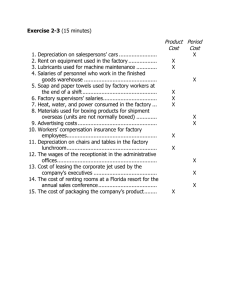

Confirming Pages Managerial Accounting and Cost Concepts 53 Exercises All applicable exercises are available with McGraw-Hill’s Connect™ Accounting. EXERCISE 2–1 Classifying Manufacturing Costs [LO1] Your Boat, Inc., assembles custom sailboats from components supplied by various manufacturers. The company is very small and its assembly shop and retail sales store are housed in a Gig Harbor, Washington, boathouse. Below are listed some of the costs that are incurred at the company. Required: For each cost, indicate whether it would most likely be classified as direct labor, direct materials, manufacturing overhead, selling, or an administrative cost. 1. The wages of employees who build the sailboats. 2. The cost of advertising in the local newspapers. 3. The cost of an aluminum mast installed in a sailboat. 4. The wages of the assembly shop’s supervisor. 5. Rent on the boathouse. 6. The wages of the company’s bookkeeper. 7. Sales commissions paid to the company’s salespeople. 8. Depreciation on power tools. EXERCISE 2–2 Classification of Costs as Period or Product Costs [LO2] Suppose that you have been given a summer job at Fairwings Avionics, a company that manufactures sophisticated radar sets for commercial aircraft. The company, which is privately owned, has approached a bank for a loan to help finance its tremendous growth. The bank requires financial statements before approving such a loan. Required: Classify each cost listed below as either a product cost or a period cost for purposes of preparing the financial statements for the bank. 1. The cost of the memory chips used in a radar set. 2. Factory heating costs. 3. Factory equipment maintenance costs. 4. Training costs for new administrative employees. 5. The cost of the solder that is used in assembling the radar sets. 6. The travel costs of the company’s salespersons. 7. Wages and salaries of factory security personnel. 8. The cost of air-conditioning executive offices. 9. Wages and salaries in the department that handles billing customers. 10. Depreciation on the equipment in the fitness room used by factory workers. 11. Telephone expenses incurred by factory management. 12. The costs of shipping completed radar sets to customers. 13. The wages of the workers who assemble the radar sets. 14. The president’s salary. 15. Health insurance premiums for factory personnel. EXERCISE 2–3 Fixed and Variable Cost Behavior [LO3] Koffee Express operates a number of espresso coffee stands in busy suburban malls. The fixed weekly expense of a coffee stand is $1,100 and the variable cost per cup of coffee served is $0.26. Required: 1. Fill in the following table with your estimates of total costs and average cost per cup of coffee at the indicated levels of activity for a coffee stand. Round off the cost of a cup of coffee to the nearest tenth of a cent. Cups of Coffee Served in a Week Fixed cost . . . . . . . . . . . . . . . . . . . . . . . . . . Variable cost . . . . . . . . . . . . . . . . . . . . . . . . Total cost . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Average cost per cup of coffee served . . . . gar11005_ch02_024-082.indd 53 1,800 1,900 2,000 ? ? ? ? ? ? ? ? ? ? ? ? 02/11/10 4:31 PM Confirming Pages 54 Chapter 2 2. Does the average cost per cup of coffee served increase, decrease, or remain the same as the number of cups of coffee served in a week increases? Explain. EXERCISE 2–4 High-Low Method [LO4] The Edelweiss Hotel in Vail, Colorado, has accumulated records of the total electrical costs of the hotel and the number of occupancy-days over the last year. An occupancy-day represents a room rented out for one day. The hotel’s business is highly seasonal, with peaks occurring during the ski season and in the summer. Month January . . . . . . . . . February . . . . . . . . March . . . . . . . . . . . April . . . . . . . . . . . May . . . . . . . . . . . . June . . . . . . . . . . . July . . . . . . . . . . . . . August . . . . . . . . . September . . . . . . October . . . . . . . . . November . . . . . . . December . . . . . . . OccupancyDays Electrical Costs 2,604 2,856 3,534 1,440 540 1,116 3,162 3,608 1,260 186 1,080 2,046 $6,257 $6,550 $7,986 $4,022 $2,289 $3,591 $7,264 $8,111 $3,707 $1,712 $3,321 $5,196 Required: 1. 2. Using the high-low method, estimate the fixed cost of electricity per month and the variable cost of electricity per occupancy-day. Round off the fixed cost to the nearest whole dollar and the variable cost to the nearest whole cent. What other factors other than occupancy-days are likely to affect the variation in electrical costs from month to month? EXERCISE 2–5 Traditional and Contribution Format Income Statements [LO5] Redhawk, Inc., is a merchandiser that provided the following information: Number of units sold . . . . . . . . . . . . . . . . . . . . . . . . . . . . Selling price per unit . . . . . . . . . . . . . . . . . . . . . . . . . . . . Variable selling expense per unit . . . . . . . . . . . . . . . . . . . Variable administrative expense per unit . . . . . . . . . . . . . . Total fixed selling expense . . . . . . . . . . . . . . . . . . . . . . . . Total fixed administrative expense . . . . . . . . . . . . . . . . . . . Merchandise inventory, beginning balance . . . . . . . . . . . . Merchandise inventory, ending balance . . . . . . . . . . . . . . Merchandise purchases . . . . . . . . . . . . . . . . . . . . . . . . . . 10,000 $15 $2 $1 $20,000 $15,000 $12,000 $22,000 $90,000 Required: 1. 