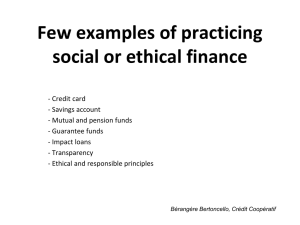

roles of saccos

advertisement

Yves Boily: currently working with Desjardins • Yves has a Master’s Degree in Microbiology from the University of Montreal. • For Développement international Desjardins (DID), he has carried out and supervised appraisal, monitoring, analysis and evaluation missions in Europe, Africa and Asia. • He has over 23 years of experience related to the management and development of international projects (Africa, Asia and Central and Eastern Europe) • Eleven years as university teacher in medical, science and agronomy faculty in Africa. • Program Officer (1988-2000) in charge of the management and monitoring of various savings and credit projects, microfinance projects as well as microenterprise financing projects. • In 2000, he was appointed as Market Development Director at DID's head office and was in charge of the bidding process in the organisation. Roles of SACCOS Network in Value Chain Finance Yves Boily Paul Julien DID • Part of Desjardins group. • Canadian largest financial cooperative. – 5.7 million members – 40,000 employees – 125 billion USD in asset • Corporation specializing in providing technical support for the community finance sector in developing and emerging countries since 1970. Desjardins office in Montréal • 23 DID’s partner networks in 20 developing or emerging countries. • 7,5 million members or clients • Goal: fostering communication among institutions that share the same business model and values, and in order to further sound community finance practices. PROXFIN management committee Nombre de membres ou clients PAYS Réseaux financiers membres de PROXFIN BENIN Fédération des caisses d’épargne et de crédit agricole mutuel du Bénin (FECECAM) AFRIQUE RÉGIONALE Centre d’innovation financière (CIFsa) BURKINA FASO Fédération des caisses populaires du Burkina Faso (FCPB) CAMEROUN Cameroon Co-operative Credit Union League (CAMCCUL) 97 647 GUINÉE Réseau des caisses populaires d’épargne et de crédit Yètè Mali 35 678 HAÏTI Association des coopératives d’épargne et de crédit haïtiennes (ACOOPECH) 210 457 INDE BASIX 265 600 LITUANIE Lithuanian Central Credit Union (LCCU) MALI Réseau des caisses d’épargne et de crédit Nyèsigiso 162 117 MALI Kafo Jiginew (Fédération des caisses mutuelles d’épargne et de crédit de la zone Mali Sud) 205 694 MAURITANIE Agence de promotion des caisses populaires d’épargne et de crédit (PROCAPEC) MEXIQUE Confederación de las cooperativas de ahorro y crédito de México (COFIREM) MEXIQUE SERFIR, S.C. de R.L. de C.V. (Chiapas-Tabasco) 19 896 NICARAGUA FINDESA 39 984 NIGER Mutuelle d’épargne et de crédit des femmes (MECREF) 20 939 PARAGUAY Central de Cooperativas del Área Nacional Limitada (CENCOPAN) PHILIPPINES National Confederation of Co-operatives (NATCCO) RUSSIE National Union of Non-Commercial Organizations of Mutual Financial Assistance RWANDA Centre financier aux entrepreneurs (CFE) – AGASEKE SÉNÉGAL Union des mutuelles du partenariat pour la mobilisation de l’épargne et du crédit au Sénégal (UMPAMECAS) 288 876 SRI LANKA SANASA 858 125 TANZANIE Dunduliza TOGO Faîtière des unités coopératives d’épargne et de crédit du Togo (FUCEC) 196 935 Total Nombre total de familles jointes par les membres de Proxfin : 7 555 264 Nombre total d’individus touchés par les membres de Proxfin : 506 415 * 901 236 61 032 47 316 2 103 884 197 746 1 046 298 222 000 24 245 43 144 35 000 000 Roles of SACCOS in Value Chain Finance • Proximity services to small scale farmers; • Financial support to local farmers organisations; • Adapted loan products to all value chain links within the community; – From the field to final customer • Promotion of good credit and saving habits; • Development of entrepreneurship and local autonomy. From the Field to the Customer Inputs and working capital loans Equipment loans SACCOS Processing and business loans Storage loans Impact of SACCOS in Value Chain SACCOS contribution: • Increase productivity – Access to capital give access to inputs and equipment • Add value to agricultural products – Loans for processing, packaging, etc. • Bring product to consumer – Loan to distributors or retailers • Provide food security in the community – Financing storage Warehouse Receipt Model OTIV - Madagascar Dunduliza - Tanzania Storage Warehouse Receipt Farmers SACCOS Storage loan Destocking Warehouse SACCOS Farmers Withdrawals as needed SACCOS - AMCOS Synergy Model Nyèsigiso – Faso Jigi (Mali) Crop sale SACCOS UNION Repayment AMCOS (Agricultural Marketing Cooperative Society) MOU (Memorandum of understanding) Repayment transfer Crop delivery Refinancing SACCOS if needed Cash advance # 2 SACCOS Harvest (40%) Inputs Cash advance # 1 (60%) Factoring Model Kafo Jiginew – Mali RCPB - Burkina Faso Factoring model Cotton company 7 $ $ 5 2 3 3 6 4 1 SACCOS 8 Cotton growers’ groups $ 1 Inputs request & credit appraisal 5 Invoice payment 2 Inputs delivery 6 Cotton delivery 3 Invoice transfer 7 Cotton payment 4 Loan recording 8 Loan repayment + deposit in farmers’ savings account Some Results Loan products & SACCOS Networks Volume of Credit Number of Farmers Factoring loans (cotton) Kafo Jiginew – RCPB +/- 36 millions USD 75,000 Storage loans (Paddy) OTIV-Madagascar +/- 1 millions USD 850 99% Inputs loans - AMCOS (Paddy) Nyèsigiso - Mali +/- 1 millions USD 1,200 99% Average Repayment Rate 98% (2006/2007 N/A) Conclusion SACCOS proximity to small farmers can give a better access to financial services and contribute to improve value chain finance performance – SACCOS can sometime do it alone when conditions are met: • Regular rain or irrigation, good access to market, stable prices, diversified sources of income, know how, etc. – SACCOS can also be a part of an integrated value chain finance model • Contract farming, synergy with AMCOS, factoring, etc. – SACCOS need to share risk when agriculture lending is too hazardous and could endanger members’ savings: • Guaranty funds, crop insurance, special credit line, etc.