Uploaded by

ameerrohoma15904

Budgeting for Planning & Control: Management Accounting Principles

advertisement

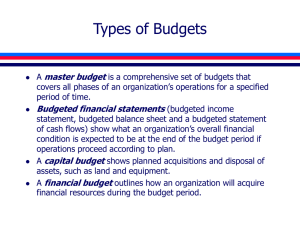

MANAGEMENT ACCOUNTING PRINCIPLES Third year Second term Lecture (2) & (3) Chapter (2): Budgeting for planning and control Learning objectives After studying this chapter, you should be able to: 1. Define budgeting and discuss its role in planning, controlling, and decision making. 2. Prepare the operating budget, identify its major components, and explain the interrelationships of the various components. 3. Identify the components of the financial budget, and prepare a cash budget. 4. Describe budgets for merchandising and service firms. The budget—For planning and control A budget is a tool that managers use to plan and control the use of scarce resources. Time and money are scarce resources to all individuals and organizations; the efficient and effective use of these resources requires planning. Planning alone, however, is insufficient. Control is also necessary to ensure that plans actually are carried out. Most budgets are prepared for a one-year period. The yearly budget can be broken down into quarterly and monthly budgets. This chapter explains the master budget, which consists of a planned operating budget and a financial budget. The planned operating budgets help to plan future earnings and results in a budgeted income statement. The financial budgets help management plan the financing of assets and results in a budgeted balance sheet. 1 MANAGEMENT ACCOUNTING PRINCIPLES Third year Second term Building the Master Budget The master budget is a comprehensive financial plan made up of various individual departmental and activity budgets for the year. A master budget can be divided into: (1) Operating budgets, which outline the income-generating activities of a company (sales, production, and manufacturing costs). The operating budget focuses on the day-to-day running of the company and it usually covers a one-year period. The outcome of the operating budgets is a pro forma (budgeted) income statement. (2) Financial budgets, which outline the inflows and outflows of cash and the financial position. The outcome of the financial budgets includes a Cash budget and Capital budgets are a pro forma (budgeted) balance sheet. The master budget is usually prepared for a one-year period corresponding to the company’s fiscal year. The yearly master budget can be broken down into quarterly and monthly budgets to allow managers to compare actual data with budgeted data and to make timely corrections. Operating Budgets The operating budgets include the budgets for sales, production, manufacturing costs (materials, labor, and overhead) or merchandise purchases, selling expenses, and general and administrative expenses. 1. Sales budget The cornerstone of the budgeting process is the sales budget because the usefulness of the entire operating budget depends on it. The sales budget involves estimating or forecasting how 2 MANAGEMENT ACCOUNTING PRINCIPLES Third year Second term much demand exists for a company's goods and then determining if a realistic, attainable profit can be achieved based on this demand. Sales forecasting can involve either formal or informal techniques, or both. Formal sales forecasting techniques often involve the use of statistical tools. For example, to predict sales for the coming period, management may use economic indicators (or variables) such as the gross national product or gross national personal income, and other variables such as population growth, per capita income, new construction, and population migration. To use economic indicators to forecast sales, a relationship must exist between the indicators (called independent variables) and the sales that are being forecast (called the dependent variable). Then management can use statistical techniques to predict sales based on the economic indicators. Management often supplements formal techniques with informal sales forecasting techniques such as intuition or judgment. In some instances, management modifies sales projections using formal techniques based on other changes in the environment. Examples include the effect on sales of any changes in the expected level of advertising expenditures, the entry of new competitors, and/or the addition or elimination of products or sales territories. In other instances, companies do not use any formal techniques. Instead, sales managers and salespersons estimate how much they can sell. Managers then add up the estimates to arrive at total estimated sales for the period. Usually, the sales manager is responsible for the sales budget and prepares it in units and then in dollars by multiplying the units by their selling price. Although its components are simple, the two items needed to prepare the budget, is often difficult and time‐ consuming. 3 MANAGEMENT ACCOUNTING PRINCIPLES Third year Second term The sales budget in units is the basis of the remaining budgets that support the operating budget. Sales = Units × Selling price per unit Example (1): The Pickup Trucks Company, which makes toy trucks, has just completed its budgeting process for next year. Total expected sales are 100,000 toy trucks at a price of $15.00 each. The expected sales are as follows: Q1: 15,000, Q2: 17,000, Q3: 28,000, Q4: 40,000 units Required: Prepare the sales budget on a quarterly basis. Solution: Pickup Trucks Company Sales Budget for the year ended December 31, 2025 Total Units sold Quarter 1 Quarter 2 Quarter 3 Quarter 4 15,000 17,000 28,000 40,000 Selling price $ 15 Total sales $ 15 target $ 225,000 255,000 100,000 $ 15 $ 15 $ 15 420,000 600,000 1,500,000 Note: In addition to annual and quarterly sales budgets, monthly budgets are often prepared so sales can be tracked against expectations more frequently than once every three months. 