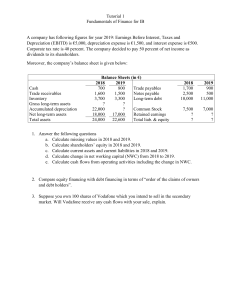

Accounting Practice Problems: Investment Property & Asset Valuation

advertisement

Problem 1 Robust Company purchased an investment property on January 1, 2018 at a cost of P4,000,000. The property had a useful life of 20 years and on December 31, 2019 had a fair value of P4,800,000. On December 31, 2019 the property was sold for net proceeds of P4,500,000. The entity used the cost model to account for the investment property. What is the gain to be recognized for 2019 regarding the disposal of the investment property? A. 900,000 B. 500,000 C. 800,000 D. 700,000 Answer: A Cost – Jan. 1, 2018 Accumulated depreciation (4,000,000/ 20 x 2) Carrying amount – Dec. 31, 2019 P4,000,000 Sale price Carrying amount Gain on disposal P4,500,000 3,600,000 P900,000 (400,000) P3,600,000 Reference: Intermediate Accounting Volume 1 2019, C. Valix, p. 566 Problem 2 On January 1, 2019, Scholastic Company acquired a building to be held as investment property in a remote location for P5,000,000. After initial recognition, the entity measured the investment property using the cost model because the fair value cannot be measured reliably. On December 31, 2019, management assessed the useful life of the building at 20 years from the date of acquisition and presumed the residual value to be nil because the fair value cannot be determined reliably. At year-end, the entity declined an unsolicited offer to purchase the building for P6,500,000. This is a onetime offer that is unlikely to be repeated in the foreseeable future. What is the carrying amount of the building on December 31, 2019? A. 5,000,000 B. 6,500,000 C. 6,175,000 D. 4,750,000 Answer: D Cost of the investment property Accumulated depreciation (5,000,000/ 20) Carrying amount – Dec. 31, 2019 P5,000,000 (250,00 0) P4,750,000 Reference: Intermediate Accounting Volume 1 2019, C. Valix, p. 568 Problem 3 Rhino Company, a real estate entity, had a building with a carrying amount of P20,000,000 on December 31, 2019. The building was used as offices of the entity’s administrative staff. On December 31, 2019, the entity intended to rent out the building to independent third parties. The staff will be moved to a new building purchased early in 2019. On December 31, 2019, the entity also had land that was held for sale in the ordinary course of business. The land had a carrying amount of P10,000,000 and fair value of P15,000,000 on December 31, 2019. On such date, the entity decided to hold the land for capital appreciation. The accounting policy is to carry all investment property at fair value. 1. On December 31, 2019, what amount should be recognized in revaluation surplus as a result of transfer of the building to investment property? A. 20,000,000 B. 35,000,000 C. 15,000,000 D. 0 2. On December 31, 2019, what amount should be recognized in profit or loss as a result of transfer of the land to investment property? A. 15,000,000 B. 10,000,000 C. 5,000,000 D. 0 Question 1 Answer: C Fair value of building Carrying amount of building Revaluation surplus P35,000,000 20,000,000 P15,000,000 Question 2 Answer: C Fair value of land Carrying amount of land Gain on reclassification P15,000,000 10,000,000 P5,000,000 Reference: Intermediate Accounting Volume 1 2019, C. Valix, p. 571 Problem 4 Chain Company has P5,000,000 life insurance policy on the president, of which Chain Company is the beneficiary. The entity provided the following information regarding the policy for the year ended December 31, 2019: Cash surrender value, January 1 Cash surrender value, December 31 Annual advance premium paid January 1 435,000 540,000 200,000 During the current year, dividends of P30,000 were applied to increase the cash surrender value of the policy. What amount should be reported as life insurance expense for 2019? A. 200,000 B. 125,000 C. 65,000 D. 95,000 Answer: D Premium paid Less: Increase in cash surrender value (540,000 – 435,000) Life insurance expense P200,000 105,000 P95,000 Reference: Intermediate Accounting Volume 1 2019, C. Valix, p. 574 Problem 5 During the year, Storm Company purchased a new machine. A P120,000 down payment was made and three monthly instalments of P360,000. The cash price would have been P1,160,000. The entity paid no installation charges under the monthly payment plan but a P20,000 installation charge would have been incurred