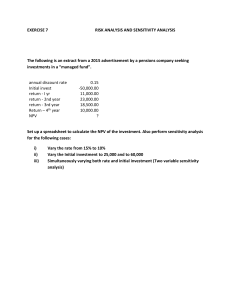

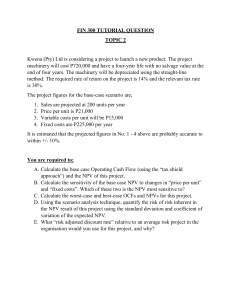

FINANCIAL MANAGEMENT Tools for Project Analysis PROJECT ANALYSIS INTRODUCTION TO PROJECT ANALYSIS Senior management and the challenge of identifying the set of projects to invest in Consistency in the assessment of projects Develop plans and budget for capital investments Authorize specific projects Check whether projects perform as promised Do not accept the project’s cash flow forecast at face value Uncertain tomorrow: input costs and output prices and hence cashflow Project Analysis Know the danger signals and the actions that you might take Sensitivity Analysis Scenario Analysis Break-even Analysis Monte Carlo Simulation Real Options approach to Capital Investments THE CAPITAL INVESTMENT PROCESS Capital Budget Preparation of annual capital budget: List of investment projects under consideration by a firm Bottom up approach vs Top down approach Capital budgeting vs Strategic planning Starts with consensus forecast of economic indicators such as inflation, growth in national income Project authorization and the problem of biased forecast Understatement of project risk: often on account of overconfidence/over-optimism Do not add fudge factors to cost of capital Postaudit Review of project to see if it met forecasts Helps management in review of next set of requests for capital investment TYPES OF ANALYSIS Sensitivity Analysis Analyzes effects of changes in sales, costs, etc., on project Scenario Analysis Project analysis, given a particular combination of assumptions Simulation Analysis Estimates probabilities of different outcomes Break Even Analysis Level of sales (or other variables) at which the project breaks even SENSITIVITY ANALYSIS SENSITIVITY ANALYSIS Scenario: As a treasurer of Otobai Company, Osaka, Japan, you are considering introduction of an electrically powered motor scooter for city use. Year 0 Investment# # Values in billion Japanese Yen Year 1 – 10 15 Revenue 37.5 Variable Costs 30 Fixed Cost 3 Depreciation 1.5 [15/10] Pretax profit 3 Tax @ 50% 1.5 Net Profit 1.5 Operating cash flow 3 Net cash flow -15 3 SENSITIVITY ANALYSIS Scenario: As a treasurer of Otobai Company, Osaka, Japan, you are considering introduction of an electrically powered motor scooter for city use. Required: NPV analysis and sensitivity analysis Given expected cash-flow forecasts for Otobai Company’s Motor Scooter project, determine the NPV of project given changes in cash- flow components using 10% cost of capital. Assume constant variables, except the one you are changing. INPUTS NEEDED FOR PREPARATION OF INCOME STATEMENT FOR SCOOTER PROJECT… INPUTS NEEDED FOR PREPARATION OF INCOME STATEMENT FOR SCOOTER PROJECT… Overall market size of Electrically powered motor scooter New proposed product’s market share Unit price of each scooter Cost structure: variable cost per unit, total fixed cost Depreciation rule Tax rate INCOME STATEMENT - PREPARATION Unit Sales = New product’s share of market (0.1) x Size of Scooter market (1 million units) = 100,000 Revenue = Number of units (100,000) x Price per unit (375,000) = 37.5 billion Variable cost = Number of units (100,000) x Variable cost per unit (300,000) = 30 billion NPV CALCULATION Year 0 Investment# Year 1 – 10 15 Revenue 37.5 Variable Costs 30 Fixed Cost 3 Depreciation 1.5 [15/10] Pretax profit 3 Tax @ 50% 1.5 Net Profit 1.5 Operating cash flow 3 Net cash flow With r = 10%, NPV = +3.43 billion -15 3 SENSITIVITY ANALYSIS Example (Continued) Outcomes Variable Pessimistic Market size .9 mil Expected Optimistic 1.0 mil 1.1 mil Market share Unit price Unit var cost .04 350,000 360,000 .1 375,000 300,000 .16 380,000 275,000 Fixed cost 4 bil 3 bil 2 bil SENSITIVITY ANALYSIS Example (Continued) NPV calculations—Optimistic scenario (Market Size) Year 0 Investment# NPV = +5.7 billion Year 1 – 10 15 Revenue 41.25 Variable Costs 33 Fixed Cost 3 Depreciation 1.5 Pretax profit 3.75 Tax @ 50% 