Grade 10 Accounting Tutor Materials: Accounting Equation & Ledger

advertisement

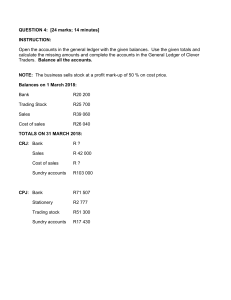

CURRICULUM FET ACCOUNTING TUTOR MATERIALS TERM ONE 2024 BACK ON TRACK PROGRAMME GRADE 10 TOPIC 1: THE ACCOUNTING EQUATION DATE: 2 MARCH 2024 BASELINE ASSESSMENT: TRANSACTION ANALYSIS Use the transactions below to complete the analysis of transactions table. See the format and example below: Example: Paid the business telephone account by EFT, R800. No. E.g., GENERAL LEDGER Account to be Account to be Credited Debited Telephone Bank ACCOUNTING EQUATION Assets = Owners’ Liabilities Equity + - 800 - 800 0 Transactions: 1. The owner decided to increase his capital contribution by depositing R30 000 directly into the current banking account of the business. 2. Received a direct deposit of R500 from a debtor in full settlement of their account. 3. Cash sales amounted to R6 440 (cost price, R4 600). 4. Made an EFT to settle our account with our creditor, R7 500. 5. Paid the weekly wages by EFT, R1 000. 6. Credit sales to a debtor, R1 680 (profit mark-up is 40% on cost price). 7. Received a direct deposit from the tenant for rent income, R3 750. 8. Bought trading stock on credit from a creditor, R5 000. 9. Bought stationery on credit from a creditor, R750. 2 ACTIVITY 1: ACCOUNTING EQUATION The following information appeared in the accounting records of Mug Stores for the month of January 2023. REQUIRED: Use the information below to complete the table provided in your Answer Book. (NOTE: Bank balance is favourable at all times.) Example: Rent received from tenant Nathee Mbane, R14 500. Accounting Equation GENERAL LEDGER ACCOUNT TO BE DEBITED No. E.g. Bank ACCOUNT TO BE DEBITED Rent Income Amount A= OE + L 14 500 + + 0 INFORMATION 1. Goods sold on credit to A. Lwethu, R9 200. Cost of sales R4 600. 2. Cash deposit fees for R400 and credit card levy R120 appeared in the bank statement. 3. Interest charged on overdue debtor’s account amounted to R230. 4. An amount of R5 700 was paid for repairs to the motor vehicle. 5. Stationery was purchased for R320 cash. ACTIVITY 2: ACCOUNTING EQUATION Use the transactions below to complete the analysis of transactions table. See the format and example below: Example: Paid the businesses telephone account by EFT, R800. GENERAL LEDGER No. E.g. ACCOUNT TO BE DEBITED Telephone ACCOUNT TO BE CREDITED Bank 3 Amount 800 Accounting Equation A = OE + L - - 0 Transactions: 1. Purchased trading stock on credit from DDX Suppliers for R4 200. 2. EFT was made to Stand Bank for R18 800. R17 000 is in repayment of the loan and the remainder is for interest for the last six months. 3. Received a bank statement from Stand Bank and noted that the following appeared on the bank statement: • Bank charges, R275 • Interest on current account, R40 • A debit order for the payment of the annual insurance premium of R5 200. 4. A debtor, S Rocks, requested an allowance of R120 on goods that were damaged while they were being transported. 5. Paid Fast Lane Transporters R300 by EFT, for transporting stock purchased to our store. 6. Received R720 cash from D Bell whose account had previously been written off as a bad debt. 7. Bought the equipment on credit from Hendry Suppliers, R20 000. BASELINE ASSESSMENT: GENERAL JOURNAL TRANSACTIONS The following transactions were taken from the records of Glynis Stores during June 2023. REQUIRED: Analyse the following transactions according to the Accounting Equation A= OE + L Indicate which account will be debited and credited in the General Ledger. INFORMATION: 1. Interest on the overdue account of M. Jara must be charged at 12% p.a. His balance of R2 800 is three months in arrears. 2. Write off the account of J. Jan as irrecoverable, R500. 3. The owner took stock, with a cost price of R1 500, for personal use. 4. The owner donated stock, R990 (cost price) to a Children’s Home. It was mistakenly debited to Drawings. 5. Transferred C Carl’s credit balance, R400 in the Debtors Ledger to her account in the Creditors Ledger. 