Cost Accounting Reviewer: Labor & Overhead

advertisement

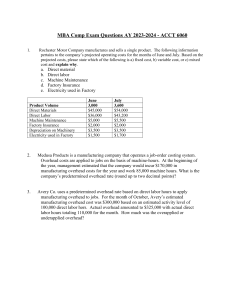

COST ACCOUNTING REVIEWER Topic I: Accounting for Labor Labor Classifications Labor — consists of workers’ payroll who are needed to process and convert raw materials into finished goods. Direct Labor ▪ ▪ Payroll costs that are paid to workers who are directly engaged in the conversion process of raw materials to finished goods Charged to Work In Process Account Indirect Labor ▪ ▪ Payroll costs that are paid to a worker that supports the production process and which are not directly involved in the conversion of raw materials into finished products Charged to Factory Overhead Control Account Recording Payroll ❖ Recording the number of hours used in total and by job. ❖ Recording the quantity produced by the workers. ❖ Amalyzing the hours used by the employees to determine how time is to be charged. ❖ Allocation of payroll costs to jobs and factory overhead accounts. ❖ Preparation of the payroll, including computation and recording of the employees gross earnings, deductions, and net earnings. Control for Labor ❖ Correct timekeeping ❖ Strict control on labor engagement ❖ Analysis of time in terms of departments, operations, and productions orders ❖ Improvement in the method of production Timekeeping Clock cards Time tickets Production reports Payroll Payroll records Employee’s earning records Payroll Summaries Types of Earnings ✓ Wages – earnings of an employee who is paid by hour, piece or day. ✓ Salaries – earnings of an employee who is paid a flat amount of per week or month regardless of the hours worked in a period. ✓ Commissions – gross earnings of an employee typically based on the number of sales. Wage Payment Plans - Should be approved by the Union and should comply with regulations of government agencies. Time Based Wage Plan / Hourly Rate Plan - - Wages are determined on the basis of time spend by workers irrespective of the quality of the work done. Calculated by multiplying the hourly rate of the worker by the number of time spent. Piece Based Wage Plan - - Wages are determined on the basis of output produced by the workers without considering the time spent in performing the job. Calculated by multiplying the number if units by a specified rate per unit. Modified Wage Plan - - Combination of hourly wage and piece wage plan. Wages are paid based on a minimum hourly rate regardless if an established quota of production is not met. However, workers are given a bonus for the additional piece of output if they exceed the established quota. Bonus or Incentive Scheme - Wages are based on a bonus plan intended to increase production. Can be on an individual or group incentive plan. Employee’s Gross Earnings ❖ If hourly Based Wage Plan (Basic Hourly Pay x Hours Spent) + Overtime ❖ If Piece Based Wage Plan Number of Units Produced x Pay per piece Payroll Deductions Mandatory Contributions / deductions ✓ ✓ ✓ ✓ SSS/GSIS contributions PhilHealth contributions PAG-IBIG contributions Withholding taxes on compensation Other Contributions / deductions ✓ Union Fees Net Pay = Gross Earnings – deductions Labor Losses Idle Time • • Normal Idle Time Abnormal Idle Time Machine Set-Up Time Labor Costs of Reworking Defective Units Topic II: Accounting for Overhead Factory Overhead ❖ Includes all factory costs incurred in the manufacturing process other than direct materials and direct labor. ❖ Also known as manufacturing overhead, factory burden, and indirect manufacturing costs. ❖ Normally accumulated into cost pools and allocated to unit produced are later sold as finished goods. ▪ ▪ ▪ Indirect Materials Indirect Labor Other Manufacturing Expenes/Indirect Expenses Recognition of Factory Overhead 1. Budgeting of Expenses Related to Overhead 2. Determining of Factory Overhead Rate 3. Applying the Factory Overhead Rate to appropriate base of production Budgeting of Expenses Related to Overhead ❖ Budget is a detailed plan, expressed in quantitive terms, about business operations for a specific period. ❖ When the company has already classified factory overhead as either fixed or variable, the budgets are the prepared for the expected level of production. ❖ Factory overhead budget helps the company monitor and control production costs to improve its profit margin. Accounting for Factory Overhead Rate ✓ Predermined FOH Rate – used to apply FOH costs to products, services, or jobs. ✓ Plant-Wide or Blanket Rate – single OH rate to all o Similar products o Services are relatively similar o Total amount of FOH rate to be allocated is too small that using multiple allocaton rates is unnecessary and costly. ✓ Departmental Rate – one OH rate for each department o Various products with different processes o Services are highly differentiated o Total amount of FOH rate to be allocated is too large. ✓ Overhead Bases – allocation bases should be related to the functions represented by the factory overhead costs being applied. o Physical output/units produced o Direct Materials Cost o Direct Labor Cost o Direct Labor Hours o Machine Hours Predetermined Overhead Rate = Estimated Factory Overhead Costs / Estimated Allocation Base [SAMPLE PROBLEM] P2P Company estimates factory overhead at P225,000 for the next fiscal year. It is estimated that 45,000 units were to be produced at a direct material costs of P300,000. Conversion