Cash & Cash Equivalents Test: Accounting Practice

advertisement

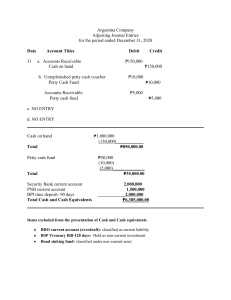

lOMoARcPSD|12528915 CASH AND CASH EQUIVALENTS- Datumanguda, Ugokan Theories 1. A cash equivalent is a short-term, highly liquid investment that is readily convertible into known amount of cash and a. Is acceptable as a meant to pay current liabilities. b. Has a current market value that is greater than its original cost. c. Bears an interest rate that is at least equal to the prime rate of interest at the date of liquidation. d. Is so near its maturity that it presents insignificant risk of change in interest rate. 2. Which of the following should not be included in “cash”? a. Coins and currency b. Checks from other parties presently in the cash register c. Amounts on deposit in checking account at the bank d. Postage stamps on hand 3. Which item should be excluded from cash and cash equivalents? a. The minimum cash balance in the entity’s current account which is maintained to avoid service charges. b. A check issued by the entity on December 27 of the current year but dated January 15 of next year. c. Time deposit which matures in one year. d. A customer’s check denominated in a foreign currency. 4. In which account are customers’ postdated checks received classified? a. Accounts receivable b. Prepaid expenses c. Cash d. Accounts payable 5. Deposits held as compensating balance a. Usually do not earn interest. b. If legally restricted and held against short-term credit may be included as cash. c. If legally restricted and held against long-term credit may be included among current assets. d. None of the above. 6. In reimbursing the petty cash fund, which of the following statements is true? a. Cash is debited b. Petty cash is debited c. Petty cash is credited d. Expense accounts are debited Downloaded by ELLIE LIM (lawrelynjoydlimpiada@tua.edu.ph) lOMoARcPSD|12528915 7. The internal control feature that is specific to petty cash is a. Separation of duties b. Assignment of responsibility c. Proper authorization d. Imprest system 8. What is the major purpose of an imprest petty cash fund? a. To effectively plan cash inflows and outflows b. To ease the payment of cash to vendors c. To determine the honesty of the petty cashier d. To effectively control cash disbursements 9. Which is not considered as a cash equivalent? a. A three-year treasury note maturing on May 30 of the current year purchased by the entity on April 15 of the current year b. A three-year treasury note maturing on May 30 of the current year purchased by the entity on January 15 of the current year c. A 90-day treasury bill d. A 60-day money market placement 10. If material, deposits in foreign bank which are subject to foreign exchange restriction shall be classified a. Separately as current asset, with appropriate disclosure. b. Separately as noncurrent asset with appropriate disclosure. c. Be written off as an extraordinary loss. d. As part of cash and cash equivalents. 11. Cash set aside for a particular purpose is a. Immediately classified as noncurrent asset b. May be classified as current or noncurrent asset depending on the purpose for its establishment c. Still classified as current asset regardless of the purpose of the establishment d. Recorded in off-balance sheet records 12. Deposits in foreign bank which are subject to foreign exchange restriction should be classified a. Separately as current asset with appropriate disclosure. b. Separately as noncurrent asset with appropriate disclosure. c. Be written off as loss. d. As part of cash and cash equivalents. Downloaded by ELLIE LIM (lawrelynjoydlimpiada@tua.edu.ph) lOMoARcPSD|12528915 13. Which of the following should be considered “cash”? a. Certified check b. Postdated check c. Undelivered check d. Stale check 14. In which account are postage stamps classified? a. Receivables b. Prepaid expenses c. Cash d. Payables 15. How is interest earned on cash equivalents shown in statement of cash flows? a. As an operating activity b. As an investing activity c. As a financing activity d. As a noncash investing and financing activity 16. Which of the following statements in relation to an imprest petty cash is incorrect? a. The imprest petty cash system in effect adheres to the rule of disbursement by check. b. Entries are made to the petty cash account only to increase or decrease the size of the fund or to adjust the balance if not replenished at year-end. c. The petty cash account is debited when the fund is replenished. d. The petty cash und is reported as part of current assets. 