4 ACTIVITY 3: ACCOUNTING EQUATION Analyse the given transactions. See the format and example below: Example: Write off the account of a debtor as irrecoverable, R500 GENERAL LEDGER No. E.g. Account to be debited Bad debts Account to be credited Debtor’s Control Amount 500 Accounting Equation A = OE + - - L 0 INFORMATION: The following transactions are from the books of Larah Traders who applies 100% mark up on trading stock. 1. B. Good (debtor) is declared insolvent. His insolvent estate paid a first and final dividend of 20 cents in the rand per EFT (electronic funds transfer), R292. Write off the balance as irrecoverable. 2. The owner took stock, with a selling price of R1 500, for personal use. 3. Charged debtor A. Andy 10% p.a. interest on her overdue account of 3 months. She owed R600. 4. Transfer M. Salah’s debit balance, R400 from the Debtors Ledger to the Creditors Ledger. 5. Received an EFT payment from AB Bank for R11 000, for a fixed deposit of R10 000 that matured on 30 January 2021. The full amount was entered in the Fixed Deposit account. Correct the error. 5 ACTIVITY 4: ACCOUNTING EQUATION Use the transactions below to complete the analysis of transactions table. See the format below: GENERAL LEDGER No. Account to be debited Account to be credited Amount Accounting Equation A = OE + L INFORMATION: The following transactions relate to Kolisi Traders. They maintain a profit mark up of 50% mark up on cost. 1. Siya Kolisi, the owner, took stationery (R130) and trading stock (selling price R960) for personal use. 2. C. Candice, a debtor owing R430, must be written off as irrecoverable. 3. Kolisi Traders failed to pay their account of R8 820 with NO.1 Dealers on time. Interest for two months at 10% p.a. must be brought into account. 4. Repairs of R20 000 was done to the roof of the building. This was entered in the Land and Buildings account in error. 5. B. Patient, whose account was previously written off as bad debt, settled his outstanding account of R1 250. This receipt was entered in the Debtors Control column of the Cash Receipts Journal in error 6 TOPIC 1: INFORMAL ASSESSMENT ACCOUNTING EQUATION (19 marks; 15 minutes) The information pertains to Jozi Stores. Transactions were taken from their May 2023 records. REQUIRED: 1. Analyse each transaction according to the table given in the Answer book. Show an increase with a + and a decrease with a - Show no effect with a 0. (19) INFORMATION: No. Account to be debited Account to be credited 1. Bought trading stock on credit for R50 000. 2. Sold goods on credit, R21 000. Applied the mark-up policy of 50%. 3. Borrowed R70 000 from VBS Bank at an interest rate of 12% p.a. 4. The owner took trading stock for own use, R1 200 (Cost price). 5. Stationery was incorrectly recorded as trading stock purchased, R500. Amount 7 Assets Owners’ equity Liabilities TOPIC 2: THE GENERAL LEDGER DATE: 16 MARCH 2024 BASELINE ASSESSMENT: GENERAL LEDGER Indicate the contra account in each of the following ledger accounts: TRANSACTIONS Took delivery of trading stock purchased from ABC Suppliers, R36 000. Purchase are subject to 5% trade discount. Dr Debit order payment to the municipality for municipality expenses, R4 123. Dr Cr Bank The owner (Ms Mbane) deposited R5 000 as additional capital. Dr Bank Cr (D) The Bank statement from IOU Bank showed the following: Service fees R576; Cash deposit fees R84; Credit card levy R402; Interest on overdraft R1 228. Dr Bank charges Dr (E) Cr (F) Received R50 000 from BT Bank. It was for a loan negotiated at 10% p.a. interest. Dr (G) Cr Loan: BT Bank Cash sales to date R6 210; the mark-up is 50% (CRT 4). Dr Dr Cr Cr (H) Cost of sales Sales (I) Cr (A) Calculation of trade discount (B) Bank (C) Calculation for cost of sales (J) 8 ACTIVITY 5: GENERAL LEDGER ACCOUNTS REQUIRED: Use the information below to prepare the TRADING STOCK account in the General Ledger of Inga Traders for March 2023. INFORMATION: Balance on 1 March 2023: Trading Stock R53 000 The following are the extracts of various subsidiary journals for March 2023: Cash Receipts Journal of Inga Traders for March 2023 Bank Sales Cost of sales 110 300 102 000 76 000 CRJ1 Sundry accounts 8 300 Cash Payments Journal of Inga Traders for March 2023 Bank Trading Stock Creditors Control 96 900 2 900 520 CPJ1 Sundry accounts 800 Debtors Journal of Inga Traders