with a cash purchase. What amount should be capitalized as cost of the machine? A. 1,220,000 B. 1,200,000 C. 1,180,000 D. 1,160,000 Answer: C Cash paid Directly attributable cost Capitalized cost of the machine P1,160,000 20,000 P1,180,000 Reference: Intermediate Accounting Volume 1 2019, C. Valix, p. 656 Problem 6 Grey Company acquired a machine with a cash price of P2,000,000. Down payment Note payable in 3 equal annual instalments 20,000 shares of Grey Company at fair value Prior to use, installation cost of P50,000 was incurred machine has a residual value of P100,000. What is the initial measurement of the new machine? A. 2,000,000 B. 2,400,000 C. 2,050,000 D. 2,450,000 Answer: C Cash price Installation cost Total cost P 2,000,000 50,000 P 2,050,000 Reference: Intermediate Accounting Volume 1 2019, C. Valix, p.656 Problem 7 Corner Company purchased a van with a list price of P3,000,000. The dealer granted a 15% reduction in list price and an additional 10% cash discount on the net price if payment is made in 30 days. Irrecoverable taxes amounted to P40,000 and the entity paid an extra P30,000 to have a special horn installed. What amount should be recorded as initial cost of the van? A. 2,550,000 B. 2,335,500 C. 2,365,000 D. 2,325,000 Answer: C List price Trade discount (3,000,000 x 15%) Cash discount (3,000,000 – 450,000 x 10%) Irrecoverable taxes Installation cost Total cost P 3,000,000 450,000 255,000 40,000 30,000 P 2,365,000 Reference: Intermediate Accounting Volume 1 2019, C. Valix, p.656 Problem 8 Lax Company recently acquired two items of equipment. Acquired a press at an invoice price of P3,000,000 subject to a 5% cash discount which was taken. Costs of freight and insurance during shipment were P50,000 and installation cost amounted to P200,000. Acquired a welding machine at an invoice price of P2,000,000 subject to a 10% cash discount which was not taken. Additional welding supplies were acquired at a cost of P100,000. What is the total increase in the equipment account as a result of the transactions? A. 4,900,000 B. 5,000,000 C. 5,100,000 D. 5,200,000 Answer: A First equipment: Invoice price Discount taken – 5% Freight and insurance Installation cost P3,000,000 (150,000) 50,000 200,000 P3,100,000 Second equipment: Invoice price Discount taken – 10% 2,000,000 (200,000) 1,800,000 Total cost P4,900,000 Reference: Intermediate Accounting Volume 1 2019, C. Valix, p. 658 Problem 9 At the beginning of the current year, Hallmark Company exchanged an old packaging machine, which cost P1,200,000 and was 50% depreciated, for a used machine and paid a cash difference of P160,000. The fair value of the old packaging machine was determined to be P700,000. 1) What is the cost of the new asset acquired? A. 700,000 B. 860,000 C. 660,000 D. 600,000 2) What is the gain on exchange? A. 540,000 B. 100,000 C. 60,000 D. 0 Question 1 Answer: B Fair value of asset given Cash payment Total cost P700,000 160,000 P860,000 Question 2 Answer: B Fair value of asset given Installation cost Total cost P700,000 600,000 P100,000 Reference: Intermediate Accounting Volume 1 2019, C. Valix, p. 659 Problem 10 On June 30, 2014, Louisiana Company reported the following information: Equipment at cost Accumulated depreciation 5,000,000 1,500,000 The equipment was measured using the cost model and depreciated on a straight line basis over a 10year period. On December 31, 2014, the management decided to change the basis of measuring the equipment from the cost model to the revaluation model. The equipment was recorded at fair value of P4,550,000 with remaining useful life of 5 years. Ignoring income tax, what amount should be reported as revaluation surplus on December 31, 2014? A. 1,050,000 B. 1,300,000 C. 1,500,000 D. 2,000,000 Answer: B Cost – June30, 2014 Accumulated depreciation Carrying amount – June 30, 2014 Depreciation from July 1 to December 31, 2014 (5,000,000/10 x 6/12) Carrying amount – December 31, 2014 P5,000,000 (1,500,000) P3,500,000 Fair value – December 31, 2014 Carrying amount – December 31, 2014 Revaluation surplus – December 31, 2014 P4,550,000 3,250,000 P1,300,000 (250,000) P3,250,000 Reference: Practical Accounting Volume One 2014, C. Valix, p. 662 Problem 11 On January 1, 2009, Boston Company purchased a new building at a cost of P6,000,000. Depreciation was computed on the straight line basis at 4% per year. On January 1, 2014, the building was revalued at fair value of P8,000,000. 