2. Prepare a traditional income statement. Prepare a contribution format income statement. EXERCISE 2–6 Identifying Direct and Indirect Costs [LO6] The Empire Hotel is a four-star hotel located in downtown Seattle. Required: For each of the following costs incurred at the Empire Hotel, indicate whether it would most likely be a direct cost or an indirect cost of the specified cost object by placing an X in the appropriate column. gar11005_ch02_024-082.indd 54 02/11/10 4:31 PM Confirming Pages Managerial Accounting and Cost Concepts Cost Ex. 1. 2. 3. 4. 5. 6. 7. 8. Direct Cost Cost Object Room service beverages The salary of the head chef The salary of the head chef Room cleaning supplies Flowers for the reception desk The wages of the doorman Room cleaning supplies Fire insurance on the hotel building Towels used in the gym A particular hotel guest The hotel’s restaurant A particular restaurant customer A particular hotel guest A particular hotel guest A particular hotel guest The housecleaning department The hotel’s gym The hotel’s gym 55 Indirect Cost X EXERCISE 2–7 Differential, Opportunity, and Sunk Costs [LO7] The Sorrento Hotel is a four-star hotel located in downtown Seattle. The hotel’s operations vice president would like to replace the hotel’s antiquated computer terminals at the registration desk with attractive state-of-the-art flat-panel displays. The new displays would take less space, would consume less power than the old computer terminals, and would provide additional security since they can only be viewed from a restrictive angle. The new computer displays would not require any new wiring. The hotel’s chef believes the funds would be better spent on a new bulk freezer for the kitchen. Required: For each of the items below, indicate by placing an X in the appropriate column whether it should be considered a differential cost, an opportunity cost, or a sunk cost in the decision to replace the old computer terminals with new flat-panel displays. If none of the categories apply for a particular item, leave all columns blank. Differential Opportunity Sunk Cost Cost Cost Item Ex. 1. 2. 3. 4. 5. 6. 7. 8. Cost of electricity to run the terminals . . . . . . . . . . . . . . . Cost of the new flat-panel displays . . . . . . . . . . . . . . . . . Cost of the old computer terminals . . . . . . . . . . . . . . . . . Rent on the space occupied by the registration desk . . . Wages of registration desk personnel . . . . . . . . . . . . . . . Benefits from a new freezer . . . . . . . . . . . . . . . . . . . . . . . . Costs of maintaining the old computer terminals . . . . . . . Cost of removing the old computer terminals . . . . . . . . . Cost of existing registration desk wiring . . . . . . . . . . . . . X EXERCISE 2–8 Cost Behavior; Contribution Format Income Statement [LO3, LO5] Parker Company manufactures and sells a single product. A partially completed schedule of the company’s total and per unit costs over a relevant range of 60,000 to 100,000 units produced and sold each year is given below: Units Produced and Sold gar11005_ch02_024-082.indd 55 60,000 80,000 100,000 Total costs: Variable costs . . . . . . . . . Fixed costs . . . . . . . . . . . Total costs . . . . . . . . . . . . . $150,000 360,000 $510,000 ? ? ? ? ? ? Cost per unit: Variable cost . . . . . . . . . . Fixed cost . . . . . . . . . . . . Total cost per unit . . . . . . . . ? ? ? ? ? ? ? ? ? 02/11/10 4:31 PM Confirming Pages 56 Chapter 2 Required: 1. 2. Complete the schedule of the company’s total and unit costs. Assume that the company produces and sells 90,000 units during the year at the selling price of $7.50 per unit. Prepare a contribution format income statement for the year. EXERCISE 2–9 Cost Classification [LO1, LO2, LO3, LO7] Several years ago Medex Company purchased a small building adjacent to its manufacturing plant in order to have room for expansion when needed. Since the company had no immediate need for the extra space, the building was rented out to another company for rental revenue of $40,000 per year. The renter’s lease will expire next month, and rather than renewing the lease, Medex Company has decided to use the building itself to manufacture a new product. Direct materials cost for the new product will total $40 per unit. It will be necessary to hire a supervisor to oversee production. Her salary will be $2,500 per month. Workers will be hired to manufacture the new product, with direct labor cost amounting to $18 per unit. Manufacturing operations will occupy all of the building space, so it will be necessary to rent space in a warehouse nearby in order to store finished units of product. The rental cost will be $1,000 per month. In addition, the company will need to rent equipment for use in producing the new product; the rental cost will be $3,000 per month. The company will continue to depreciate the building on a straight-line basis, as in past years. Depreciation on the building is $10,000 per year. Advertising costs for the new product will total $50,000 per year. Costs of shipping the new product to customers will be $10 per unit. Electrical costs of operating machines will be $2 per unit. To have funds to purchase materials, meet payrolls, and so forth, the company will have to liquidate some temporary investments. These investments are presently yielding a return of $6,000 per year. Required: Prepare an answer sheet with the following column headings: Name of the Cost Product Cost Variable Cost Fixed Cost Direct Materials Direct Labor Manufacturing Overhead Period (Selling and Administrative) Cost Opportunity Cost Sunk Cost List the different costs associated with the new product decision down the extreme left column (under Name of the Cost). Then place an X