1.875 Net Profit 1.875 Operating cash flow 3.375 Net cash flow -15 3.375 SENSITIVITY ANALYSIS Example (Continued) Possibilities ( Billions ¥) Variable Market size Pessimistic 1.1 Expected Optimistic 3.4 5.7 Market share Unit price Unit var cost - 10.4 - 4.2 - 15.0 3.4 3.4 3.4 17.3 5.0 11.1 Fixed cost 0.4 3.4 6.5 SCENARIO ANALYSIS SCENARIO ANALYSIS: NPV OF ELECTRIC SCOOTER BREAK-EVEN ANALYSIS NPV SCENARIOS: UNDER DIFFERENT ANNUAL SALES BREAK-EVEN CHART Point at which NPV=0 is break-even point Otobai Motors has a break-even point of 85,000 units sold PV (Yen) Billions 400 PV inflows Break-even NPV = 0 PV Outflows 200 19.6 85 200 Sales, thousands ACCOUNTING PROFIT SCENARIOS: UNDER DIFFERENT ANNUAL SALES ACCOUNTING BREAK-EVEN Accounting break-even does not consider the time value of money Otobai Motors has an accounting break-even point of 60,000 units sold Revenues 60 Accounting revenue and costs (Yen) Billions 40 Break -even Profit =0 Costs 20 Sales, thousands 60 200 OPERATING LEVERAGE AND BREAK-EVEN POINT ELECTRIC SCOOTER CASH-FLOW FORECASTS OPERATING LEVERAGE Operating Leverage Degree to which costs are fixed Degree of Operating Leverage (DOL) Percentage change in profits given 1% change in sales DOL = % change in profits % change in sales or fixed costs DOL = 1 + profits OPERATING LEVERAGE Example Using the data from the Otobai scooter project, calculate the DOL (3 + 1.5) DOL = 1 + = 2.5 3 MONTE CARLO SIMULATION MONTE CARLO SIMULATION Modeling Process Step 1: Model Project Step 2: Specify Probabilities Step 3: Simulate Cash Flows Step 4: Calculate Present Value SIMULATION OF CASH FLOWS REAL OPTIONS AND DECISION TREES NPV Analysis REAL OPTIONS AND DECISION TREES Decision Trees Diagram of sequential decisions and possible outcomes Help companies analyze options by showing various choices and outcomes Option to avoid a loss or produce extra profit has value Ability to create option has value that can be bought or sold FEDEX’S EXPANSION OPTION: AN EXAMPLE FEDEX’S EXPANSION OPTION Real Options Option to expand Option to abandon Timing option Flexible production facilities DECISION TREE Phase III Trials and prelaunch, 3 years Phase II Trials, 2 years $700 (.80) - $130 .25 $ 0 (.20) $ 300 (.80) - $18 Invest Yes / No .44 .56 .50 - $130 $0 $ 0 (.20) .25 NPV= ? $ 100 (.80) - $130 $ 0 (.20) DECISION TREE $700 (.80) - $130 .25 560 $ 0 (.20) $ 300 (.80) - $18 Invest Yes / No .44 .56 .50 - $130 $0 $ 0 (.20) .25 NPV= ? 240 $ 100 (.80) - $130 80 $ 0 (.20) DECISION TREE $700 (.80) - $130 .25 560 $ 0 (.20) $ 300 (.80) - $18 Invest Yes / No .44 .56 .50 - $130 $0 $ 0 (.20) .25 NPV= ? 240 $ 100 (.80) - $130 (700 .80) + (0 .20) = 560 80 $ 0 (.20) DECISION TREE NPV = $295 $700 (.80) - $130 .25 Invest Yes / No $ 0 (.20) 560 = 295 3 (1.096) .44 .50 = −130 - $130 NPV (upside) + - $18 .56 $0 $ 300 (.80) 240 $ 0 (.20) .25 NPV= ? 560 $ 100 (.80) - $130 80 $ 0 (.20) DECISION TREE NPV = $295 $700 (.80) - $130 .25 560 $ 0 (.20) $ 300 (.80) - $18 Invest Yes / No .44 .56 .50 - $130 NPV = $52 $0 $ 0 (.20) .25 NPV= ? 240 $ 100 (.80) - $130 NPV = - $69 (do not invest, so NPV = 0) 80 $ 0 (.20) DECISION TREE NPV = $295 $700 (.80) - $130 .25 - $18 Invest Yes / No $ 300 (.80) - $130 NPV = $52 $0 240 $ 0 (.20) (0 .25) + (52 .5) + (295 .25) $2 100 (.80) (1.096) - $130 80 NPV = - $69 = $83 .25 NPV= ? $ 0 (.20) NPV = $83 .44 .50 .56 560 NPV = (do not invest, so NPV = 0) $ 0 (.20) DECISION TREE NPV = $295 $700 (.80) - $130 .25 - $18 Invest Yes / No NPV = $83 .44 .50 .56 $ 0 (.20) $ 300 (.80) - $130 NPV = $52 $0 240 $ 0 (.20) .25 NPV= $19 560 NPV = −18 + (.-44 83) + (.56 0) $130 = $19 NPV = - $69 (do not invest, so NPV = 0) $ 100 (.80) 80 $ 0 (.20) DECISION TREE Phase III Trials and prelaunch, 3 years Phase II Trials, 2 years NPV = $295 $700 (.80) - $130 .25 - $18 Invest Yes / No NPV = $83 .44 .50 .56 $ 0 (.20) $ 300 (.80) - $130 NPV = $52 $0 240 $ 0 (.20) .25 NPV= $19 560 $ 100 (.80) - $130 NPV = - $69 (do not invest, so NPV = 0) 80 $ 0 (.20)