will require an estimated 50,000 direct labor hours at a cost of P1.50 per hour, with 22,500 machine hours. ▪ Physical Output per Units Produced Predetermined overhead rate = Estimated FOH Costs / /Estimated Allocation Base = P225,000 / 45,000 units = P5.00 / unit of production ▪ Direct Materials Cost Predetermined overhead rate = Estimated FOH Costs / /Estimated Allocation Base = P225,000 / P300,000 = 0.75 or 75% of material costs ▪ Direct Labor Cost Predetermined overhead rate = Estimated FOH Costs / /Estimated Allocation Base = P225,000 / (P1.50 x 50,000 DLHs) x 100 = P225,000 / (75,000) x 100 = 3 x 100 = 300% of Labor Costs ▪ Direct Labor Hours Predetermined overhead rate = Estimated FOH Costs / /Estimated Allocation Base = P225,000 / 50,000 DLHs = P4.50 per DLH ▪ Machine Hours Predetermined overhead rate = Estimated FOH Costs / /Estimated Allocation Base = P225,000 / 22,500 MHrs = P10 per MHrs Capacity of Production – in the estimation of the factory overhead base and its allocation base, it is important to know the capacity of production to be used. ✓ Theoretical (Maximum or Ideal) – plan or department’s capablity to produce without any interruptions. ✓ Practical – plan or department’s capablity to produce with an allowance for internal factors. o Theoretical less unavoidable operating interruptions ✓ Expected (Budget) – level based on expected capaciy utilization for the budget period. ✓ Normal – most commonly used capacity. o Capacity driven by customers or business demand and not by maximum capacity. Typial Allocation Bases for Common Costs Departmentalization of Factory Overhead Departmentalization – dividing the plant into segments or departments or cost centers to which expense are charged. ✓ Producing Department – responsible for actual manufacture of the product. o Cutting, Assembly, Machining, Sewing, Mixing, Extracting, Refining, Finishing, etc. ✓ Service Department – responsible in assisting other departments by redering services to production and service departments. o Repairs and Maintenance, Storage, Medical, Recieving, Purchasing, Personnel, Security, Cafeteria, Inspection, etc. Direct Departmental Expenses ❖ Supervision ❖ Indirect Labor ❖ Overtime ❖ Sick and Vacation Leaves ❖ Pension aand other Labor Fringe Benefits ❖ Mandatory Contributions ❖ Indirect Materials ❖ Factory Supplies ❖ Repairs and Maintenance Indirect Departmental Expenses ❖ Depreciation – Building ❖ Factory Rent ❖ Insurance – Building ❖ Interior and Building Maintenance ❖ Supervision ❖ Utilities ❖ Insurance – Equipment ❖ Depreciation – Equipment ❖ Equipment Maintenance ❖ Property Taxes ❖ Freight – In ❖ Materials Handling Methods of Service Department Cost Allocation 1. Direct Method – simplest of the three methods. - It ignores interdepartmental services which means no portion of the cost of the service department is allocated to another service department, only directed to revenue producing departmemnts. 2. Step Method – allocates in a sequential manner. - Starts with the service department that provides the most number of services or with the one with the largest amount of costs. 3. Algebraic Method – also called “reciprocal method”. - It is the most accurate and recognizes interrelationship among all departments. [SAMPLE PROBLEM] AD Inc. is exploring ways to allocate the cost of service departments such as Quality Control and Maintenance to the production departments such as Machining and Assembly. In determining the factory overhead rate, the machine hours 30,000 is used for Machining Department and 60,000 direct labor hours is used for Assembly Department. The controller of the company has the following information: DIRECT METHOD Cost Total Quality Control Maintenance Machining Assembly P350,000 P200,000 P400,000 P300,000 P(350,000) P262,500 P87,500 P(200,000) P120,000 P80,000 P782,500 P467,500 Divide by MHrs 30,000 Divide by DLHrs 60,000 FOH/hr P26.08/MHr P7.79/DLHr Allocation Fraction: Allocation of Quality Control Machining 21,000/28,000 x P350,000 Assembly 7,000/28,000 x P350,000 Allocation of Maintenance Machining 18,000/30,000 x P200,000 Assembly 12,000/30,000 x P200, 000 STEP METHOD Cost Total Quality Control Maintenance Machining Assembly P350,000 P200,000 P400,000 P300,000 P(350,000) P70,000 P210,000 P70,000 P(270,000) P162,000 P108,000 P772,000 P478,000 Divide by MHrs 30,000 Divide by DLHrs 60,000 FOH/hr P25.73/MHr P7.97/DLHr Allocation Fraction: Allocation of Quality Control Maintenance 7,000/35,000 x P350,000 Machining 21,000/35,000 x P350,000 Assembly 7,000/35,000 x P350,000 Machining Assembly Allocation of Maintenance 18,000/30,000 x P270,000 12,000/30,000 x P270,000 Topic III: Activity-Based Costing Activity-based Costing ❖ Costs are allocated on the basis of different types of cost drivers utilized. It uses a cost hierarchy to classify different activities. ▪ ▪ ▪ ▪ Unit Level Activities – activities performed evey time a service is performed or product is made. Bath-Level Activities – activities which occur every time a group of units is produced or a seried of steps are made. Product-Line Activities – activities that occur too support an entire product line but nt always performed every time a new unit or batch of products is produced. Facility-Level Activities – activities that are carried out at the plant level, it is independent of the number of units produced. [SAMPLE PROBLEM]