17. When an imprest petty cash fund is used, which of the following statements is true? a. The balance of the petty cash fund should be reported in the statement of financial position as a long-term investment. b. The petty cashier’s summary of petty cash payments serves as a journal entry that is posted to the appropriate general ledger account. c. The reimbursement of the petty cash fund should be credited to the cash account. d. Entries that include a credit to the cash account should be recorded at the time the payments from the petty cash fund are made. 18. Which of the following statements in relation to petty cash fund is false? a. Each disbursement form petty cash should be supported by a petty cash voucher. b. The creation of a petty cash fund requires a journal entry to reflect the transfer of fund out of the general cash account. c. At any time, the sum of the cash in the petty cash fund and the total of petty cash vouchers should equal the amount for which the imprest petty cash fund was established. d. With the establishment of an imprest petty cash fund, one person is given the authority and responsibility for issuing checks to cover minor disbursements. Downloaded by ELLIE LIM (lawrelynjoydlimpiada@tua.edu.ph) lOMoARcPSD|12528915 19. It is a practice of opening the books of accounts beyond the close of the reporting period for the purpose of showing a better financial position and performance. a. Window dressing b. Kiting c. Lapping d. None of the above 20. It consists of misappropriating a collection from one customer and concealing this defalcation by applying a subsequent collection made from another customer. a. Window dressing b. Kiting c. Lapping d. None of the above 21. What is the entry to record increase in fund under imprest fund system? a. Petty cash fund xx Cash in bank xx b. Cash in bank xx Petty cash fund xx c. Cash on hand xx Accounts receivable xx d. Petty cash fund xx Accounts receivable xx 22. Which of the following statements is incorrect concerning measurement of cash and cash equivalents? a. Cash is measured at face value b. Cash in foreign currency is measured at the current exchange rate c. If a bank or financial institution holding the funds of the entity is in bankruptcy or financial difficulty, cash shall be written down to estimated realizable value d. Cash equivalents shall be measured at maturity value, meaning face value plus interest 23. Bank overdraft generally should be a. Reported as a deduction from current assets. b. Reported as a deduction from cash. c. Netted against cash and a net cash amount reported. d. Reported as a current liability. 24. Which of the following is classified as “cash and cash equivalents”? Downloaded by ELLIE LIM (lawrelynjoydlimpiada@tua.edu.ph) lOMoARcPSD|12528915 a. b. c. d. Sinking fund Preference share redemption fund Travel fund Insurance fund 25. A cash over and short account a. Is credited when the petty cash fund proves out over. b. Is credited when the petty cash fund proves out short. c. Is debited when the petty cash fund proves out over. d. Is a contra account to cash. Downloaded by ELLIE LIM (lawrelynjoydlimpiada@tua.edu.ph) lOMoARcPSD|12528915 Problem Solving 1. On December 31, 2017, Pot Company had the following balances in the bank: Checking account #101 Time Deposit- 30 days 150-day treasury bill, acquired on Oct. 1, 2017, due on Feb. 1, 2018 180-day treasury bill, due April 2, 2018 90-day treasury bill, due Feb. 28, 2018 2,000,000 300,000 575,000 400,000 150,000 What amount should Pot Company report as cash and cash equivalents? a. 3,425,000 b. 2,450,000 c. 3,025,000 d. 2,850,000 Checking account #101 Time Deposit- 30 days 90-day treasury bill, due Feb. 28, 2018 Cash and Cash Equivalents 2,000,000 300,000 _____150,000 P2,450,000 2. Wing Company had the following balances on December 31, 2015: Cash in bank- current account