under each heading that helps to describe the type of cost involved. There may be X’s under several column headings for a single cost. (For example, a cost may be a fixed cost, a period cost, and a sunk cost; you would place an X under each of these column headings opposite the cost.) EXERCISE 2–10 High-Low Method; Scattergraph Analysis [LO4] Zerbel Company, a wholesaler of large, custom-built air conditioning units for commercial buildings, has noticed considerable fluctuation in its shipping expense from month to month, as shown below: Month January . . . . . . . . . . February . . . . . . . . . March . . . . . . . . . . . . April . . . . . . . . . . . . May . . . . . . . . . . . . . June . . . . . . . . . . . . . July . . . . . . . . . . . . . . Units Shipped Total Shipping Expense 4 7 5 2 3 6 8 $2,200 $3,100 $2,600 $1,500 $2,200 $3,000 $3,600 Required: 1. gar11005_ch02_024-082.indd 56 Prepare a scattergraph using the data given above. Plot cost on the vertical axis and activity on the horizontal axis. Is there an approximately linear relationship between shipping expense and the number of units shipped? 02/11/10 4:31 PM Confirming Pages Managerial Accounting and Cost Concepts 2. 3. 4. 57 Using the high-low method, estimate the cost formula for shipping expense. Draw a straight line through the high and low data points shown in the scattergraph that you prepared in requirement 1. Make sure your line intersects the Y axis. Comment on the accuracy of your high-low estimates assuming a least-squares regression analysis estimated the total fixed costs to be $1,010.71 per month and the variable cost to be $317.86 per unit. How would the straight line that you drew in requirement 2 differ from a straight line that minimizes the sum of the squared errors? What factors, other than the number of units shipped, are likely to affect the company’s shipping expense? Explain. EXERCISE 2–11 Traditional and Contribution Format Income Statements [LO5] Haaki Shop, Inc., is a large retailer of surfboards. The company assembled the information shown below for the quarter ended May 31: Amount Total sales revenue . . . . . . . . . . . . . . . . . . . . . . . . . . . Selling price per surfboard . . . . . . . . . . . . . . . . . . . . . . . Variable selling expense per surfboard . . . . . . . . . . . . Variable administrative expense per surfboard . . . . . . Total fixed selling expense . . . . . . . . . . . . . . . . . . . . . . Total fixed administrative expense . . . . . . . . . . . . . . . . Merchandise inventory, beginning balance . . . . . . . . . Merchandise inventory, ending balance . . . . . . . . . . . . Merchandise purchases . . . . . . . . . . . . . . . . . . . . . . . . $800,000 $400 $50 $20 $150,000 $120,000 $80,000 $100,000 $320,000 Required: 1. 2. 3. Prepare a traditional income statement for the quarter ended May 31. Prepare a contribution format income statement for the quarter ended May 31. What was the contribution toward fixed expenses and profits for each surfboard sold during the quarter? (State this figure in a single dollar amount per surfboard.) EXERCISE 2–12 Cost Behavior; High-Low Method [LO3, LO4] Speedy Parcel Service operates a fleet of delivery trucks in a large metropolitan area. A careful study by the company’s cost analyst has determined that if a truck is driven 120,000 miles during a year, the average operating cost is 11.6 cents per mile. If a truck is driven only 80,000 miles during a year, the average operating cost increases to 13.6 cents per mile. Required: 1. 2. 3. Using the high-low method, estimate the variable and fixed cost elements of the annual cost of truck operation. Express the variable and fixed costs in the form Y = a + bX. If a truck were driven 100,000 miles during a year, what total cost would you expect to be incurred? EXERCISE 2–13 High-Low Method; Predicting Cost [LO3, LO4] The number of X-rays taken and X-ray costs over the last nine months in Beverly Hospital are given below: Month January . . . . . . . . . . . February . . . . . . . . . . . March . . . . . . . . . . . . . . April . . . . . . . . . . . . . . May . . . . . . . . . . . . . . . June . . . . . . . . . . . . . . July . . . . . . . . . . . . . . . . August . . . . . . . . . . . . September . . . . . . . . . gar11005_ch02_024-082.indd 57 X-Rays Taken X-Ray Costs 6,250 7,000 5,000 4,250 4,500 3,000 3,750 5,500 5,750 $28,000 $29,000 $23,000 $20,000 $22,000 $17,000 $18,000 $24,000 $26,000 02/11/10 4:32 PM Confirming Pages 58 Chapter 2 Required: 1. 2. 3. 4. 5. Using the high-low method, estimate the cost formula for X-ray costs. Using the cost formula you derived above, what X-ray costs would you expect to be incurred during a month in which 4,600 X-rays are taken? Prepare a scattergraph using the data given above. Plot X-ray costs on the vertical axis and the number of X-rays taken on the horizontal axis. Draw a straight line through the two data points that correspond to the high and low levels of activity. Make sure your line intersects the Y-axis. Comment on the accuracy of your high-low estimates assuming a least-squares regression analysis estimated the total fixed costs to be $6,529.41 per month and the variable cost to be $3.29 per X-ray taken. How would the straight line that you drew in requirement 3 differ from a straight line that minimizes the sum of the squared errors? Using the least-squares regression estimates given in requirement 4, what X-ray costs would you expect to be incurred during a month in which 4,600 X-rays are taken? Problems All applicable problems are available with McGraw-Hill’s Connect™ Accounting. PROBLEM 2–14 Contribution