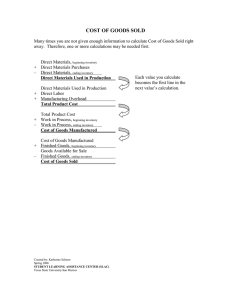

ACCT2200 Principles of Accounting II Managerial Accounting COURSE OVERVIEW Required Textbook Whitecotton, Libby, and Phillips. Managerial Accounting, 5th Edition (McGraw-Hill). ▪ Assessment Participation 6% Assignments 9% Midterm 1 (Chap 1-4; 19:00-20:30, Feb 29) 20% Midterm 2 (Chap 5-7; 19:00-20:30, Mar 26) 15% Final (Chap 1-11) 50% Total: 100% ▪ Participation: active in-class participation ▪ If you miss a midterm exam due to extenuating circumstances, the weight of that midterm exam will be reassigned to the final exam. ▪ Exam arrangement is subject to changes; ▪ Communications ▪ Use Piazza as the primary communication platform (https://piazza.com/school-search or directly through Canvas) ▪ A student can post anonymously/publicly to all ▪ (not required) providing high-quality answers to other students’ questions will be awarded bonus marks for participation. ▪ Tell me about yourself ▪ Which major are you pursuing? A. Accounting B. Finance C. Other SBM majors rather than accounting and finance D. Non-SBM majors ▪ Tell me about yourself ▪ What is your financial accounting background? A. I have taken ACCT 2010 or its equivalent. B. I have not taken ACCT 2010, but I learned some financial accounting in high school. C. I have not taken ACCT 2010, but I am taking a financial accounting course this term. D. I have zero exposure to financial accounting. CHAPTER 1 CHAPTER 1 Introduction to Managerial Accounting Financial Accounting: External users Ray Dalio, founder of the hedge fund Bridgewater Associates. Image Credits: Bridgewater Associates Managerial Accounting: Internal users Steve Jobs, founder of Apple Image Credits: AP Financial Accounting: Follow accounting standards US GAAP (Generally Accepted Accounting Principles) Managerial Accounting: Internal reports Financial Accounting: Objective, reliable, historical Managerial Accounting: Subjective, future-oriented Financial Accounting: Periodic reports Managerial Accounting: Prepared as needed Zara’s growth story Tesla’s financials reports (from Yahoo Finance) Financial Accounting: Report the whole company Starbucks, the parent company Managerial Accounting: Report at the decision level Starbucks at HKUST COMPARISON OF FINANCIAL AND MANAGERIAL ACCOUNTING Which of the following best describes the function of managerial accounting within an organization? A)It places more emphasis on precision of data than financial accounting does. B)It focuses on the organization as a whole, rather than on the organization's segments. C)It has its primary emphasis on the future. D)It is required by regulatory bodies such as the Securities and Futures Commission. Implement Plan Control Plan: set goals (i.e., budget) Implement: put the plan into action Control: compare the actual and planned results; take corrective actions if necessary (i.e., variance analysis) Which activities can be classified as planning, implementing, or controlling? 1-16 ▪ Manufacturers TYPES OF ORGANIZATIONS ▪ Merchandisers ▪ wholesalers ▪ retailers ▪ Service companies Which of the following businesses is a retailer? A. Coke cola B. Fusion supermarket located in HKUST C. HKUST’s clinic D. HKUST’s Canteen 2 1-18 Which of the following statement is true about Apple ? A. B. C. D. it’s a manufacturer. It’s a service firm. It’s a retailer. It’s a wholesaler. 1-19 How does Apple officially describe its business? https://www.sec.gov/ix?doc=/Archives/edgar/data/3 20193/000032019322000108/aapl-20220924.htm 1-20 Define and give examples of different types of costs Direct or Indirect Manufacturing or Nonmanufacturing Product or Period Variable or Fixed Relevant or Irrelevant Direct Costs Indirect Costs Costs that can be Costs that cannot be easily and conveniently traced to a unit of product or other cost object. easily and conveniently traced to a unit of product or other cost object. Name and Tell Look around. Find one object in your room. Name one direct cost and one indirect cost of making it and delivering it to the end customer (you). DIRECT MATERIALS ▪ Direct materials are major material inputs that can be directly and conveniently traced to the product. DIRECT LABOR Direct