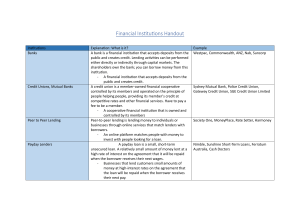

What Are the Three Main Types of Lending? Introduction Lending involves providing funds to individuals, whether men, women, or any other person, with the anticipation of repayment, usually accompanied by interest. It forms the cornerstone of the financial industry, fostering economic activity by extending credit to individuals and organisations, enabling them to access capital. Credit is essential in the global financial system, allowing human beings and corporations to enter capital for various goals. Understanding the easy-to-recognise styles of loans is vital for everyone searching out valuable merchandise in finance or investing in this area. Here, we are going to explore the main types of lending: Secured Lending Borrowers offer collateral as loan security in secured lending. Real estate, vehicles, and other valuable goods might be used as collateral. Interest rates are frequently lower for this type of borrowing because lenders face less risk. Individuals with assets can use secured loans to obtain cheaper interest rates than unsecured loans. Mortgages and auto loans are common examples of secured lending. The advantage for lenders in secured lending is the reduced risk of loss as they have a tangible asset to claim if the borrower defaults. Borrowers, alternatively, run the risk of getting their collateral thrown out in the event of a default. Real property, cars, financial savings loans, and other excessive-fee assets are not unusual sorts of secured loans. Unsecured Lending Unsecured lending, on the other hand, does not require collateral. The creditworthiness and financial history of the borrower are used to determine the loan amount. Personal loans and credit cards are frequent examples. However, because of the greater risk for lenders, they frequently come with higher interest rates. Because security isn't available, lenders just depend on the borrower's word to repay the loan. Because of this, the interest rates on unsecured loans are usually higher to offset the greater risk to lenders. Peer-to-Peer Lending Peer-to-peer lending, commonly called P2P lending, is facilitated by online platforms connecting individual lenders and borrowers. This macroeconomy allows individuals to borrow and lend from each other at once, often bypassing traditional financial institutions in good faith. Borrowers and lenders are primarily matched based on their eligibility and credit score information through a P2P lending platform. Borrowers get lower interest rates than traditional financial institutions, while lenders can earn better rates than savings banks that are commonly used. However, there are such cases through lenders and borrowers, as well as cases of programs or borrowers defaulting on loans, and borrower credit rating checks and fee intervention are essential measures to mitigate those risks. How to Use DataGardener’s Lending Intelligence Tool to Find Prospects DataGardener’s Lending intelligence tool is a valuable resource for lenders, brokers, commercial finance brokers, and real estate professionals looking to gain insights into companies based in the UK. You can easily search for Information based on specific criteria. This enables new possibilities and informed selection-making in today’s dynamic business world. For commercial finance brokers, this tool increases their client base by imparting vital facts about credit scores, income costs, prices, renewal dates, etc. This enables targeted outreach and tailor-made services to fulfil each organisation’s unique needs, ultimately improving productivity. Original Source: Three Main Types of Lending