Format versus Traditional Income Statement [LO5] House of Organs, Inc., purchases organs from a well-known manufacturer and sells them at the retail level. The organs sell, on the average, for $2,500 each. The average cost of an organ from the manufacturer is $1,500. The costs that the company incurs in a typical month are presented below: Costs Selling: Advertising . . . . . . . . . . . . . . . . . . . . . . . Delivery of organs . . . . . . . . . . . . . . . Sales salaries and commissions . . . . . . Utilities . . . . . . . . . . . . . . . . . . . . . . . . . . Depreciation of sales facilities . . . . . . . . Administrative: Executive salaries . . . . . . . . . . . . . . . Depreciation of office equipment . . . . . . Clerical . . . . . . . . . . . . . . . . . . . . . . . . . . Insurance . . . . . . . . . . . . . . . . . . . . . . . . Cost Formula $950 per month $60 per organ sold $4,800 per month, plus 4% of sales $650 per month $5,000 per month $13,500 per month $900 per month $2,500 per month, plus $40 per organ sold $700 per month During November, the company sold and delivered 60 organs. Required: 1. 2. 3. Prepare a traditional income statement for November. Prepare a contribution format income statement for November. Show costs and revenues on both a total and a per unit basis down through contribution margin. Refer to the income statement you prepared in (2) above. Why might it be misleading to show the fixed costs on a per unit basis? PROBLEM 2–15 Identifying Cost Behavior Patterns [LO3] A number of graphs displaying cost behavior patterns are shown on the next page. The vertical axis on each graph represents total cost and the horizontal axis represents the level of activity (volume). Required: 1. gar11005_ch02_024-082.indd 58 For each of the following situations, identify the graph that illustrates the cost behavior pattern involved. Any graph may be used more than once. a. Electricity bill—a flat fixed charge, plus a variable cost after a certain number of kilowatthours are used. 02/11/10 4:32 PM Rev.Confirming Pages Managerial Accounting and Cost Concepts b. City water bill, which is computed as follows: First 1,000,000 gallons or less . . . . . . Next 10,000 gallons . . . . . . . . . . . . . . Next 10,000 gallons . . . . . . . . . . . . . . Next 10,000 gallons . . . . . . . . . . . . . . Etc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . c. d. e. f. g. h. i. gar11005_ch02_024-082.indd 59 59 $1,000 flat fee $0.003 per gallon used $0.006 per gallon used $0.009 per gallon used Etc. Depreciation of equipment, where the amount is computed by the straight-line method. When the depreciation rate was established, it was anticipated that the obsolescence factor would be greater than the wear and tear factor. Rent on a factory building donated by the city, where the agreement calls for a fixed fee payment unless 200,000 labor-hours or more are worked, in which case no rent need be paid. Cost of raw materials, where the cost starts at $7.50 per unit and then decreases by 5 cents per unit for each of the first 100 units purchased, after which it remains constant at $2.50 per unit. Salaries of maintenance workers, where one maintenance worker is needed for every 1,000 hours of machine-hours or less (that is, 0 to 1,000 hours requires one maintenance worker, 1,001 to 2,000 hours requires two maintenance workers, etc.). Cost of raw material used. Rent on a factory building donated by the county, where the agreement calls for rent of $100,000 less $1 for each direct labor-hour worked in excess of 200,000 hours, but a minimum rental payment of $20,000 must be paid. Use of a machine under a lease, where a minimum charge of $1,000 is paid for up to 400 hours of machine time. After 400 hours of machine time, an additional charge of $2 per hour is paid up to a maximum charge of $2,000 per period. 1 2 3 4 5 6 7 8 9 10 11 12 11/11/10 11:36 AM Confirming Pages 60 Chapter 2 2. How would a knowledge of cost behavior patterns such as those above be of help to a manager in analyzing the cost structure of his or her company? (CPA, adapted) PROBLEM 2–16 Variable and Fixed Costs; Subtleties of Direct and Indirect Costs [LO3, LO6] The Central Area Well-Baby Clinic provides a variety of health services to newborn babies and their parents. The clinic is organized into a number of departments, one of which is the Immunization Center. A number of costs of the clinic and the Immunization Center are listed below. Example: The cost of polio immunization tablets a. The salary of the head nurse in the Immunization Center. b. Costs of incidental supplies consumed in the Immunization Center, such as paper towels. c. The cost of lighting and heating the Immunization Center. d. The cost of disposable syringes used in the Immunization Center. e. The salary of the Central Area Well-Baby Clinic’s information systems manager. f. The costs of mailing letters soliciting donations to the Central Area Well-Baby Clinic. g. The wages of nurses who work in the Immunization Center. h. The cost of medical malpractice insurance for the Central Area Well-Baby Clinic. i. Depreciation on the fixtures and equipment in the Immunization Center. Required: For each cost listed above, indicate whether it is a direct or indirect cost of the Immunization Center, whether it is a direct or indirect cost of immunizing particular patients, and whether it is variable or fixed with respect to the number of immunizations administered. Use the form shown below for your answer. Direct or Indirect Cost of the Immunization Center Item Description Example: The cost of polio immunization tablets . . . . . . . . . . . Direct Direct or Indirect Cost of Particular Patients Indirect Direct X Indirect Variable or Fixed with Respect to the Number of Immunizations Administered Variable X Fixed X PROBLEM 2–17 High-Low Method; Predicting Cost [LO3, LO4] Echeverria SA is an Argentinian manufacturing company whose total factory overhead costs fluctuate somewhat from year to year according to the number of machine-hours worked in its production facility. These costs (in Argentinian pesos) at high and low levels of activity over recent years are given below: Level of Activity Low Machine-hours . . . . . . . . . . . . . . . . Total factory overhead costs . . . . . High 60,000 274,000 pesos 80,000 312,000 pesos The factory overhead costs above consist of indirect materials, rent, and maintenance. The company has analyzed these costs at the 60,000 machine-hours level of activity as follows: Indirect materials (variable) Rent (fixed) . . . . . . . . . . . . Maintenance (mixed) . . . . . Total factory overhead costs gar11005_ch02_024-082.indd 60 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 90,000 pesos 130,000 54,000 274,000 pesos 02/11/10 4:32 PM Confirming Pages Managerial Accounting and Cost Concepts 61 For planning purposes, the company wants to break down the maintenance cost into its variable and fixed cost elements. Required: 1. 2. 3. Estimate how much of the factory overhead cost of 312,000 pesos at the high level of activity consists of maintenance cost. (Hint: To do this, it may be helpful to first determine how much of the 312,000 pesos cost consists of indirect materials and rent. Think about the behavior of variable and fixed costs.) Using the high-low method, estimate a cost formula for maintenance. What total overhead costs would you expect the company to incur at an operating level of 65,000 machine-hours? PROBLEM 2–18 Cost Behavior; High-Low Method; Contribution Format Income Statement [LO3, LO4, LO5] Frankel Ltd., a British merchandising company, is the exclusive distributor of a product that is gaining rapid market acceptance. The company’s revenues and expenses (in British pounds) for the last three months are given below: Frankel Ltd. Comparative Income Statements For the Three Months Ended June 30 April May June Sales in units . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,000 3,750 4,500 Sales revenue . . . . . . . . . . . . . . . . . . . . . . . . . . . . Cost of goods sold . . . . . . . . . . . . . . . . . . . . . . . . Gross margin . . . . . . . . . . . . . . . . . . . . . . . . . . . . Selling and administrative expenses: Shipping expense . . . . . . . . . . . . . . . . . . . . . . . Advertising expense . . . . . . . . . . . . . . . . . . . . . Salaries and commissions . . . . . . . . . . . . . . . . Insurance expense . . . . . . . . . . . . . . . . . . . . . . Depreciation expense . . . . . . . . . . . . . . . . . . . . Total selling and administrative expenses . . . . . . Net operating income (loss) . . . . . . . . . . . . . . . . . £420,000 168,000 252,000 £525,000 210,000 315,000 £630,000 252,000 378,000 44,000 70,000 107,000 9,000 42,000 272,000 £ (20,000) 50,000 70,000 125,000 9,000 42,000 296,000 £ 19,000 56,000 70,000 143,000 9,000 42,000 320,000 £ 58,000 (Note: Frankel Ltd.’s income statement has been recast in the functional format common in the United States. The British currency is the pound, denoted by £.) Required: 1. 2. 3. Identify each of the company’s expenses (including cost of goods sold) as either variable, fixed, or mixed. Using the high-low method, separate each mixed expense into variable and fixed elements. State the cost formula for each mixed expense. Redo the company’s income statement at the 4,500-unit level of activity using the contribution format. PROBLEM 2–19 High-Low and Scattergraph Analysis [LO4] Sebolt Wire Company heats copper ingots to very high temperatures by placing the ingots in a large heat coil. The heated ingots are then run through a shaping machine that shapes the soft ingot into wire. Due to the long heat-up time, the coil is never turned off. When an ingot is placed in the coil, the temperature is raised to an even higher level, and then the coil is allowed to drop to the “waiting” temperature between ingots. Management needs to know the variable cost of power gar11005_ch02_024-082.indd 61 02/11/10 4:32 PM Confirming Pages 62 Chapter 2 involved in heating an ingot and the fixed cost of power during “waiting” periods. The following data on ingots processed and power costs are available: Required: 1. 2. 3. Using the high-low method, estimate a cost formula for power cost. Express the formula in the form Y = a + bX. Prepare a scattergraph by plotting ingots processed and power cost on a graph. Draw a straight line though the two data points that correspond to the high and low levels of activity. Make sure your line intersects the Y-axis. Comment on the accuracy of your high-low estimates assuming a least-squares regression analysis estimated the total fixed costs to be $1,185.45 per month and the variable cost to be $37.82 per ingot. How would the straight line that you drew in requirement 2 differ from a straight line that minimizes the sum of the squared errors? PROBLEM 2–20 Ethics and the Manager [LO2] The top management of General Electronics, Inc., is well known for “managing by the numbers.” With an eye on the company’s desired growth in overall net profit, the company’s CEO (chief executive officer) sets target profits at the beginning of the year for each of the company’s divisions. The CEO has stated her policy as follows: “I won’t interfere with operations in the