1. What is the depreciation for 2014? A. 320,000 B. 400,000 C. 100,000 D. 240,000 2. What is the revaluation surplus on December 31, 2014? A. B. C. D. 3,072,000 1,900,000 3,040,000 1,920,000 Question 1 Answer: B Accumulated depreciation (4% x 5 years expired) 20 % List of asset Expired Remaining life Depreciation for 2014 (8,000,000/20) 25 years (5) 20 P400,000 Question 2 Answer: C Fair value Carrying amount P8,000,000 4,800,000 Revaluation surplus – January 1, 2014 Realization in 2014 (3,200,000/20) Revaluation surplus – December 31, 2014 P3,200,000 160,000 P3,040,000 Reference: Practical Accounting Volume One 2014, C. Valix, p. 663 Problem 12 Cynosure Company has an equipment with carrying amount of P1,600,000 on December 31, 2014 after recording depreciation for 2014. The following information is available on December 31, 2014 relative to the equipment: Fair value of similar equipment Discounted future cash flows Undiscounted future cash flows 1,400,000 1,300,000 1,350,000 At what amount should the equipment be reported on December 31, 2014? A. 1,600,000 B. 1,400,000 C. 1,300,000 D. 1,350,000 Answer: B Carrying amount Less: Recoverable amount equal to fair value which is higher than value in use Impairment loss P1,600,000 1,400,000 P200,000 Reference: Practical Accounting Volume One 2014, C. Valix, p.670 Problem 13 On January 1, 2011, Reed Company purchased a machine for P8,000,000 and established an annual depreciation charge of P1,000,000 over an eight-year life. During 2014, after issuing the 2013 financial statements, the entity concluded that the machine suffered permanent impairment of its operational value, and P2,000,000 is a reasonable estimate of the amount expected to be recovered through use of the machine for the period January , 2014 through December 31, 2018. In the December 31, 2014 statement of financial position, what is the carrying amount of the machine? A. 4,000,000 B. 1,000,000 C. 1,600,000 D. 0 Answer: C Recoverable amount - Jan. 1, 2014 Less: Depreciation for 2014 (2,000,000/ 5) Carrying amount – Dec. 21, 2014 P2,000,000 400,00 0 P1,600,000 Reference: Practical Accounting Volume One 2014, C. Valix, p. 680 Problem 14 Gei Company determined that, due to obsolescence, equipment with an original cost of P9,000,000 and accumulated depreciation on January 1, 2014, of P4,200,000 had suffered permanent impairment, and as a result should have a carrying amount of only P3,000,000 as of the beginning of the year. In addition, the remaining useful life of the equipment was reduced from 8 years to 3. In the December 31, 2014 statement of financial position, what amount should be reported as accumulated depreciation? A. 1,000,000 B. 5,200,000 C. 6,000,000 D. 7,000,000 Answer: D Cost Accumulated depreciation – Jan. 1, 2014 Carrying amount – Jan. 1, 2014 Expected recoverable amount Impairment loss P9,000,000 4,200,000 P4,800,000 3,000,000 P1,800,000 Adjusted accumulated depreciation, Jan. 1, 2014 (4,200,000 + 1,800,000) Depreciation for 2014 (3,000,000/ 3) Accumulated depreciation – Dec. 31, 2014 P6,000,000 1,000,000 P7,000,000 Reference: Practical Accounting Volume One 2014, C. Valix, p. 680 Problem 15 One of the cash generating units of sanmig Company is the production of liquor. On December 31, 2014, the entity believed that the assets of the cash generating unit (CGU) are impaired based on an analysis of economic indicators. The assets and liabilities of the cash generating unit at carrying amount on December 31, 2014 are: Cash Account receivable Allowance for doubtful accounts Inventory Property, plant and equipment Accumulated depreciation Goodwill Accounts payable Loans payable 4,000,000 6,000,000 1,000,000 7,000,000 22,000,000 4,000,000 3,000,000 2,000,000 1,000,000 The entity determined that the value in use of the cash generating unit is P30,000,000. The account receivable are considered collectible, except those considered doubtful. 