A Notice Regarding the Biggert-Waters Flood Insurance Reform Act

advertisement

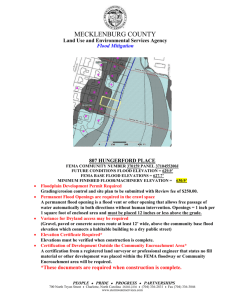

A Notice Regarding the Biggert-Waters Flood Insurance Reform Act of 2012 In July 2012, Congress made a number of changes to the National Flood Insurance Program that is administered by FEMA. There is a great deal of confusion on how this will affect different properties and when the effect will be felt as the changes are being implemented over time. ARE YOU AFFECTED? 1. Is the house you are concerned about a second home built before 1985? If yes, then the flood premium will go up 25% per year until the premium is at the level that FEMA would require of that house at full FEMA rates. If the home is above the required based flood elevation there would be no negative pricing impact. The pricing changes will affect homes that are below the base flood elevation for your zone. You need an elevation certificate to be able to evaluate how this affects you. This was effective Jan 1, 2013. 2. Commercial properties built before 1985 will have their premiums based on the required base flood elevation for that commercial property. No elevation certificate? You will need to have one done. You will no longer have subsidized pricing based on the premium rules for buildings built before 1985. Premiums will go up 25% per year until full FEMA rates are reached. THIS IS EFFECTIVE 10/1/2013. 3. What happens if they redraw the flood maps and I have a higher base flood elevation in the redrawn maps? Am I still grandfathered to the old elevation requirement and respective premium? NO. The act would cause your premium to be based on the new elevation requirement. If you were in a 13 foot zone and the redrawn map puts you in a 14 foot zone: you will pay more premium at an increase of 20% per year over 5 years. THIS IS EFFECTIVE LATE 2014. 4. My house was built before 1985 and it is my primary residence. How am I affected by the changes? Your premium will remain subsidized as long as you own the house and you will see normal premium increases based on overall flood premium changes. 5. I am planning to buy a house that was built before 1985. How will the Flood Act changes affect me? Is there an elevation certificate? Without one there is no way to know. The law, as it is now written, will require you to obtain an elevation certificate within one year of October 2013 and at that time your flood premium will be based on the elevation certificate. THIS TAKES EFFECT 10/1/2013 ON PROPERTY PURCHASED AFTER JULY 2012. 6. But the seller of a pre-1985 home has subsidized rates. Are you saying that I will not get the same subsidized pricing? The law now says that the buyer will not get subsidized pricing and has a one-year provisional premium to allow time for the buyer to furnish an elevation certificate at which time his premium will be at full FEMA rates. 7. Can you give me an example? It takes an elevation certificate to truly answer this question. But assume that the home you buy is in an AE15 which would require the base elevation to be 15 feet. You obtain an elevation certificate and learn the home sits at 11 feet or 4 feet below the required elevation. The flood premium would be about 8 times more than the seller who had subsidized pricing would have been paying. In dollars this would mean that a $2,000 subsidized premium paid by the seller would be about $15,000 to the buyer at the end of the one year provisional period. 8. Will Congress make some adjustments? We hope that they do as the punitive effects on some homes could have a tremendous effect on the value of those homes at the time an owner might want to sell his home. We all need to be writing our congressmen.