Tianxiang Electronic Instrument Company Performance Evaluation

advertisement

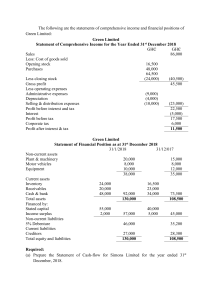

财务绩效评价与控制 Performance Evaluation of Tianxiang Electronic Instrument Company Tianxiang Electronic Instrument Company is a large company that produces professional instruments (voltmeters, etc.) for measuring current characteristics. Its products are divided into two major production lines: electrical instruments (EM) and electronic instruments (EI). These two types of products are substitute products and are industrial measuring instruments, but they are in different technical stages. EM's technology is relatively old, but it is still the mainstream of the industry, and EI's technology is new and experimental. Zhang Tian is the general manager of Tianxiang Company. One day at the beginning of 2019, he looked at the company's income statement for 2018 (Table A). It seemed that the overall performance in 2018 was good and satisfactory. The next question to consider is whether or not we should issue substantial bonuses to middle and senior managers in recognition of their efforts to exceed profits. Tianxiang Company has two business departments: Marketing Department and Production Department, which are respectively responsible for product sales strategy and product production. At the same time, there are two vice presidents who are responsible for coordinating the relevant decisions of the two types of products to ensure the maximum profit of each product. Zhang Tian also hopes to summarize the reasons for outstanding performance in 2018 and provide experience for the company's future strategic development. Thinking: If you are Zhang Tian, how do you use the difference analysis to evaluate the performance of the marketing and production managers and the two product vice presidents in charge of EI/EM in 2018? What do you think is the reason for the outstanding performance of Tianxiang in 2018? Any suggestions for the business strategy for the coming year? Sales gross profit Other costs Selling expenses General & Admin expenses R&D expenses Profit before tax 1 / 2 Table A Initial operating results of Tianxiang 2018 年 (thousand) budget Percentage of sales Actual Percentage of sales 6,215 100% 6,319 100% 2,590 42% 2,660 42% 706 11% 740 12% 320 5% 325 5% 318 5% 325 5% 1,246 20% 1,270 20% 财务绩效评价与控制 Table B product information Price per unit Standard price (competition) Tianxiang company actual price Production cost per unit Average standard variable manufacturing cost Average actual variable manufacturing cost Average standard sales commission Average actual sales commission Number of products sold and produced Actual Plan Total industry sales revenue-actual (million) market share Plan Actual Market demand (quantity) Plan Actual EM EI 30 29 150 153 15 16 1 0.98 40 42 15 14.9 65369 82867 28910 24860 26 36 10% 10% 10% 8% 828,670 653,690 248,600 361,375 2018 Annual fixed cost (thousand yuan) Plan Fixed manufacturing cost 1,388,000 Fixed sales expense 250,000 Fixed administrative expenses 320,000 Fixed R&D expenses 318,000 2 / 2 Actual 1,399,000 245,000 325,000 325,000