1. What is the impairment loss to be allocated to property, plant and equipment? A. 4,000,000 B. 2,880,000 C. 2,400,000 D. 4,200,000 Answer: B Cash Accounts receivable – net Inventory Property, plant and equipment – net Goodwill Carrying amount of cash generating unit Value in use Impairment loss Impairment loss allocated to goodwill Remaining impairment loss Inventory Property, plant and equipment P4,000,000 5,000,000 7,000,000 18,000,000 3,000,000 P37,000,000 30,000,000 P7,000,000 3,000,000 P4,000,000 Carrying amount P7,000,000 18,000,000 P25,000,000 Fraction 7/25 18/25 Loss P1,120,000 2,880,000 P4,000,000 Reference: Practical Accounting Volume One 2014, C. Valix, p. 690 Problem 16 Liton Company buys and sells securities expecting to earn profits on short-term differences in price. During 2014, Liton Company purchased the following trading securities: Security A B C Fair value Dec. 31, 2014 P 225,000 162,000 678,000 Cost P 195,000 300,000 660,000 Before any adjustments related to these trading securities, Liton Company had net income of P 900,000. 1. What is Liton’s net income after making any necessary trading security adjustments? A. 900,000 B. 810,000 C. 762,000 D. 948,000 2. What would Liton’s net income be if the fair value of security B were P285,000? A. 867,000 B. 900,000 C. 885,000 D. 933,000 Question 1 Answer: B Net income before trading security adjustment Unrealized loss (1,155,000 – 1,065,000) Net income, as adjusted Security A B C Cost P195,000 300,000 660,000 P1,155,000 Fair value December 31, 2014 P225,000 162,000 678,000 P1,065,000 Question 1 Answer: D Net income before trading security adjustment Unrealized loss (1,188,000 – 1,155,000) Net income, as adjusted P900,000 90,00 0 P810,000 P900,000 33,000 P933,000 Security A B C Cost P 195,000 300,000 660,000 P1,155,000 Fair value December 31, 2014 P225,000 285,000 678,000 P1,188,000 Reference: Auditing Problems CPA Examination Reviewer 2014, G. Roque, p. 281 Problem 17 On January 1, 2014, Rambutan Corp, purchased debt securities for cash of P765,540 to be held as financial assets at amortized cost. The securities have a face value of P 600,000, and they mature in 15 years. The securities carry fixed interest of 10% that is receivable semiannually, on June 30 and December 31. The prevailing market interest rate on these debt securities is 7% compounded annually. 1. The carrying value of the debt securities on December 31, 2014, at amortized cost using the effective interest rate method is A. 771,840 B. 759,016 C. 765,540 D. 600,000 2. The interest income to be reported for 2014 using the effective interest rate method is A. 66,524 B. 6,534 C. 60,000 D. 53,476 Question 1 Answer: B Carrying value, Jan. 1, 2014 Amortization of premium, Jan. 1 – June 30: Nominal interest (600,000 x 10% x ½) Effective interest (765,540 x 7% x ½) Carrying value, June 30, 2014 Amortization of premium, July 1 – Dec. 31: Nominal interest Effective interest (762,334 x 7% x ½) Carrying value at amortized cost, Dec. 31, 2014 Question 2 Answer: D Effective interest, Jan. 1 – June 30 Effective interest, July 1 – June 30 Interest income 2014 Reference: P26,794 26,682 P53,476 P765,540 30,000 (26,794) 30,000 (26,682) (3,206) P762,334 3,318 P759,016 Auditing Problems CPA Examination Reviewer 2014, G. Roque, p. 302 Problem 18 CHICO Company purchased the following non-trading equity securities during 2014: Security Cost X Y P450,000 500,000 Fair value December 31, 2014 P500,000 800,000 At initial recognition, Chico classified these securities as at fair value through other comprehensive income. On July 28, 2015, Chico sold all the shares of Security Y for a total of P835,000. As of December 31, 2015, the shares of Security X had a fair value of P200,000 No other activity occurred during 2015 relation to the non-trading equity securities portfolio. 1. What amount should Chico Company report as realized gain in the 2015 income statement? A. 35,000 B. 335,000 C. 300,000 D. 265,000 2. What is the cumulative unrealized gain (loss) to be reported in the statement of changes in equity for 2015? A. 300,000 B. 150,000 C. (300,000) D. (250,000) Question 1 Answer: A Cash proceeds Less: Carrying value of Security Y, Dec.31, 2014 Realized gain on sale P835,000 800,000 P35,000 Question 2 Answer: D Cumulative unrealized gain, Dec. 31, 2014 Unrealized gain related to Security Y Unrealized loss for 2015 – Security X (500,000 – 200,000) Cumulative unrealized loss, Dec. 31, 2015 P350,000 (300,000) (300,000) P(250,000) Reference: Auditing Problems CPA Examination Reviewer 2014, G. Roque, p. 303 Problem 19 Saxophone Company acquires a new manufacturing equipment on January 1, 2014, on instalment basis. The deferred payment contract provides for a down payment of P300,000 and an 8-year note for P3,104,160. The note is to be paid in 8 equal annual instalment payments of P388,020, including 10% interest. The payments are to be made on December 31 of each year, beginning December 31, 2014. The equipment has a cash price equivalent of P2,370,000. Saxophone’s financial year-end is December 31. 