Cash on hand Cash in bank- restricted account for building construction expected to be disbursed in 2016 Time deposit, purchased Nov. 5, 2015, and due Feb. 1, 2016 4,500,000 2,150,000 5,000,000 300,000 The cash on hand included a P150,000 check payable to Wing, dated Jan. 7, 2016. What total amount should be reported as cash and cash equivalents on December 31, 2015? a. 6,650,000 b. 6,950,000 c. 6,800,000 d. 7,300,000 Cash in bank- current account Cash on hand Time deposit Cash and Cash Equivalents 4,500,000 2,000,000 ___300,000 P6,800,000 Downloaded by ELLIE LIM (lawrelynjoydlimpiada@tua.edu.ph) lOMoARcPSD|12528915 3. At year-end, Krisha Company reported cash and cash equivalents which comprised the following: Cash on hand Demand deposit Postdated customer check Traveler’s check Manager’s check Money order Petty cash fund 30,000 15,000 7,500 11,250 15,600 12,000 3,500 What total amount should be reported as “cash” at year-end? a. 79,250 b. 60,350 c. 87,350 d. 64,500 Cash on hand Demand deposit Traveler’s check Manager’s check Money order Petty cash fund Cash 30,000 15,000 11,250 15,600 12,000 ____3,500 P87,350 Downloaded by ELLIE LIM (lawrelynjoydlimpiada@tua.edu.ph) lOMoARcPSD|12528915 4. On December 31, 2014, Mitch Company reported cash 2,950,000 with the following details: Undeposited collection Cash in bank- Metrobank checking account Undeposited check from a customer, dated January 7, 2015 Cash in bank- Metrobank fund for payroll Cash in bank- Metrobank money market instrument, 90 days Cash in foreign bank restricted Total 300,000 450,000 100,000 525,000 875,000 __700,000 2,950,000 On December 31, 2014, what is the correct amount of cash and cash equivalents? a. 2,150,000 b. 2,950,000 c. 2,075,000 d. 2,850,000 Undeposited collection Cash in bank- Metrobank checking account Cash in bank- Metrobank fund for payroll Cash in bank- Metrobank money market instrument, 90 days Cash and Cash Equivalents 300,000 450,000 525,000 ____875,000 P2,150,000 Downloaded by ELLIE LIM (lawrelynjoydlimpiada@tua.edu.ph) lOMoARcPSD|12528915 5. Paidu Company provided the following information on December 31, 2018: Cash on hand Security Bank current account BDO current account no. 1 BDO current account no. 2 (overdraft) BSP treasury bill-60 days 500,000 890,000 670,000 (75,000) 150,000 The cash on hand included a customer postdated check of P95,000 and postal money order of P120,000. A check for P150,000 in payment of account was drawn against Security Bank current account, dated January 20, 2019 but recorded December 31, 2018. What total amount of cash and cash equivalents should be reported on December 31, 2018? a. 2,285,000 b. 1,895,000 c. 1,920,000 d. 2,190,000 Cash on hand (500,000-95,000) Security Bank current account (890,000 + 150,000) BDO current account no. 1 BDO current account no. 2 BSP treasury bill-60 days Cash and cash equivalents 405,000 1,040,000 670,000 (75,000) ____150,000 P2,190,000 6. Far Company had cash in bank of P300,000, petty cash fund of P15,000, cash restricted for plant expansion fund of P2,500,000, and a bank overdraft in a second account at another bank of P50,000. What total amount of cash should be reported? a. 265,000 b. 315,000 c. 2,815,000 d. 2, 765,000 Cash in bank Petty cash fund Cash 300,000 __15,000 P315,000 Downloaded by ELLIE LIM (lawrelynjoydlimpiada@tua.edu.ph) lOMoARcPSD|12528915 7. Mhezzy Company provided the following data at year-end: Cash balance in checking account with First Bank Overdraft in checking account with Second Bank Currency and coins in petty cash fund Cash in a special fund for plant expansion 700,000 (230,000) 5,080 2,500,000 What total amount should be reported as cash at year-end? a. 475,080 b. 700,000 c. 705,080 d. 2,975,080 Cash balance in checking account with First Bank Currency and coins in petty cash fund Cash 700,000 ____5,080 P705,080 8. Shai Company reported a total cash and cash equivalent of P6,325,000 on December 31, 2014, which includes the following information: Two certificates of deposits, each totaling P500,000. These certificates of deposit have maturity of 120 days. A check that is dated January 12, 2015 in the amount of P125,000. A commercial paper of P2,100,000 which is due in 120 days. Currency