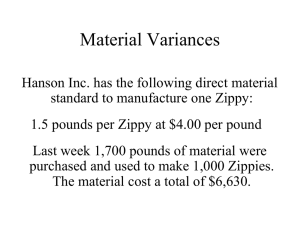

Dr. Bob’s 256 Notes, 11-1 CHAPTER 11 STANDARD COSTS AND OPERATING PERFORMANCE MEASURES I. OBJECTIVES Overview of how standard costing systems are established and used Standard cost variance analysis for materials and labor Overview of how operating performance measures are used II. OVERVIEW OF STANDARD COSTS: A. Standard Costs are … Based on carefully predetermined amounts Used for planning labor, material, and overhead requirements The expected level of performance Benchmarks for measuring performance B. Focus is on quantities and costs that exceed established standards, a practice known as… C. Advantages Possible reductions in production costs Better information for planning and decision making Disadvantages Emphasis on negative exceptions may impact morale, lead to cover ups Focus on big variances may obscure early stages of trends D. Setting Standard Costs In General… _______________ Standards based on perfect conditions (e.g., machines never break down) really not attainable _______________ Standards levels that are currently attainable, but high enough to encourage efficient and effective operations Dr. Bob’s 256 Notes, 11-2 Specific Standard-Setting Materials Standards Price – Use competitive bids for the quality and quantity desired Quantity – Use product design specifications So, the standard material cost for one unit of product is: Labor Standards Rate – Use wage surveys and labor contracts Time – Use time and motion studies for each labor operation So, the standard labor cost for one unit of product is: Variable Overhead Standards We’re not covering Overhead Variance in this course; however it’s not really different from the above discussion (just more involved in the calculations). Standard Cost Card might look something like this: Inputs Direct Materials Direct Labor Variable Mfg. Overhead Total Standard Unit Cost Standard Quantity or Hours 3.0 lbs. 2.5 hrs. 2.5 hrs. Standard Price or Rate $ 4.00 per lb. 14.00 per hr. 3.00 per hr. What’s the difference between a Standard and a Budget ___________________ is the expected cost for one unit. ___________________ is the expected cost for all units. Standard Cost $12.00 35.00 .50 $54.50 Dr. Bob’s 256 Notes, 11-3 III. Standard Cost Variance Analysis Standard Cost Variances Price Variance Quantity Variance A General Model for Variance Analysis Actual Quantity x Actual Price Actual Quantity x Standard Price Standard Quantity x Standard Price Dr. Bob’s 256 Notes, 11-4 Demo Problem: Let’s use the General Model to compute the Materials and Labor Variances for Hansen Company. Materials Variances: Hanson Inc. has the following direct material standard to manufacture one Zippy: 1.5 pounds per Zippy at $4.00 per pound Last week, 1,700 pounds of material were purchased and used to make 1,000 Zippies. The material cost a total of $6,630. What is the actual price per pound paid for the material? What is the standard quantity of material that should have been used to produce 1,000 Zippies? Actual Quantity x Actual Price Actual Quantity x Standard Price Standard Quantity x Standard Price An Issue Regarding Standard Cost Variance Analysis for Materials: Suppose in the Demo Problem that Hanson had purchased 2,800 pounds of material for a total cost of $10,920; but used only 1,700 pounds in making the 1,000 Zippies. How do the Variances change? Price Variance Quantity Variance Dr. Bob’s 256 Notes, 11-5 Info for Labor Variances: Hanson has the following direct labor standard to manufacture one Zippy: 1.5 standard hours per Zippy at $6.00 per direct labor hour Last week 1,550 direct labor hours were worked at a total labor cost of $9,610 to make 1,000 Zippies. What was Hanson’s actual rate for labor for the week? What is the amount of standard labor hours that should have been worked to produce 1,000 Zippies? Actual Hours x Actual Rate Actual Hours x Standard Rate Standard Hours x Standard Rate Dr. Bob’s 256 Notes, 11-6 IV. OPERATIONAL PERFORMANCE MEASURES Demo Problem – Delivery Performance Measures: Smith Company recorded the following average times for each order received and processed: Wait time to start production 6.0 days Inspection time 0.5 days Process time 2.0 days Move time 0.2 days Queue time 4.0 days Delivery Cycle and Throughput Time: Customer’s Order Received Production Started Wait Time Goods Shipped Process Time + Inspection Time + Move Time + Queue Time Throughput Time (Manufacturing Cycle Time) Delivery Cycle Time Value-Added Time Non-Value-Added Time Key Measures of Delivery Performance: Percentage of on-time deliveries Throughput time (aka manufacturing cycle time, or the velocity of production) Measured by the Manufacturing Cycle Efficiency (MCE): MCE = Value-Added Time = Process Time Throughput Time Throughput Time Delivery cycle time = Wait Time + Throughput Time