1. What is the acquisition cost of the equipment? A. 3,404,160 B. 2,804,160 C. 2.370,000 D. 3,104,160 2. The amount to be recognized on January 1, 2014, as discount on note payable is A. 1,034,160 B. 310,416 C. 827,160 D. 0 Question 1 Answer: C Acquisition cost of equipment (cash price equivalent) P2,370,000 Question 2 Answer: A Cost of equipment (cash price equivalent) Less: Down payment Amount assigned to note payable Face value of note Discount on note payable, Jan. 1, 2014 P2,370,000 300,000 P2,070,000 3,104,160 P1,034,260 Reference: Auditing Problems CPA Examination Reviewer 2014, G. Roque, p. 350 Problem 20 ACCORDIAN Company incurred the following expenditures in 2014: Purchased of land P7,892,000 Land survey 104,000 Fees for search of title for land 12,000 Building permit fee 70,000 Temporary quarters for construction crews 215,000 Cost to demolish old building 940,000 Excavation of basement 200,000 Special assessment for street project 40,000 Dividends 100,000 Damages awarded for injuries sustained in construction (no insurance carried) 168,000 Cost of construction 58,000,000 Cost of paving parking lot adjoining building 800,000 Cost of shrubs, trees, and other landscaping 660,000 A portion of the building site had been temporarily used by Accordian to operate a car park while the building was being constructed. A total of P325,000 was earned by Accordian from this incidental activity. 1. What is the cost of the land? A. 8,896,000 B. 8,048,000 C. 9,648,000 D. 10,448,000 2. What is the cost of the land improvements? A. 660,000 B. 1,500,000 C. 1,460,000 D. 800,000 3. What is the cost of the building? A. 58,485,000 B. 58,160,000 C. 58,252,000 D. 59,425,000 Question 1 Answer: B Question 2 Answer: C Question 3 Answer: D Land Purchased of land Land survey Fees for search of title for land Building permit fee Temporary quarters for construction crews Cost to demolish old building Excavation of basement Special assessment for street project Cost of construction Cost of paving parking lot adjoining building Cost of shrubs, trees, and other landscaping Totals Land improvements Building P7,892,000 104,000 12,000 P70,000 215,000 940,000 200,000 40,000 58,000,000 P800,000 P8,048,000 660,000 P1,460,000 P59,425,000 Reference: Auditing Problems CPA Examination Reviewer 2014, G. Roque, p. 366 Problem 21 Sheng Company constructed a building for use by the administration section of the company. The completion date was January 1, 2007, and the construction cost was P16,800,000. The company expected to remain in the building for the next 20 years, at which time the building would probably have no real salvage value and have to be demolished. It is expected that demolition costs will amount to P300,000. In June 2013, following a storm that wreaked vast destruction in the city, the roof of the administration building was considered to be in porr shape so the company decided to replace it. On January 1, 2014, a new roof was installed at a cost of P4,400,000. The new roof was of a different material to the old roof, which was estimated to have cost only P2,800,000 in the original construction, although at the time of construction it was thought that the roof would last for the 20 years that the company expected to use the building. Because the company had spent the money replacing the roof, it thought that it would delay construction of a new building, thereby extending the original life of the building from 20 years to 25 years. 