4 MANAGEMENT ACCOUNTING PRINCIPLES Third year Second term 2. Production budget Before preparing the direct materials, direct labor, and manufacturing overhead budgets, the production budget must be completed. The production budget shows the number of units that must be produced. To budget for annual production, three things must be known: the number of units to be sold (the units in the sales budget), the required level of inventory at the end of the year, and the number of units, if any, in the beginning inventory (the company's inventory policy). If quarterly budgets are required, this same information is needed on a quarterly basis. Units to be produced = Ending inventory units + Target units sold – Beginning inventory units Example (2): Furniture, Inc., estimates the following number of mattress sales for the first four months of 2025: Month Sales January 10,000 units February 14,000 March 13,000 April 16,000 Finished goods inventory at the end of December is 3,000 units. Target ending finished goods inventory is 30% of the next month's sales. Required: How many mattresses need to be produced in the first quarter (January, February, March) of 2025? 5 MANAGEMENT ACCOUNTING PRINCIPLES Third year Second term Solution: Furniture, Inc. Company Production Budget for the first quarter of 2025 January February March Expected units sold + Required ending Inventory Beginning Inventory Units to be produced 10,000 14,000 13,000 Total 37,000 14,000*30%= 13,000*30%= 16,000*30%= 4,800 4,200 3,900 4,800 (3,000) (4,200) (3,900) (3,000) 11,200 13,700 13,900 38,800 3. Manufacturing costs Budgets Manufacturing costs budgets compose of direct materials, direct labor, and manufacturing overhead budgets. 3.a. Direct materials budget (Purchases budget): The direct materials budget determines the number of units of raw materials to be purchased. It uses the number of units to be produced from the production budget, the required level of ending inventory for raw materials, and the number of units in beginning inventory. Once the number of units to be purchased is determined, it is multiplied by the cost per unit to determine the budgeted amount for raw materials purchases. 6 MANAGEMENT ACCOUNTING PRINCIPLES Third year Second term Units to be produced (production Budget) xx x Direct materials needed per unit of each finished goods xx = Total Direct material units needed for production xx + Desired ending inventory of direct materials xx − Beginning Direct materials on hand (xx) = Direct materials needed to be purchased xx x Cost per Direct materials unit (Unit price) xx = Direct Material Purchases costs (cost of purchases) xx Example (3): Alex. Company provides the following data for next year: Month Direct Material needed for production January 72,000 Kg. February 64,800 March 79,200 April 86,400 Inventory at the end of December is 21,600 Kg. and target ending inventory levels are 30% of next month's direct material needed for production. The cost per direct material unit is $10. Required: Prepare the direct materials budget (Purchases budget) in the first quarter (January, February, March) of 2025. Solution: 7 MANAGEMENT ACCOUNTING PRINCIPLES Third year Second term Alex. Company Direct Material Budget for the first quarter of 2025 January February March Total DM Units production needed for 72,000 64,800 79,200 216,000 + Desired Inventory ending DM 64,800*30% = 19,440 91,440 79,200*30% = 23,760 88,560 86,400*30% = 25,920 105,120 25,920 (-) Beginning Direct Material (21,600) Inventory (19,440) (23,760) (21,600) Direct Material purchase 69,840 needed for production 69,120 81,360 220,320 * Unit price 10 10 10 691,200 813,600 2,203,200 purchases required Direct costs Material 10 purchase 698,400 Example (4): Alex. Company wants 25,000 units to be produced during March. At Alex. Company, five pounds of material are required per unit of product. Management wants materials on hand at the end of each month equal to 10% of the following month’s production needs. Expected production units in April are 28,000 units. On March 1, 13,000 pounds of material are on hand. Material cost is $0.70 per pound. Required: Prepare the direct materials budget for March. Solution: 8 241,920 MANAGEMENT ACCOUNTING PRINCIPLES Third year Second term Alex. Company Direct materials Budget for the month ended March 31, 2025 March Units to be produced (production Budget) 25,000 x Direct materials needed per unit of each finished goods 5 pounds = DM Units needed for production (25,000 * 5) 125,000 + Desired ending DM inventory (28,000 *5) * 10% 14,000 (-) Beginning DM Inventory (13,000) = Direct materials needed to be purchased 126,000 x Cost per Direct materials unit (Unit price) 0.7 = Direct Materials Purchase costs $ 88,200 9 MANAGEMENT ACCOUNTING PRINCIPLES Third year Second term Lecture (4) Budgeting for planning and control: Manufacturing costs Budgets 3.b. Direct labour budget The direct labor (DL) budget shows the total direct labor hours needed and the associated cost based on the input-output relationship of each product. Expected DL hours = DL hours needed per unit of output × Units of output DL costs = Expected DL hours × Wage rate Example (5): Alex. Manufacturing Inc. produces two products, A and B. Alex expects to sell 10,000 units of product (B) and to have an inventory of 2,000 units of (B) on hand at the end of the period. Currently, Alex has 800 units of (B) on hand. Product (B) requires two labor operations, molding and polishing. Each unit of product (B) requires one hour of molding and two hours of polishing. The direct labor rate for molding is $20 per molding hour and the direct labor rate for polishing is $25 per polishing hour. Required: Prepare the direct labour budget for product (B). 