divisions. I am available for advice, but the division vice presidents are free to do anything they want so long as they hit the target profits for the year.” In November, Stan Richart, the vice president in charge of the Cellular Telephone Technologies Division, saw that making the current year’s target profit for his division was going to be very difficult. Among other actions, he directed that discretionary expenditures be delayed until the beginning of the new year. On December 30, he was angered to discover that a warehouse clerk had ordered $350,000 of cellular telephone parts earlier in December even though the parts weren’t really needed by the assembly department until January or February. Contrary to common accounting practice, the General Electronics, Inc., Accounting Policy Manual states that such parts are to be recorded as an expense when delivered. To avoid recording the expense, Mr. Richart asked that the order be canceled, but the purchasing department reported that the parts had already been delivered and the supplier would not accept returns. Because the bill had not yet been paid, Mr. Richart asked the accounting department to correct the clerk’s mistake by delaying recognition of the delivery until the bill is paid in January. Required: 1. 2. gar11005_ch02_024-082.indd 62 Are Mr. Richart’s actions ethical? Explain why they are or are not ethical. Do the general management philosophy and accounting policies at General Electronics encourage or discourage ethical behavior? Explain. 02/11/10 4:32 PM Confirming Pages Managerial Accounting and Cost Concepts 63 PROBLEM 2–21 High-Low Method; Predicting Cost [LO3, LO4] Golden Company’s total overhead cost at various levels of activity are presented below: Month Machine-Hours Total Overhead Cost 50,000 40,000 60,000 70,000 $194,000 $170,200 $217,800 $241,600 March . . . . . . . . . . . . . . . . . . . . . April . . . . . . . . . . . . . . . . . . . . May . . . . . . . . . . . . . . . . . . . . . June . . . . . . . . . . . . . . . . . . . . . . . . . Assume that the overhead cost above consists of utilities, supervisory salaries, and maintenance. The breakdown of these costs at the 40,000 machine-hour level of activity is as follows: Utilities (variable) . . . . . . . . . . . . . . . . . Supervisory salaries (fixed) . . . . . . . . . Maintenance (mixed) . . . . . . . . . . . . . . Total overhead cost . . . . . . . . . . . . . . . $ 52,000 60,000 58,200 $170,200 The company wants to break down the maintenance cost into its variable and fixed cost elements. Required: 1. 2. 3. 4. Estimate how much of the $241,600 of overhead cost in June was maintenance cost. (Hint: To do this, it may be helpful to first determine how much of the $241,600 consisted of utilities and supervisory salaries. Think about the behavior of variable and fixed costs within the relevant range.) Using the high-low method, estimate a cost formula for maintenance. Express the company’s total overhead cost in the form Y = a + bX. What total overhead cost would you expect to be incurred at an activity level of 45,000 machine-hours? PROBLEM 2–22 Cost Classification [LO2, LO3, LO6] Listed below are costs found in various organizations. 1. Depreciation, executive jet. 2. Costs of shipping finished goods to customers. 3. Wood used in manufacturing furniture. 4. Sales manager’s salary. 5. Electricity used in manufacturing furniture. 6. Secretary to the company president. 7. Aerosol attachment placed on a spray can produced by the company. 8. Billing costs. 9. Packing supplies for shipping products overseas. 10. Sand used in manufacturing concrete. 11. Supervisor’s salary, factory. 12. Executive life insurance. 13. Sales commissions. 14. Fringe benefits, assembly-line workers. 15. Advertising costs. 16. Property taxes on finished goods warehouses. 17. Lubricants for production equipment. gar11005_ch02_024-082.indd 63 02/11/10 4:33 PM Confirming Pages 64 Chapter 2 Required: Prepare an answer sheet with column headings as shown below. For each cost item, indicate whether it would be variable or fixed with respect to the number of units produced and sold; and then whether it would be a selling cost, an administrative cost, or a manufacturing cost. If it is a manufacturing cost, indicate whether it would typically be treated as a direct or indirect cost with respect to units of product. Three sample answers are provided for illustration. Variable or Fixed Cost Item Direct labor . . . . . . . . . . . . . . . . Executive salaries . . . . . . . . . . . Factory rent . . . . . . . . . . . . . . . . . Selling Cost V F F Administrative Cost Manufacturing (Product) Cost Direct Indirect X X X PROBLEM 2–23 High-Low Method; Contribution Format Income Statement [LO4, LO5] Alden Company has decided to use a contribution format income statement for internal planning purposes. The company has analyzed its expenses and has developed the following cost formulas: Cost Cost Formula Cost of goods sold . . . . . . . . . . . . . . . . Advertising expense . . . . . . . . . . . . . . . Sales commissions . . . . . . . . . . . . . . . . Administrative salaries . . . . . . . . . . . . . Shipping expense . . . . . . . . . . . . . . . . . Depreciation expense . . . . . . . . . . . . . . $20 per unit sold $170,000 per quarter 5% of sales $80,000 per quarter ? $50,000 per quarter Management has concluded that shipping expense is a mixed cost, containing both variable and fixed cost elements. Units sold and the related shipping expense over the last eight quarters are given below: Quarter Year 1: First . . . . . . . . . . . . . . . . . Second . . . . . . . . . . . . . Third . . . . . . . . . . . . . . . Fourth . . . . . . . . . . . . . . Year 2: First . . . . . . . . . . . . . . . . . Second . . . . . . . . . . . . . Third . . . . . . . . . . . . . . . Fourth . . . . . . . . . . . . . . Units Sold Shipping Expense 16,000 18,000 23,000 19,000 $160,000 $175,000 $217,000 $180,000 17,000 20,000 25,000 22,000 $170,000 $185,000 $232,000 $208,000 Management would like a cost formula derived for shipping expense so that a budgeted contribution format income statement can be prepared for the next quarter. Required: 1. 