1. If the roof were treated as a separate component of the building, the total depreciation expense for 2014 would be A. 750,000 B. 681,566 C. 606,667 D. 672,000 2. If the roof were not treated as a separate component of the building, the total depreciation expense for 2014 would be A. 1,178,462 B. 861,944 C. 851,111 D. 750,000 Question 1 Answer: A Roof (4,400,000/ 18 years) Rest of the building: Cost Less: Accumulated depreciation (14,000,000 x 7/ 20) Book value, Jan. 1, 2014 Divide by revised remaining life (25-7) Total P244,444 14,000,000 4,900,000 9,100,000 18 yrs 505,556 P750,000 Question 2 Answer: C Book value of building, Jan. 1, 2014 (16,800,000 x 13/ 20) Add: Cost of new roof Total Divide by revised remaining life (25 - 7) Depreciation expense for 2014 P10,920,000 4,400,000 15,320,000 18 yrs P851,111 Reference: Auditing Problems CPA Examination Reviewer 2014, G. Roque, p. 399 Problem 22 Eagle Company owns a tract of land that it purchased for P2,000,000. The land is held as a future plant site and has a fair value of P2,800,000 on the date of exchange. Hall Company also owns a tract of land held as a future plant site. Hall paid P3,600,00 for the land upon purchase and the land has a fair value of P3,800,00 on the date of exchange. On date of exchange, Eagle exchanged its land and paid P1,000,000 cash for the land owned by Hall. The configuration of cash flows from land acquired is expected to be significantly different from the configuration of cash flows of the land exchanged. At what amount should Eagle record the land acquired in the exchange? A. 2,800,000 B. 3,000,000 C. 3,200,000 D. 3,800,000 Answer: D Fair value Cash paid Land acquired in the exchange P2,800,000 1,000,000 P3,800,000 Reference: Conceptual Framework and Accounting Standards 2018, C. Valix, p. 299 Problem 23 Yola Company and Zaro Company are fuel distributors. To facilitate the delivery of oil to their customers, Yola and Zaro exchanged ownership of 1,200 barrels of oil without physically moving the oil. Yola paid Zaro P300,000 to compensate for a difference in the grade of oil. It is reliably determined that the exchange lacks commercial substance. On he date of the exchange, carrying amount and market value of the oil were: Carrying amount Market Value Yola Company 1,000,000 1,200,000 Zaro Company 1,400,000 1,500,000 What amount should Yola Company record as cost of the oil inventory received in exchange? A. 1,000,000 B. 1,300,000 C. 1,200,000 D. 1,500,000 Answer: B Carrying amount Cash paid Cost of the oil inventory received in exchange P1,000,000 300,000 P1,300,000 Reference: Conceptual Framework and Accounting Standards 2018, C. Valix, p. 300 Problem 24 Galore Company ventured into construction of a condominium in Makati which is rated as the largest state-of-the-art structure. The board of directors decided that instead of selling the condominium, the entity would hold this property for purposes of earning rentals by letting out space to business executive in the area. The construction of the condominium was completed and the property was placed in service on January 1, 2018. The cost of the construction was P50,000,000. The useful life of the condominium is 25 years and the residual value is P5,000,000. An independent valuation expert provided the following fair value at each subsequent year-end: December 31, 2018 December 31, 2019 December 31, 2020 55,000,000 53,000,000 60,000,000 1. Under the cost model, what amount should be reported an annual depreciation of investment property? A. 1,800,000 B. 2,000,000 C. 2,200,000 D. 0 2. Under the fair value model, what amount should be recognized as gain from change in fair value in 2020? A. 5,000,000 B. 3,000,000 C. 7,000,000 D. 0 Question 1 Answer: A Cost of the construction Less: Residual value Divide by useful life Depreciation expense P50,000,000 5,000,000 25 years P1,800,000 Question 2 Answer: C Fair value - December 31, 2020 Carrying amount - December 31, 2019 Gain from change in fair value P60,000,000 53,000,000 P7,000,000 Reference: Conceptual Framework and Accounting Standards 2018, C. Valix, p. 560 Problem 25 Eragon Company and its subsidiaries own the following properties at year-end: Land held by Eragon for undetermined use A vacant building owned by Eragon and to be leased out under an operating lease Property held by a subsidiary of Eragon, a real estate firm, in the ordinary course of business 5,000,000 3,000,000 2,000,000 Property held by Eragon for use in production Building owned by a subsidiary of Eragon and for which the subsidiary provides security and maintenance services to the lessees Land leased by Eragon to a subsidiary under an operating lease Property under construction for use as investment Property Land held for factory site Machinery leased out by Eragon to an unrelated party under an operating lease 4,000,000 1,500,000 2,500,000 6,000,000 3,500,000 1,000,000 1. What is the total investment property