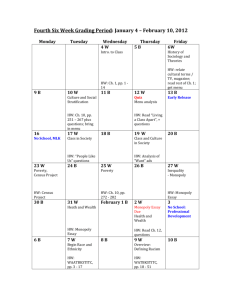

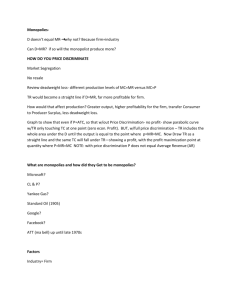

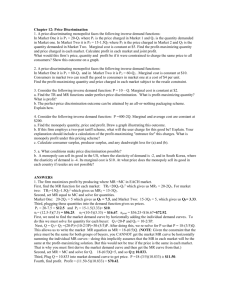

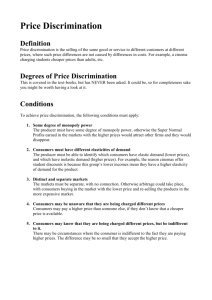

Monopoly

advertisement