and coins on hand amounted to P7,700. Shai Company has agreed to maintain a cash balance of P500,000 in one of its bank at all times and it is not available for withdrawal and to ensure future credit availability (this amount was included in the above balance). How much is the correct amount of cash and cash equivalents that Shai Company should report in its December 31, 2014 statement of financial position? a. b. c. d. 2,600,000 3,100,000 5,200,000 6,200,000 Balance reported Certificate of deposit Postdated check Compensating balance Commercial paper Correct cash and cash equivalents 6,325,000 (1,000,000) (125,000) (500,000) (2,100,000) P2,600,000 Downloaded by ELLIE LIM (lawrelynjoydlimpiada@tua.edu.ph) lOMoARcPSD|12528915 9. Jayrs Corporation’s checkbook balance on December 31, 2016 was P160,000. On the same date, Jayrs held the following items in its safe: A P5,000 check payable to Jayrs, dated January 2, 2015, was not include in the December 31 checkbook balance. A P3,500 check payable to Jayrs which was deposited December 19 and included in the December 31 checkbook balance, was returned by the bank on December 30 marked NSF. The check was redeposited on January 2, 2017 and cleared on January 9. A P25,000 check payable to supplier and drawn on Jayrs’ account, was dated and recorded on December 31, but was not mailed until January 19, 2017. In its December 31, 2016 statement of financial position, how much should Jayrs report as cash? a. b. c. d. 156,600 161,500 181,500 185,000 Balance per checkbook Undelivered check NSF check Correct cash balance 160,000 25,000 ___(3,500) P181,500 10. Following were the account balances of Ana Company at December 31, 2019: Cash on hand Cash in current and savings accounts Cash set aside for plant expansion (expected for payment in 2020) 187,500 3,375,000 2,400,000 Cash in current and savings accounts includes P50,000 as holdout against short-term loan arrangements. There are no legal restrictions as to withdrawal by Ana on these holdouts. What is the total cash that should be reported in the current asset section of Ana‘s December 31, 2019 statement of financial position? a. 2,662,500 b. 3,375,000 c. 3,562,000 d. 5,962,000 Cash on hand Cash in current and savings accounts Total cash 187,500 ___3,375,000 P3,562,000 Downloaded by ELLIE LIM (lawrelynjoydlimpiada@tua.edu.ph) lOMoARcPSD|12528915 11. On October 1, Mariam Corporation established an imprest petty cash fund for P15,000 by writing a check drawn against its general checking account. On Oct. 1, the fund contained the following: Currency and coins Transportation Telephone Postage 3,000 4,700 4,400 2,900 On October 1, the entity wrote a check to replenish the fund. What is the amount of replenishment under imprest fund system? a. 15,000 b. 13,000 c. 12,000 d. 11,000 Transportation Telephone Postage Total replenishment 4,700 4,400 ____2,900 P12,000 12. Dawdaw Company had the following balances on December 31, 2010: Cash in checking account Cash in money market account Treasury bill, purchased Nov. 1, 2010 maturing Jan. 31, 2011 Time deposit purchased Dec. 1, 2010 maturing Feb. 28, 2011 400,000 350,000 2,750,000 1,100,000 What amount should be reported as cash and cash equivalents on Dec. 31, 2010? a. 750,000 b. 3,500,000 c. 3,850,000 d. 4,600,000 Cash in checking account Cash in money market account Treasury bill, purchased Nov. 1, 2010 maturing Jan. 31, 2011 Time deposit purchased Dec. 1, 2010 maturing Feb. 28, 2011 Cash and cash equivalents 400,000 350,000 2,750,000 ____1,100,000 P4,600,000 Downloaded by ELLIE LIM (lawrelynjoydlimpiada@tua.edu.ph) lOMoARcPSD|12528915 13. The controller of the Shrek Corporation is trying to determine the amount of cash and cash equivalents to be reported on its December 31, 2017, statement of financial position. The following information is provided: Balances in the company’s account at the Monte Bank: Checking account- P540,000 Savings account- P884,000 Undeposited customer checks of P208,000 Savings account at the BPI with a balance of P350,000. This account is being used to accumulate cash for future plant expansion (in 2019). P800,000 balance in a checking account at the BPI. Treasury bills; 30-day maturity bills totaling