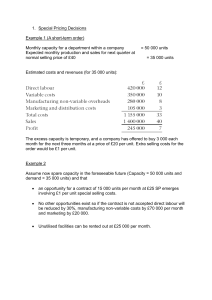

Uploaded by

nirmal shrestha

CIMA C1 Fundamentals of Management Accounting Practice Kit

advertisement