that should be reported in the consolidated statement of financial position of the parent and its subsidiaries? A. 12,000,000 B. 15,500,000 C. 10,500,000 D. 9,500,000 2. What total amount should be included in property, plant and equipment in the consolidated statement of financial position? A. 11,000,000 B. 13,000,000 C. 10,500,000 D. 8,500,000 Question 1 Answer: B Question 2 Answer: A Investment property Land held by Eragon for undetermined use A vacant building owned by Eragon and to be leased out under an operating lease Property held by Eragon for use in production Building owned by a subsidiary of Eragon and for which the subsidiary provides security Land leased by Eragon to a subsidiary under an operating lease Property under construction for use as investment property Land held for factory site Machinery leased out by Eragon to an unrelated party under an operating lease Totals Property, plant and equipment P5,000,000 3,000,000 P4,000,000 1,500,000 2,500,000 6,000,000 3,500,000 P15,500,000 1,000,000 P11,000,000 Reference: Conceptual Framework and Accounting Standards 2018, C. Valix, p. 561 Problem 26 Bona Company purchased an investment property on January 1, 2016 for P2,200,000. The property had a useful life of 40 years and on December 31, 2018 had a fair value of P3,000,000. On December 31, 2018 the property was sold for net proceeds of P2,900,000. The entity used the cost model to account for the investment property. What is the gain or loss to be recognized for the year ended December 31, 2018 regarding the disposal of the property? A. 865,000 gain B. 810,000 gain C. 100,000 loss D. 700,000 gain Answer: A Cost – Jan. 1, 2016 Accumulated depreciation (2,200,000/ 40 x 3) Carrying amount – Dec. 31, 2019 P2,200,000 Sale price Carrying amount Gain on disposal P2,900,000 2,035,000 P865,000 (165,000) P2,035,000 Reference: Conceptual Framework and Accounting Standards 2018, C. Valix, p. 562 Problem 27 Dayara Company owned three investment properties with the following details: Initial cost Property 1 Property 2 Property 3 2,700,000 3,450,000 3,300,000 Fair value Fair value December 31, 2018 December 31, 2019 3,200,000 3,050,000 3,850,000 3,500,000 2,850,000 3,600,000 Each property was acquired three years ago with a useful life of 25 years. The accounting policy is to use the fair value model for investment property. What is the gain or loss to be recognized for the year ended December 31, 2020? A. 189,000 loss B. 150,000 loss C. 300,000 gain D. 450,000 loss Answer: B Property 1 Fair value December 31, 2018 3,200,000 Fair value December 31, 2019 3,500,000 Gain (loss) P300,000 Property 2 Property 3 3,050,000 3,850,000 2,850,000 3,600,000 (200,000) (250,000) Net loss from change in fair value P(150,000) Reference: Conceptual Framework and Accounting Standards 2018, C. Valix, p. 562 Problem 28 Baguio Company is considering the appropriate classification of the following items: a. Land held for long-term capital appreciation b. Land held for undecided future use c. Building leased out under an operating lease d. Building leased out under a finance lease e. Vacant building held to be leased out under an operating lease f. Property held for use in the production or supply of goods or services g. Property held for administrative purposes h. Property held for sale in the ordinary course of business i. Property held in the process of construction or development for sale j. Property being constructed or developed on behalf of third parties k. Property held for future use as owner-occupied property l. Property held for future development and subsequent use as owner-occupied property m. Property occupied by employees n. Owner-occupied property awaiting disposal o. Property that is being constructed or developed for use as an investment property p Existing investment property that is being redeveloped for continuing use as investment property q. Building held for administrative purposes and leased out under operating lease (40% is for administrative purposes) r. Building leased out under an operating lease (the entity supplies security and maintenance services to the lessees) P10,000,000 20,000,000 50,000,000 30,000,000 5,000,000 4,000,000 6,000,000 1,000,000 2,000,000 8,000,000 2,500,000 3,000,000 2,400,000 500,000 7,000,000 15,000,000 10,000,000 24,000,000 How much is total amount that would normally be