2. Using the high-low method, estimate a cost formula for shipping expense. In the first quarter of Year 3, the company plans to sell 21,000 units at a selling price of $50 per unit. Prepare a contribution format income statement for the quarter. PROBLEM 2–24 Cost Classification and Cost Behavior [LO2, LO3, LO6] Heritage Company manufactures a beautiful bookcase that enjoys widespread popularity. The company has a backlog of orders that is large enough to keep production going indefinitely at the plant’s full capacity of 4,000 bookcases per year. Annual cost data at full capacity follow: gar11005_ch02_024-082.indd 64 02/11/10 4:33 PM Confirming Pages Managerial Accounting and Cost Concepts Direct materials used (wood and glass) . . . . . . . . . . . Administrative office salaries . . . . . . . . . . . . . . . . . . . Factory supervision . . . . . . . . . . . . . . . . . . . . . . . . . . Sales commissions . . . . . . . . . . . . . . . . . . . . . . . . . . Depreciation, factory building . . . . . . . . . . . . . . . . . . . Depreciation, administrative office equipment . . . . . . Indirect materials, factory . . . . . . . . . . . . . . . . . . . . . . Factory labor (cutting and assembly) . . . . . . . . . . . . . Advertising . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Insurance, factory . . . . . . . . . . . . . . . . . . . . . . . . . . . . Administrative office supplies (billing) . . . . . . . . . . . . Property taxes, factory . . . . . . . . . . . . . . . . . . . . . . . . Utilities, factory . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65 $430,000 $110,000 $70,000 $60,000 $105,000 $2,000 $18,000 $90,000 $100,000 $6,000 $4,000 $20,000 $45,000 Required: 1. Prepare an answer sheet with the column headings shown below. Enter each cost item on your answer sheet, placing the dollar amount under the appropriate headings. As examples, this has been done already for the first two items in the list above. Note that each cost item is classified in two ways: first, as either variable or fixed with respect to the number of units produced and sold; and second, as either a selling and administrative cost or a product cost. (If the item is a product cost, it should also be classified as either direct or indirect as shown.) Cost Behavior Cost Item Materials used . . . . . . . . . Administrative office salaries . . . . . . . . . . . . . Variable Fixed Selling or Administrative Cost $430,000 Product Cost Direct Indirect* $430,000 $110,000 $110,000 *To units of product. 2. 3. 4. Total the dollar amounts in each of the columns in (1) above. Compute the average product cost per bookcase. Due to a recession, assume that production drops to only 2,000 bookcases per year. Would you expect the average product cost per bookcase to increase, decrease, or remain unchanged? Explain. No computations are necessary. Refer to the original data. The president’s next-door neighbor has considered making himself a bookcase and has priced the necessary materials at a building supply store. He has asked the president whether he could purchase a bookcase from the Heritage Company “at cost,” and the president has agreed to let him do so. a. Would you expect any disagreement between the two men over the price the neighbor should pay? Explain. What price does the president probably have in mind? The neighbor? b. Because the company is operating at full capacity, what cost term used in the chapter might be justification for the president to charge the full, regular price to the neighbor and still be selling “at cost”? Explain. Cases All applicable cases are available with McGraw-Hill’s Connect™ Accounting. CASE 2–25 Scattergraph Analysis; Selection of an Activity Base [LO4] Mapleleaf Sweepers of Toronto manufactures replacement rotary sweeper brooms for the large sweeper trucks that clear leaves and snow from city streets. The business is seasonal, with the largest demand during and just preceding the fall and winter months. Because there are so many different kinds of sweeper brooms used by its customers, Mapleleaf Sweepers makes all of its brooms to order. gar11005_ch02_024-082.indd 65 02/11/10 4:33 PM Confirming Pages 66 Chapter 2 The company has been analyzing its overhead accounts to determine fixed and variable components for planning purposes. Below are data for the company’s janitorial labor costs over the last nine months. (Cost data are in Canadian dollars.) January . . . . . . . . . . . . . February . . . . . . . . . . . . March . . . . . . . . . . . . . . . April . . . . . . . . . . . . . . . . May . . . . . . . . . . . . . . . . June . . . . . . . . . . . . . . . July . . . . . . . . . . . . . . . . . August . . . . . . . . . . . . . . September . . . . . . . . . . . Number of Units Produced Number of Janitorial Workdays Janitorial Labor Cost 115 109 102 76 69 108 77 71 127 21 19 23 20 23 22 16 14 21 $3,840 $3,648 $4,128 $3,456 $4,320 $4,032 $2,784 $2,688 $3,840 The number of workdays varies from month to month due to the number of weekdays, holidays, days of vacation, and sick leave taken in the month. The number of units produced in a month varies depending on demand and the number of workdays in the month. There are two janitors who each work an eight-hour shift each workday. They each can take up to 10 days of paid sick leave each year. Their wages on days they call in sick and their wages during paid vacations are charged to miscellaneous overhead rather than to the janitorial labor cost account. Required: 1. 