P600,000, and 180-day bills totaling P800,000. What total amount of cash and cash equivalent should be reported in the current asset section of the 2017 statement of financial position? a. b. c. d. 3,032,000 2,432,000 2,932,000 2,332,000 Checking account in Monte Bank Savings account in Monte Bank Undeposited customer check Check account in BPI Treasury bills with 30-day maturity Cash and cash equivalents 540,000 884,000 208,000 800,000 _____600,000 P3,032,000 Downloaded by ELLIE LIM (lawrelynjoydlimpiada@tua.edu.ph) lOMoARcPSD|12528915 14. The auditor for Pasaol Corporation examined the petty cash fund immediately after the close of business July 31, 2016, the end of the company’s natural business year. The petty cash custodian presented the following during the count: Currency Petty cash vouchers A check drawn by Pasaol payable to the petty cash custodian Psotage stamps An employee’s check, returned by bank, marked NSF An envelope containing currency for a gift for a retiring employee 1,650 3,960 7,200 300 1,000 1,890 The general ledger shows an imprest petty cash fund balance of P16,000. How much is the petty cash shortage or overage? a. 2,190 overage b. 2,190 shortage c. 1,890 shortage d. 1,890 overage Currency Petty cash vouchers Replenishment check Employee’s NSF check Petty cash accounted Petty cash fund per ledger Petty cash shortage 1,650 3,960 7,200 _1,000 13,810 (16,000) (P2,190) 15. Based on the information given in #14, what is the adjusted balance of the petty cash fund at July 31, 2016? a. 10,740 b. 3,540 c. 7,200 d. 8,850 Currency Replenishment check Adjusted petty cash balance 1,650 __7,200 P8,850 Downloaded by ELLIE LIM (lawrelynjoydlimpiada@tua.edu.ph) lOMoARcPSD|12528915 16. Ali Company’s checkbook balance at December 31, 2012 was P180,000. In addition, Ali held the following items in its safe on that date: Check payable to Ali dated January 2, 2013 in payment of a sale made in December 2012, included in December 31 checkbook balance, P65,000. Check payable to Ali deposited December 15 but returned by the bank marked NSF, P20,000. Check drawn on Ali’s account, payable to a vendor, dated and recorded on December 30 but not yet mailed to payee as of December 31, 2012, P15,000. What is the correct balance of the company? a. b. c. d. 180,000 110,000 115,000 95,000 Checkbook balance Postdated check NSF check Undelivered check Correct cash balance 180,000 (65,000) (20,000) ___15,000 P110,000 Downloaded by ELLIE LIM (lawrelynjoydlimpiada@tua.edu.ph) lOMoARcPSD|12528915 17. A school supplies enterprise, operating on a calendar-year basis, has the following data in its accounting records: Cash Accounts receivable Inventory Accounts payable Sales Cost of goods sold Operating expenses January 1 93,000 105,000 169,000 77,000 December 31 ? 138,000 191,000 87,600 890,000 530,000 203,000 What is the expected cash balance for December 31? a. 271,600 b. 184,400 c. 205,600 d. 294,400 Sales Cost of goods sold Operating expenses Net Income Increase in Accounts Receivable Increase in Inventory Increase in Accounts Payable Increase in Cash Cash, January 1 Cash, December 31 890,000 (530,000) (203,000) 157,000 (33,000) (22,000) ___10,600 112,600 __93,000 P205,600 18. Mama Corporation had the following account balances on Dec. 31, 2013: Cash on hand and in bank Cash restricted for bonds payable due on June 30, 2014 Savings deposit set aside for dividends payable on June 30, 2014 3,450,000 5,230,000 4,910,000 What is the total amount that should be reported as cash and cash equivalents? a. 3,450,000 b. 8,360,000 c. 8,680,000 d. 13,590,000 Cash on hand and in bank Cash restricted for bonds payable Savings deposit 3,450,000 5,230,000 __4,910,000 Downloaded by ELLIE LIM (lawrelynjoydlimpiada@tua.edu.ph) lOMoARcPSD|12528915 Cash and cash equivalents P13,590,000 19. Antok Company had the following account balances on December 31, 2015: Cash in bank Cash on hand Petty cash fund Cash restricted for additional plant in 2016 670,000 310,500 35,000 1,400,000 Cash in bank included P200,000 of compensating balance against short-term borrowing arrangement. The compensating balance is not legally restricted as to withdrawal. What amount should be reported as “cash” on December 31, 