for March 2023 Sales 174 000 DJ1 Cost of sales 99 000 Debtors Allowances Journal of Inga Traders for March 2023 Debtors Allowances Cost of sales 19 450 16 300 DAJ1 Creditors Journal of Inga Traders for March 2023 CJ1 Creditors Control Trading Stock Consumable Stores 233 000 210 000 9 000 Creditors Allowances Journal of Inga Traders for March 2023 Creditors Control Trading Stock Consumable Stores 15 500 14 250 300 9 Sundry accounts 14 000 CAJ1 Sundry accounts 1 000 ACTIVITY 6: GENERAL LEDGER ACCOUNTS Use the information given below to prepare the Trading stock, Debtors’ Control, Creditors’ Control, Stationery and Discount Allowed accounts in the General Ledger of Van Niekerk Sport Stores. INFORMATION: Balances on: 1 April 2023 Trading Stock R153 200 Debtors’ Control R102 500 Creditors’ Control R140 500 Stationery R18 600 Discount allowed R16 725 Summary of information obtained from certain subsidiary journals for April 2023. Cash Receipts Journal Bank Sales Cost of sales Debtors’ control Discount allowed Sundry accounts R300 400 140 600 90 125 160 500 7 000 6 300 Cash Payments Journal Bank Trading stock Creditors’ control Discount received Stationery Sundry accounts R196 500 83 200 100 235 3 045 9 025 7 085 Debtors’ Journal Sales Cost of sales R241 120 150 700 Debtors’ Allowances Journal Debtors’ allowances Cost of sales R16 200 10 125 Creditors’ Journal Creditors control Trading stock Equipment Stationery Packaging Creditors’ Allowances Journal Creditors control R8 890 Trading stock 6 050 Stationery 620 Packaging 150 R120 850 60 000 50 000 8 050 1 220 Information extracted from the General Journal (a) Trading stock purchased during April 2014, R1 250 was incorrectly recorded in the Stationery column in the Cash payments Journal and posted as such. Correct the error. (b) The owner took trading stock for her own use during April, R3 800. (c) Debtors’ control Journal debits Journal credits Creditors’ control Journal debits Journal credits R200 R875 10 R1 450 2 700 ACTIVITY 7: GENERAL LEDGER ACCOUNTS REQUIRED: Use the given information to post to the following accounts in the General Ledger of Topley Traders. Close off the accounts in the balance sheet section. Balances on 1 April 2023: Trading Stock Debtors' Control Creditors' Control Sales Cost of Sales Debtors' Allowances Stationery B6 B7 B8 N1 N2 N3 N4 R102 500 76 250 68 440 213 225 142 150 8 300 3 800 Note: Goods are sold at cost plus 50%. The following totals appeared in the journals as on 31 April 2023: Cash Receipts Journal of Topley Traders – April 2023 Debtors’ Bank Sales Cost of sales control 144 600 74 400 64 680 ? Cash Payments Journal of Topley Traders – April 2023 Trading Creditors’ Bank Stock Stationery control 140 800 3 240 47 500 ? Debtors’ Journal of Topley Traders – April 2023 Sales Cost of sales 42 100 ? Discount allowed 2 390 CRJ2 Sundry accounts 7 910 Discount received 1 300 CPJ2 Sundry accounts 22 400 DJ2 Debtors’ Allowances Journal of Topley Traders – April 2023 DAJ2 Debtors’ Allowances Cost of sales 780 520 Creditors’ Journal of Topley Traders – April 2023 Creditors’ Control ? Trading Stock 50 300 Stationery 7 350 11 CJ2 Sundry Accounts 2 450 Creditors’ Allowances Journal of Topley Traders – April 2023 Creditors’ Control 1 415 Trading Stock 850 CAJ2 Sundry Accounts 475 Stationery 90 General Journal of Topley Traders – April 2023 GJ2 Debtors’ control Creditors’ control Debit Credit Debit Credit 320 1 350 365 180 TOPIC 2: INFORMAL ASSESSMENT GENERAL LEDGER (20 marks; 15 minutes) The information pertains to Jozi Stores. Transactions were taken from their May 2023 records. REQUIRED: 1. Post the transactions to the selected ledger accounts provided in the Answer Book. (20) NOTE: First enter the initial balances/totals in the ledger accounts. INFORMATION: A. Balances / Total on 1 May 2023: Debtor’s control R7 200 Creditor’s control 10 400 Bank 6 000 Trading stock 8 000 Do NOT balance or close off the accounts at the end of the month. NB: Accept a favourable bank balance throughout. 1. Bought trading stock on credit for R50 000. 2. Sold goods on credit, R21 000. Applied the mark-up policy of 50%. 3. Borrowed R70 000 from VBS Bank at an interest rate of 12% p.a. 12