10 MANAGEMENT ACCOUNTING PRINCIPLES Third year Second term Solution: Alex. Company Production budget for product (B) Product (B) Sales 10,000 units + Required ending Inventory 2,000 Units required 12,000 - Beginning Inventory (800) Units to be produced 11,200 units Direct labour budget for product (B) Product (B) Units to be produced 11,200 units Labour operations Molding Polishing Direct labour hour per unit 1 2 hours Expected Direct labour hours (11,200*1=) 11,200 $ 20 (11,200*2=) 22,400 $ 25 * direct labour rate The expected cost of direct labour 224,000 $ 560,000 for operation Total expected cost of direct labour $ 784,000 for (B) 11 MANAGEMENT ACCOUNTING PRINCIPLES Third year Second term 3.c. Overhead budget The overhead budget shows the expected cost of all indirect manufacturing items. The estimated overhead is divided into variable and fixed components: Total overhead cost = Variable overhead cost + total fixed overhead costs In more details: Total overhead = (Variable overhead rate × Activity level per chosen cost driver) + Budgeted total fixed overhead costs Example (6): Alex. Manufacturing Inc. expects to produce and sell 6,000 units of product (A), its only product, for $20 each. Variable manufacturing overhead is $3 per unit. Fixed manufacturing overhead is $24,000 in total. Required: Prepare the overhead budget for product (A). Solution: Alex. Manufacturing Inc. Overhead budget for product (A) Product (A) Units to be produced 6,000 units * Variable manufacturing overhead per $3 unit = Variable manufacturing overhead (6,000 * 3 =) 18,000 + Fixed manufacturing overhead $ 24,000 = Total overhead costs 42,000 12 MANAGEMENT ACCOUNTING PRINCIPLES Third year Second term 4. Selling, administrative, and other expense budgets To prepare the Master Budget you need to prepare operating budgets and financial budget. You had studied Purchases, Direct Labour, and Manufacturing Costs Budgets as operating budgets. As well, Selling, Administrative, and other expense budgets are parts of operating budgets. The costs of selling a product are closely related to the sales forecast. Generally, the higher the forecast, the higher the selling expenses. Administrative expenses are likely to be less dependent on the sales forecast because many of the items are fixed costs (e.g. salaries of administrative personnel and depreciation of administrative buildings and office equipment). Managers must also estimate other expenses such as interest expense, income tax expense, and research and development expenses. Example (7): Alex. Manufacturing Inc. expects to produce and sell 6,000 units of product (A), its only product, for $20 each. Variable selling and administrative expenses are $1 per unit, and fixed selling and administrative costs are $3,000 in total. Required: Prepare the selling and administrative Budget. Solution: Alex. Manufacturing Inc. Selling and Administrative Budget Product (A) Units to be produced 6,000 units Variable selling and administrative expenses 6,000 * 1 = Fixed selling and administrative costs $ 3,000 Total selling and administrative costs 9,000 13 6,000 MANAGEMENT ACCOUNTING PRINCIPLES Third year Second term 5. Budgeted Income Statement A budgeted income statement is simply a predicted income statement for a future period of time. The budgeted income statement is an important part of a business's financial planning process. The budgeted income statement, along with a budgeted balance sheet, can help a business determine if its plans are financially feasible. A business can develop and compare different budget projections to help in making decisions about which projects the business should pursue and how it can pay for them. Example (8): Alex. Company projects sales of 25,000 units during May at $6 per unit. Production costs are $1.80 per unit. Variable selling and administrative expenses are $0.60 per unit; fixed selling and administrative expenses are $60,000. Required: Prepare the budgeted Income Statement before income taxes. Solution: Alex. Company Budgeted Income Statement Sales units 25,000 units X Selling price per unit $6 = Sales revenue $150,000 (-) Cost of goods sold 25,000 units * $1.8 (45,000) Gross Margin 105,000 (-) Variable selling and administrative 25,000 units * $0.60 expenses (-) Fixed selling and administrative costs Net income before taxes (15,000) 14 (60,000) $ 30,000 MANAGEMENT ACCOUNTING PRINCIPLES Third year Second term 15

0

0

advertisement

Download

advertisement

Add this document to collection(s)

You can add this document to your study collection(s)

Sign in Available only to authorized usersAdd this document to saved

You can add this document to your saved list

Sign in Available only to authorized users