2015? a. 815,500 b. 1,015,500 c. 2,215,500 d. 2,415,500 Cash in bank Cash on hand Petty cash fund Cash 670,000 310,500 ______35,000 P1,015,500 20. Puyat Company reported the following information at year-end: Share investment of P1,000,000 that are very actively traded in the stock market. Government treasury bills of P3,000,000 with a 10-year term but purchased on December 31 at which time they had two months to go until maturity. Cash of P2,100,000 in the form of coin, currency, saving account and checking account. Commercial papers of P1,600,000 with term of nine months but purchased on December 31 at which time they had three months to go until maturity. What is the total amount of cash and cash equivalents? a. b. c. d. 6,700,000 5,100,000 4,600,000 3,200,000 Cash Government treasury bills Commercial papers Cash and cash equivalents 2,100,000 3,000,000 __1,600,000 P6,700,000 Downloaded by ELLIE LIM (lawrelynjoydlimpiada@tua.edu.ph) lOMoARcPSD|12528915 21. The cash account of Kapoy Company’s ledger on Dec. 31, 2011 showed a balance of P4,610,500 which included the following: Petty cash fund Undeposited receipts, including a postdated customer check of P350,000 Cash in bank Cash in sinking fund IOUs signed by employees Total 43,500 607,000 450,000 2,600,000 __400,000 4,610,500 At what amount should Kapoy report as cash in the Dec. 31, 2011 statement of financial position? a. 750,500 b. 1,100,500 c. 3,350,500 d. 3,700,500 Petty cash fund Undeposited receipts Cash in bank Cash 43,500 257,000 __450,000 P750,000 22. On December 31, 2019, Pagod Company had the following cash balances: Cash in bank-current account Petty cash fund (all funds were reimbursed at year-end) Time deposit-three months, due January 16, 2020 Savings deposit 4,000,000 175,000 1,300,000 800,000 Cash in bank included P500,000 of compensating balance against short-term borrowing arrangement. The compensating balance is legally restricted as to withdrawal. What total amount should be reported as cash and cash equivalents? a. 6,275,000 b. 5,775,000 c. 4,975,000 d. 4,475,000 Cash in bank Petty cash fund Time deposit Savings deposit Cash and cash equivalents 3,500,000 175,000 1,300,000 ____800,000 P5,775,000 Downloaded by ELLIE LIM (lawrelynjoydlimpiada@tua.edu.ph) lOMoARcPSD|12528915 23. Okay Company provided the following information with respect to its cash and cash equivalents on December 31, 2018: Checking account at BPI Checking account at Metrobank Treasury bonds Payroll account Value added tax account Foreign bank account- restricted Postage stamps Employee’s postdated check IOU from president’s brother Credit memo from a vendor for a purchase return Traveler’s check NSF check Petty cash fund (P10,000 in currency and expense receipts for P35,000) Money order (100,000) 475,000 1,500,000 350,000 200,000 2,500,000 10,000 230,000 310,000 150,000 380,000 420,000 45,000 180,000 What total amount should be reported as unrestricted cash and cash equivalent on December 31, 2018? a. 1,630,000 b. 1,445,000 c. 1,495,000 d. 1,595,000 Checking account at Metrobank Payroll account Value added tax account Traveler’s check Petty cash fund Money order Unrestricted cash and cash equivalent 475,000 350,000 200,000 380,000 10,000 ____180,000 P1,595,000 Downloaded by ELLIE LIM (lawrelynjoydlimpiada@tua.edu.ph) lOMoARcPSD|12528915 24. Kengkoy Company had cash in bank of P2,000,000, petty cash fund of P37,500, cash sinking fund of P2,100,000, and money order of P310,000. How much should be reported as cash? a. 2,037,500 b. 2,310,000 c. 2,347,500 d. 4,447,500 Cash in bank Petty cash fund Money order Cash 2,000,000 37,500 ___310,000 P2,347,500 25. Tapos Company had cash on hand of P230,000 which included the following: A customer check for P43,000 returned by the bank on Dec. 28, 2016. It was redeposited and cleared the bank on January 2, 2017. A customer check for P75,000 dated January 3, 2017, received December 27, 2016. Postal money orders received from customers, P30,000. How much is the correct amount of cash on hand? a. b. c. d. 112,000 155,000 187,000 200,000 Cash on hand NSF check Postdated check Adjusted cash on hand 230,000 (43,000) __(75,000) P112,000 Downloaded by ELLIE LIM (lawrelynjoydlimpiada@tua.edu.ph)