IAS Accounting Standards: Tangible Assets, Grants, Borrowing Costs

advertisement

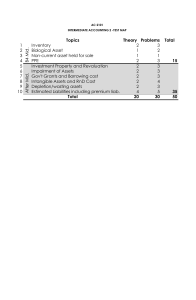

CHAPTER 2 TANGIBLE NON-CURRENT ASSETS IAS-16 PROPERTY, PLANT & EQUIPMENT All the costs that should be included in the initial measurement of an asset are: 1. Bring asset to working condition 2. Site Preparation, Delivery Costs, Installation Costs, Borrowing Costs 3. Dismantling Costs Subsequent Expenditure 1. Capital Expenditure Which will increase - Existing useful life - Existing performance 2. Revenue Expenditure Which will maintain - Existing performance - Repairs, Maintenance Revaluation of Non-Current Assets 1. Cost Model = Cost less accumulated depreciation. 2. Revaluation Model = Revalued amount less any subsequent accumulated depreciation . = Surplus is recorded in SOCIE whilst loss is recorded in SOPL. = Revaluation gain is added in other comprehensive income whilst loss is recorded in SOPL Upward Revaluation An asset was revalued upward from 1000 to 1200. Dr NCA 200 Cr R.S 200 Downward Revaluation An asset was revalued downward from 1000 to 800. Dr R.D 200 Cr NCA 200 Upward and Upward Revaluation An asset was revalued upward from 1000 to 1200 and then to 1400. Same as first entry. Downward and Downward Revaluation An asset was revalued downward from 1000 to 800 and then to 600. Same as second entry. Upward and Downward Revaluation An asset was revalued upward from 1000 to 1200 and then to 900. Dr R.D 100 Dr R.S 200 Cr NCA 300 Downward and Upward Revaluation An asset was revalued downward from 1000 to 800 and then to 1100. Dr NCA 300 Cr R.D 200 Cr R.S 100 IAS-20 GOVERNEMENT GRANTS 1. REVENUE GRANTS The costs are 200,000 and govt. grants are 100,000. The rest of the amount is to be paid by the company. SOCIE OPTION 1 SOCIE OPTION 2 Staff costs (200,000) Govt. Grants 100,000 Net amount (100,000) Staff costs (100,000) 2. CAPITAL GRANTS These are related to the purchase of non-current assets. An asset is bought for 100,000 with useful life of 5 years. Govt. grant is 50,000 for 5 years. OPTION 1 SOCI SOFP Depreciation (10000) NCA 50000 DEP (10000) NBV 40000 OPTION 2 SOCI Depreciation Govt. Grants (20000) 10000 (10000) SOFP NCA DEP NBV NCL G.G Amm 100000 (20000) 80000 50000 (10000) 40000 IAS-23 BORROWING COST If a company takes out a loan for the purpose of financing the acquisition of a qualifying asset, that is known as borrowing cost. These should be capitalized with the cost of assets in SOFP. A qualifying asset is an asset which takes substantial time period to get ready for its intended use or sale. Commencement of Capitalization 1. When activities on the assets or on qualifying assets has been started. 2. Borrowing costs has been started. Loan taken and approved. 3. Investment on the qualifying asset has been done. All the above 3 conditions should be met in order to treat it as a borrowing cost else won’t be classified as borrowing costs. Before this we will expense out. EXAMPLE NO.1 Loan taken and asset taken on the same date as 1st Jan. Now in SOFP the qualifying asset value is 100,000 and interest is 10%. SOFP = 100,000 + 10,000 = 110,000 SOCIE = Finance Cost = 0 EXAMPLE NO.2 The asset became qualifying on 1st April and at a value of 100,000. Loan was arranged on 1st Jan @ 10%. The Co. invested 80,000 for 6 months @ 8% interest. SOFP Qualifying asset + Borrowing Cost [10000*(9/12)] -Temporary Income [80000*8%*(3/12)] Asset Value 100,000 7500 (1600) 105900 SOPL Finance Costs [10000*(3/12)] -Temporary Income SOCIE 2500 (1600) 900 Cessation of Assets All activities necessary to prepare the qualifying asset for its intended use or sale are complete or construction has been suspended. EXAMPLE NO.1 An asset costing 100,000 became qualifying on 1st Jan and loan was arranged on 1st Jan. Loan Interest is 10%. Asset was ceased for two months of August and September and completed in November. For the months, construction didn’t occur, they will be treated as finance costs. For 3 months = 100,000 × 10% × 3/12 = 2500 Add: Depreciation (Useful life 5 years) = 100,000/5 = 2500 Types of Borrowing 1. Specific For e.g = 9.5% @ 850,000 2. General There is no concept of temporary income under general borrowings. 100,000 10% 1st Jan 200,000 12% 1st April 300,000 14% 1st July (100,000*10%*(12/12)) + (200,000*12%*(9/12)) + (300,000*14%*(6/12)) (100,000*(12/12) + (200,000*(9/12)) + (300,000*(6/12)) The rate is equals to 12.25% IAS-40 INVESTMENT PROPERTY It is applied on: 1. Investment properties held for capital appreciation 2. Rental purposes (whole property is declared for rental purposes) - In IAS-16, there is historical cost model and revaluation model. - In IAS-40, there is cost model and fair value model. - In cost model, depreciation is charged but in fair value model, it is not charged.