labor is the cost of labor that can be directly and conveniently traced to the product. “Touch labor” MANUFACTURING OVERHEAD All costs other than direct materials and direct labor that must be incurred to manufacture a product. Indirect labour Indirect materials Amortization on factory buildings, insurance, taxes, maintenance on factory facilities Which of the following is an indirect cost of manufacturing a table made of wood and glass for a firm that manufactures furniture? A. The cost of the wood in the table. B.The cost of the labor used to assemble the table. C.The cost of the glass in the table. D. The cost of rent on the factory where the table is manufactured. MANUFACTURING VERSUS NONMANUFACTURING COSTS Manufacturing Costs Direct Labor Direct Materials Prime Cost Manufacturing Overhead Conversion Cost Elon Musk’s idiot index of manufacturing cost 𝐈𝐝𝐢𝐨𝒕 𝒊𝒏𝒅𝒆𝒙 = 𝑪𝒐𝒔𝒕 𝒐𝒇 𝒂 𝒇𝒊𝒏𝒊𝒔𝒉𝒆𝒅 𝒑𝒓𝒐𝒅𝒖𝒄𝒕 𝑪𝒐𝒔𝒕 𝒐𝒇 𝒓𝒂𝒘 𝒎𝒂𝒕𝒆𝒓𝒊𝒂𝒍𝒔 Direct materials=20 Direct labor=30 Indirect materials=10 Indirect labor=10 Other MOH=40 Total manufacturing cost? Idiot index? 1-29 Manufacturing Cost Flows Manufacturer Current Assets Cash Receivables Prepaid Expenses Inventories • Raw Materials • Work in Process • Finished Goods Manufacturing Cost Flows Manufacturer Current Assets Cash Materials purchased from Receivables suppliers but not yet used in production Prepaid Expenses Inventories Partially complete products • Raw Materials • Work in Process • Finished Goods Products completed but not sold. Manufacturing Cost Flows Inventory Equation + Beginning balance + Additions to inventory = Ending balance + Withdrawals from inventory Manufacturing Cost Flows Inventory Equation in the T-account Inventory Debit Credit (a)Beginning balance (b)Additions (c)Withdrawals (d)Ending balance (a)+(b)-(c) =(d) (a)+(b)=(c) +(d) Manufacturing Cost Flows Inventory Equation If your inventory balance at the beginning of the month was $1,000, you bought $100 during the month, and sold $200 during the month, what would be the balance at the end of the month? A. $1,000. B. $ 900. C. $1,200. D. $ 200. Manufacturing Cost Flows Raw Materials + = – = Beginning raw materials inventory Raw materials purchased Raw materials available for use in production Ending raw materials inventory Raw materials used in production Manufacturing Costs Work In Process Direct materials As raw materials are put into the production, they are called direct materials. Manufacturing Cost Flows Raw Materials + = – = Beginning raw materials inventory Raw materials purchased Raw materials available for use in production Ending raw materials inventory Raw materials used in production Manufacturing Costs Direct materials + Direct labour + MOH = Total manufacturing costs Work In Process Conversion costs incurred to convert the direct material into a finished product. Manufacturing Cost Flows Raw Materials + = – = Beginning raw materials inventory Raw materials purchased Raw materials available for use in production Ending raw materials inventory Raw materials used in production Manufacturing Costs Direct materials + Direct labour + MOH = Total manufacturing costs Work In Process Beginning work in process inventory + Total manufacturing costs = Total work in process for the period All manufacturing costs during the period are added to the beginning balance of WIP inventory. Manufacturing Cost Flows Raw Materials Beginning raw materials inventory + Raw materials purchased = Raw materials available for use in production – Ending raw materials Once inventory the goods are = Raw materials used manufacturing costs in production Manufacturing Costs Work In Process Direct materials + Direct labour + Mfg. overhead = Total manufacturing costs Beginning work in process inventory Total manufacturing costs Total work in process for the period Ending work in process inventory Cost of goods manufactured completed, total during the period (COGM) are transferred to finished goods inventory. + = – = Manufacturing Cost Flows Work In Process + = – = Beginning work in process inventory Manufacturing costs for the period Total work in process for the period Ending work in process inventory Cost of goods manufactured Finished