reported as investment property? A. 130,000,000 Land held for long-term capital appreciation P10,000,000 B. 128,000,000 Land held for undecided future use 20,000,000 C. 137,000,000 Building leased out under an operating lease 50,000,000 D. 106,000,000 Vacant building held to be leased out under an operating lease 5,000,000 Answer: C Property that is being constructed or developed for use as an investment property 7,000,000 Existing investment property that is being redeveloped for continuing use as investment property 15,000,000 Building held for administrative purposes and leased out under operating lease (10,000,000 x 60%) 6,000,000 Building leased out under an operating lease (the entity supplies security and maintenance services to the lessees) 24,000,000 Total P137,000,000 Reference: Reviewer in Auditing Problems 2010, R. Ocampo, p. 299 Problem 29 Alaminos Inc. completedthe construction of a building at the end of 2008 for a total cost of P100 million. The building is estimated to be economically useful for 25 years. The building was constructed for the purpose of earning rentals under operating leases. The tenants began occupying the building after its completion. The company opted to use the fair value model to measure the building. An independent valuation expert was used by the company to estimate the fair value of the building on an annual basis. According to the expert the fair values of the building at the end of 2008, 2009, and 2010 were P105 million, P120 million and P118 million, respectively. 1. How much should be recognized in profit or loss in 2008 as a result of the completion of the building at the end of 2008? A. 20,000,000 B. 9,000,000 C. 5,000,000 D. 0 2. The depreciation expense in 2009 is A. 4,000,000 B. 4,800,000 C. 4,200,000 D. 0 3. How much shoud be recognized in profit or loss in 2009 as a result of the fair value changes? A. 20,000,000 B. 19,200,000 C. 15,000,000 D. 0 4. How much should be recognized in profit or loss in 2010 as a result of the fair value changes? A. 18,000,000 B. 3,000,000 C. 2,000,000 D. 0 5. How much is the carrying amount of the shopping mall on December 31, 2010 if Alaminos used the cost model? A. 100,000,000 B. 118,000,000 C. 96,600,000 D. 92,000,000 Question 1 Answer: C Fair value - December 31, 2008 Cost Unrealized gain on investment property P105,000,000 100,000,000 P5,000,000 Question 2 Answer: D Investment properties carried at fair value are not depreciated since fair value changes are already recognized in profit or loss. Question 3 Answer: C Fair value - December 31, 2009 Fair value - December 31, 2008 Unrealized gain on investment property P120,000,000 105,000,000 P15,000,000 Question 4 Answer: C Fair value - December 31, 2010 Fair value - December 31, 2000 Unrealized loss on investment property P118,000,000 120,000,000 P2,000,000 Question 5 Answer: D Cost Less: Accumulated depreciation – December 31, 2010 (100,000,000 x 2/25) Carrying amount – December 31, 2010 P100,000,000 8,000,000 P92,000,000 Reference: Reviewer in Auditing Problems 2010, R. Ocampo, p. 301 Problem 30 Candon, Inc. completed the construction of a building at the end of 2008 for a total cost of P20 million. The building is estimated to be economically useful for 25 years. The building was constructed for the purpose of earning rentals under operating leases. The tenants began occupying the building after its completion. The company opted to use the fair value model to measure the building. An independent valuation expert was used by the company to estimate the fair value of the building on an annual basis. According to the expert the fair value of the building at the end of 2008, 2009, and 2010 were P22 million, P24 million and P25 million, respectively. The company’s business expanded in 2009. As a result, the company started to use the building in its operations on January 1, 2010. Because of the change in use, the company reclassified the building from investment property to property, plant and equipment. How much is the carrying amount of the building on December 31, 2010? A. 24,000,000 B. 23,040,000 C. 23,000,000 D. 21,120,000 Answer: C Fair value - December 31, 2009 Less: Accumulated depreciation – December 31, 2010 (24,000,000 x 1/24) Carrying amount – December 31, 2010 Reference: Reviewer in Auditing Problems 2010, R. Ocampo, p. 304 P24,000,000 1,000,000 P23,000,000