2. 3. Plot the janitorial labor cost and units produced on a scattergraph. (Place cost on the vertical axis and units produced on the horizontal axis.) Plot the janitorial labor cost and number of workdays on a scattergraph. (Place cost on the vertical axis and the number of workdays on the horizontal axis.) Which measure of activity—number of units produced or janitorial workdays—should be used as the activity base for explaining janitorial labor cost? CASE 2–26 Mixed Cost Analysis and the Relevant Range [LO3, LO4] The Ramon Company is a manufacturer that is interested in developing a cost formula to estimate the fixed and variable components of its monthly manufacturing overhead costs. The company wishes to use machine-hours as its measure of activity and has gathered the data below for this year and last year: Last Year Month January . . . . . . . . . . . . . . . . . . February . . . . . . . . . . . . . . . . . March . . . . . . . . . . . . . . . . . . . April . . . . . . . . . . . . . . . . . . . . May . . . . . . . . . . . . . . . . . . . . . June . . . . . . . . . . . . . . . . . . . . July . . . . . . . . . . . . . . . . . . . . . . August . . . . . . . . . . . . . . . . . . September . . . . . . . . . . . . . . . October . . . . . . . . . . . . . . . . . . November . . . . . . . . . . . . . . . . December . . . . . . . . . . . . . . . . This Year MachineHours Overhead Costs MachineHours Overhead Costs 21,000 25,000 22,000 23,000 20,500 19,000 14,000 10,000 12,000 17,000 16,000 19,000 $84,000 $99,000 $89,500 $90,000 $81,500 $75,500 $70,500 $64,500 $69,000 $75,000 $71,500 $78,000 21,000 24,000 23,000 22,000 20,000 18,000 12,000 13,000 15,000 17,000 15,000 18,000 $86,000 $93,000 $93,000 $87,000 $80,000 $76,500 $67,500 $71,000 $73,500 $72,500 $71,000 $75,000 The company leases all of its manufacturing equipment. The lease arrangement calls for a flat monthly fee up to 19,500 machine-hours. If the machine-hours used exceeds 19,500, then the fee gar11005_ch02_024-082.indd 66 02/11/10 4:33 PM Rev.Confirming Pages Managerial Accounting and Cost Concepts 67 becomes strictly variable with respect to the total number of machine-hours consumed during the month. Lease expense is a major element of overhead cost. Required: 1. 2. 3. 4. 5. Using the high-low method, estimate a manufacturing overhead cost formula. Prepare a scattergraph using all of the data for the two-year period. Fit a straight line or lines to the plotted points using a ruler. Describe the cost behavior pattern revealed by your scattergraph plot. Assume a least-squares regression analysis using all of the given data points estimated the total fixed costs to be $40,102 and the variable costs to be $2.13 per machine-hour. Do you have any concerns about the accuracy of the high-low estimates that you have computed or the least-squares regression estimates that have been provided? Assume that the company consumes 22,500 machine-hours during a month. Using the highlow method, estimate the total overhead cost that would be incurred at this level of activity. Be sure to consider only the data points contained in the relevant range of activity when performing your computations. Comment on the accuracy of your high-low estimates assuming a least-squares regression analysis using only the data points in the relevant range of activity estimated the total fixed costs to be $10,090 and the variable costs to be $3.53 per machine-hour. Appendix 2A: Least-Squares Regression Computations The least-squares regression method for estimating a linear relationship is based on the equation for a straight line: Y = a + bX As explained in the chapter, least-squares regression selects the values for the intercept a and the slope b that minimize the sum of the squared errors. The following formulas, which are derived in statistics and calculus texts, accomplish that objective: LEARNING OBJECTIVE 8 Analyze a mixed cost using a scattergraph plot and the leastsquares regression method. (ΣX)(ΣY) b = n(ΣXY) − ______________ n(ΣX2) − (ΣX)2 (ΣY) − b(ΣX) a = ____________ n where: X = The level of activity (independent variable) Y = The total mixed cost (dependent variable) a = The total fixed cost (the vertical intercept of the line) b = The variable cost per unit of activity (the slope of the line) n = Number of observations ∑ = Sum across all n observations Manually performing the calculations required by the formulas is tedious at best. Fortunately, statistical software packages are widely available that perform the calculations automatically. Spreadsheet software, such as Microsoft® Excel, can also be used to do least-squares regression—although it requires a little more work than using a specialized statistical application. In addition to estimates of the intercept (fixed cost) and slope (variable cost per unit), Excel also provides a statistic called the R2, which is a measure of “goodness of fit.” The R2 tells us the percentage of the variation in the dependent variable (cost) that is explained by variation in the independent variable (activity). The R2 varies from 0% to 100%, and the higher the percentage, the better. You should always plot the data in a scattergraph, gar11005_ch02_024-082.indd 67 11/11/10 11:37 AM