ABC Costing Analysis: Supermercados Morelos Profitability

advertisement

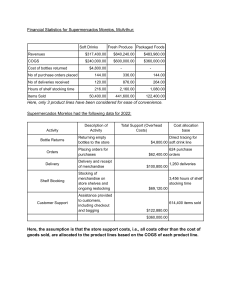

Supermercados Morelos Store, USA ABC Based Costing In partial fulfillment of MANAC-2 taught by Prof Raveesh. By: Group 2 Aarushi Anurag Saxena (MBA/2001/09) Abhishek Kumar (MBA/2002/09) Alisha Anand (MBA/2008/09) Alan Anurag (MBA/2007/09) Vanlalmalsawmdwangagzula (MBA/2092/09) Bharat Sharma (MBA/1219/08) Monika (MBA/2054/09) Akshay Bavisa (MBA/2005/09) Christeena Sunesh (MBA/2025/09) Sachin Kumar (MBA/1264/08) Siddhi Datri (MBA/2086/09) Problem Statement: To maximise the profit of Supermercados Morelos, McArthur uses various accounting methods. Company Background: Grupo Morelos carries the legacy of its founders, The Ibarra Family, who immigrated to the United States in search of better opportunities. In 2003, Grupo Morelos opened its first store in Oklahoma City to offer products that would take Mexicans back to their homeland and strengthen their connection with their heritage. It’s a small store that offers its customers a limited set of products. Financial Statistics for Supermercados Morelos, McArthur: Soft Drinks Fresh Produce Packaged Foods Revenue $317,400.00 $840,240.00 $483,960.00 COGS $240,000.00 $600,000.00 $360,000.00 Cost of bottles returned $4,800.00 - - No of purchase orders placed 144.00 336.00 144.00 No of deliveries received 120.00 876.00 264.00 Hours of shelf stocking time 216.00 2,160.00 1,080.00 50,400.00 441,600.00 122,400.00 Items Sold Here, only 3 product lines have been considered for ease of convenience. Supermercados Morelos had the following data for 2022: Activity Description of Activity Bottle Returns Returning empty bottles to the store Orders Placing orders for purchases Delivery Delivery and receipt of merchandise Shelf Stocking Stocking of merchandise on store shelves and ongoing restocking Customer Support Assistance provided to customers, including checkout and bagging Total Support (Overhead Costs) Cost allocation base Direct tracing for $4,800.00 soft drink line 624 purchase $62,400.00 orders $100,800.00 1,260 deliveries 3,456 hours of shelf stocking time $69,120.00 614,400 items sold $122,880.00 $360,000.00 Here, the assumption is that the store support costs, i.e., all costs other than the cost of goods sold, are allocated to the product lines based on the COGS of each product line. Accounting Methods used: 1. Traditional Costing: Traditional costing is a method used to assign costs to products based on the volume of resources they consume. It relies heavily on allocating overhead costs to products based on a single cost driver, such as direct labor hours or machine hours. This method often simplifies the allocation process but can result in inaccurate product costing, especially in modern manufacturing environments where overhead costs are driven by multiple factors beyond just labor or machine usage. Total store support (overhead costs) = ● ● ● ● ● Cost of bottles returned= Cost of purchase orders= Cost of deliveries= Cost of shelf stocking= Cost of customer support= $360,000 $4,800 $62,400 $100,800 $69,120 $ 122,800 Cost of goods sold= ● Cost of soft drinks= ● Cost of fresh produce= ● Cost of packaged foods= $ 1,200,000 $240,000 $600,000 $360,000 Allocation rate for support (overhead costs)= $360,000/$1,200,000= 30%. Supermercados Morelos Traditional Costing Approach: Soft Drinks Fresh Produce Packaged Foods Revenues $317,400.00 $840,240.00 $483,960.00 COGS $240,000.00 $600,000.00 $360,000.00 $72,000.00 $180,000.00 $108,000.00 $312,000.00 $780,000.00 $468,000.00 $5,400.00 $60,240.00 $15,960.00 1.70% 7.17% 3.30% Total support (overhead) costs- 30% of COGS Total Costs Operating Profits Profit Margin (Operating profit/revenue) The highest profit margin is obtained from fresh produce. Common activities conducted to produce cost objects: Activity Cost Hierarchy 2 Ordering Batch level Delivery Batch level Shelf Stocking Output unit level Customer Support Output unit level Cost driver quantity Cost driver rate 4 5= 3-4 Total costs 3 624 purchase $62,400.00 orders $100,800.00 $100 per purchase order 1,260 deliveries 3,456 hours of $69,520.00 shelf stocking time $122,880.00 614,400 items sold $80 per delivery $20 per shelf stocking hour $0.20 per item sold 2. ABC Costing: Activity-Based Costing (ABC) is a methodology used by businesses to allocate costs more accurately. Instead of lumping costs into broad categories, ABC identifies specific activities that incur costs and links these costs to the products, services, or customers that directly use those activities. Supermercados Morelos ABC Cost based Approach: Soft Drinks Packaged foods Fresh Produce Revenues $317,400.00 $480,240.00 $483,960.00 COGS $240,000.00 $600,000.00 $360,000.00 Cost of bottles returned $4,800.00 $0.00 $0.00 Ordering Costs (144, 136, 144) purchase orders x $100 14,400.00 33,600.00 14,400.00 Delivery Costs (120, 876, 264) deliveries x $80 9,600.00 70,080.00 21,120.00 Shelf stocking costs (216, 2160, 1080) shelf-stocking hours x $20 4,320.00 43,200.00 21,600.00 10,080.00 88,320.00 22,480.00 $283,200.00 $835,200.00 $441,600.00 $34,200.00 $5,040.00 $42,360.00 10.78% 0.60% 8.75% Customer support costs (50400, 441600, 122400) items sold x $0.20 Total Costs Operating profits Profit margin (Operating profits/Revenue) Profitability for Supermercados Morelos under Traditional and ABC Costing Approach: Traditional- Profit margin ABC- profit margin Traditional- operating profit ABC- operating profit Fresh Produce 7.17% 0.60% $5,400.00 $34,200.00 Packaged food 3.30% 8.75% $60,240.00 $5,040.00 Soft drinks 1.70% 10.78% $15,960.00 $42,360.00 $81,600.00 $81,600.00 Total Conclusions from the ABC Approach: 1. Soft drinks provide the highest profit margin and make the most operating profits. 2. Packaged foods provided the second-highest profit margin—lowest operating profits. Explore whether the packaged food market share is expandable.