Goods Beginning finished goods inventory + Cost of goods manufactured = Cost of goods available for sale - Ending finished goods inventory Cost of goods sold MANUFACTURING VERSUS NONMANUFACTURING COSTS Nonmanufacturing Costs Marketing or Selling Costs General and Administrative Costs Costs necessary to get the order and deliver the product All executive, organizational, and clerical costs PERIOD COSTS VERSUS PRODUCT COSTS Product Costs: costs that are assigned to the product as it is being manufactured. “Inventoriable costs” → accumulate in inventory Matching principle Period Costs: nonmanufacturing costs. Expensed in the period incurred. Matching principle not involved. PRODUCT VERSUS PERIOD COSTS Beginning balance of raw materials inventory was $30,000. $270,000 of raw material was purchased during the quarter. There were $28,000 raw materials remaining at the end of the month. What is the cost of raw materials used? A.$276,000 B.$272,000 C.$280,000 D.$ 2,000 Direct materials used in production totaled $200,000. During the month, direct labor was $395,000 and manufacturing overhead was $180,000. What were total manufacturing costs? A. B. C. D. $568,000 $775,000 $415,000 $798,000 The beginning balance of work in process inventory was $225,000. The total manufacturing costs incurred for the month were $875,000. A count of work in process inventory at the end of the month revealed that $150,000 of partially finished goods remaining. What was the cost of goods manufactured during the month? A. B. C. D. $1,160,000 $ 950,000 $ 765,000 Cannot be determined. Variable costs change, in total, in direct proportion to changes in activity level. VARIABLE VERSUS FIXED COSTS Fixed costs VARIABLE VERSUS FIXED COSTS Two mobile plans: (1) Monthly plan: $ 64 per month (2) Daily plan: $ 4 per day, assuming 30 days in a month “Monthly Plan”: Cost per day for 20 days? 16 days? 64/16=$4.00 “Daily Plan”: Cost per day for 20 days? 16 days? $64you be indifferent? When would $4*16=$64 Out-of-pocket costs involve an actual outlay of cash. An opportunity cost is the foregone benefit (or lost opportunity) of the path not taken. • Company A produces furniture, including tables. It generates $400,000 revenues per year from table sales and the cost of manufacturing tables is $350,000 per year. Alternatively, it can rent the factory space for $100,000 per year. What is the opportunity cost of producing tables? • A relevant cost has the potential to influence a RELEVANT VERSUS IRRELEVANT COSTS decision. • Otherwise irrelevant cost • For a cost to be relevant, it must: 1. Differ between the decision alternatives. • incremental or differential costs. 2. Be incurred in the future rather than the past. • sunk costs(historical and cannot be recovered) Summary of Types of Cost Classification ➢ Assigning costs to cost objects • (Direct costs vs. Indirect costs) ➢ Financial Reporting • • Direct materials, direct labor, manufacturing overhead Period costs versus product costs ➢ Cost behavior • Variable costs versus fixed costs ➢ Decision making • • Out-of-pocket costs versus opportunity costs Relevant costs Case study: truth about working at a law firm Imagine that you strive to become a lawyer. Most law firms bill their clients by the hour. Survey shows that in the U.S., the “target” billable hours typically range between 1,700 and 2,300. Case study: truth about working at a law firm Class of 2019 Salary: https://law.yale.edu/student-life/career-development/employment-data/class-2019-employment (1) What’s your hourly wage if you work the target billable hours(1,832) at a firm(use the business salary)? (2) What’s your hourly wage if you work the target billable hours (1,832) for the government? Case study: truth about working at a law firm Class of 2019 Salary: https://law.yale.edu/student-life/career-development/employment-data/class-2019-employment (3) Suppose you are a business manager who would like to hire lawyers.You expect your employees to work the target 1,832 billable hours (2,420 total working hours) and will pay them the business wage. How much of the wage expense is indirect labor cost? How much of the wage expense is direct labor cost?