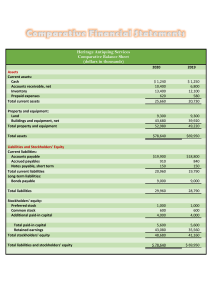

Financial Accounting Preparatory Course Bocconi University a.y. 2023/24 Accounting 20352 - Financial Accounting Preparatory Course Patrizia Tettamanzi Department of Accounting, Via Roentgen, 1 5th Floor – Room A2FM01 Email: patrizia.tettamanzi@unibocconi.it Office Hours: by email you can request an appointment (online and/or at the office) 2 Accounting Course goals The course aims to prepare students, from other graduate-level business courses, to an advanced and relevant knowledge of the financial accounting principles and tools. Upon completion of the course, students are expected to understand the basics of: • accounting terminology; • how to generate accounting information and prepare financial statements; and • how to interpret the accounting information. 3 Accounting Schedule Blackboard Collaborate Ultra: SS 1–2 3–4 5–6 7 -8 9 - 10 11 - 12 4 DATE 28/08 8.30 – 10.00 10.15 – 11.45 29/08 8.30 - 10.00 10.15 - 11.45 30/08 14.45 - 16.15 16.30 - 18.00 31/08 8.30 - 10.00 10.15 - 11.45 01/09 14.45 - 16.15 16.30 - 18.00 02/09 8.30 - 10.00 10.15 - 12.45 TOPICS PROFESSOR Accounting: purposes and tools / Accrual Accounting and Adjusting Revenues and Expenses Patrizia Tettamanzi Accounting Equation and T–Accounting / Sales Revenues and Accounts Receivable. Cost of Good Sold and Inventory Long Lived Assets and Bonds (Straight Line and Effective Interest Amortization methods) / Equity and Investments (Definitions and Common Stock Transactions) / Exercise on T-Account, Ledger, FSs Exercise Trial Balance and Financial Statements (IS and BS) / Cash Flow Statement (and CFS Exercises) Patrizia Tettamanzi Patrizia Tettamanzi Patrizia Tettamanzi Exercise – IS – BS – CFS Patrizia Tettamanzi Analysing Financial Statements Review exercises Patrizia Tettamanzi Accounting Session 1 Accounting Why is Accounting important? 6 Accounting What is Accounting? • Accounting is the information system that measures business activities, processes that information into reports and communicates the results to decision makers. • Accounting provides much information that people use: – to manage businesses; – to evaluate businesses. • to manage: for example, managers must decide what merchandise to buy and sell, what types of assets to acquire for use in the business, how to finance the company. Accounting provides information useful to take the best decision. • to evaluate: both managers and investors need accounting information to evaluate if the company is able to reach its goals or if it’s a profitable investment (in comparison to other investments). 7 Accounting What is Accounting? “Accounting is the language of business.” Collect → Process → Report ? measure record analyze ! Information Decision-Makers (Information Users) A system that collects and processes financial information about an organization and reports that information to decision makers. 8 Accounting Accounting is useful for: • • • • • • Individuals; Managers; Investors and Creditors; Government Regulatory Agencies; Taxing Authorities (businesses pay taxes on profits and assets); Employees (to evaluate the ability to pay salaries and wages). In short, Accounting is storytelling, told by narrators of varying reliability: the goal is to get to the truth, but the path is often convoluted. What do you make of it? 9 Accounting Accounting is useful for different users External Decision Makers 10 Internal Decision Makers Accounting Financial vs. Management Accounting • Financial accounting provides information mostly to external users. • Its primary objective is to provide information useful for making investment and lending decisions. • Management accounting provides mostly confidential information for internal decision makers (for example top executives). • There are very strong links between financial and management accounting. • In order to better understand the differences between financial and management accounting we can think about a firm as an INPUT-OUTPUT system. 11 Accounting Financial vs. Management Accounting • The firm needs economic resources (labor force, buildings, cash,…). These are the inputs of its activity. • The inputs acquired are then processed or transformed inside the firm. • The products of the firm (goods or services) represent the outputs of its activity. INPUTS 12 OUTPUTS Accounting Financial vs. Management Accounting • When the firm buys its inputs and when it sells its products it performs external transactions. • When the firm transforms the inputs into outputs it performs internal processes. • While the external transactions are the object of financial accounting, what happens inside the firm (that is its internal processes) is the primary object of management accounting. • So, we’ll focus our attention on external transactions while dealing with financial accounting. • You will learn about management accounting in a different course. 13 Accounting Financial vs. Management Accounting Financial Management External Reporting Stakeholders Internal Reporting Managers Purpose Financing/Tax/ Unions/... Decision Making Output Financial Statements Reports Scope Subjects 14 Accounting Financial Statements • The key product of financial accounting is the set of financial statements: the documents that report financial information about a business entity to decision makers. • Financial statements tell us how well a business entity is performing in terms of profits and losses and where it stands in financial terms. • The most basic concept in accounting is the entity concept. An accounting entity is an organization that stands apart as a separate economic unit. From an accounting point of view, we need to sharply separate each entity in order not to confuse its affairs with those of other entities. 15 Accounting Financial Statements • In different words, when we prepare a set of financial statements, we do it with reference to a specific entity, whose name is reported on the top of each statement (show slide). • There are three main forms of organizations: – proprietorship, which has a single owner, personally liable for the debts of the business; – partnership, which has two or more owners called partners, personally liable for the debts of the business; – corporation, which has a lot of owners called stockholders or shareholders, not personally liable of the debts of the company. • For our purposes, we’ll refer to a generic “company”. When necessary, we’ll distinguish among the different forms of business. 16 Accounting Financial Statements • The basic set of financial statements is composed of the following: – Balance Sheet (or Statement of financial position); – Income Statement (or Profit & Loss, or Statement of operations); – Statement of Cash Flows. • There are other statements (like, for example, the Statement of retained earnings), but these are less important for our purposes. • Each statement answers a different question about the company’s performance and financial position. 17 Accounting Financial Statements • The Balance Sheet answers the questions: – what are the company’s economic assets and who has claims to them at a certain date (the end of the period)? – What is the company’s financial position at a certain date (the end of the period)? • The Income Statement answers the question: – how well did the company perform during the period? • The Statement of Cash Flows answers the question: – how much cash did the company generate and spend during the period? 18 Accounting Financial Statements Balance Sheet Financial position at a particular point in time: • Assets • Liabilities • Owners’ Equity Statement of Cash Flows The change of the cash balance In/outflows in three categories: • Operating activities • Investing activities • Financing activities 19 Income Statement Financial performance during an accounting period measured as revenues minus expenses Statement of Retained Earnings The change of retained earnings: + net income − dividends Accounting The Accounting Period • For each statement we talk about a “period”. This is the accounting period, that is the period of time depicted by financial statements. • Usually this period corresponds to the calendar year (01.0112.31). • When the accounting year is different from the calendar year, we talk about fiscal year. • The accounting year chosen by each entity is reported on the top of each statement. 20 Accounting The four basic financial statements can be prepared at any point in time such as: ▪ End of the year (for the year ended, annual reports); ▪ Quarterly (for the quarter ended, quarterly reports); ▪ Monthly (for the month ended, monthly reports). The financial statement heading includes: ▪ Name of the entity (Company name); ▪ Title of the statement (e.g., Balance Sheet); ▪ Specific date of the statement (e.g., at December 31, 2018); ▪ Unit of measure (in millions of dollars). 21 Accounting The Balance Sheet ( BS ) • The balance sheet gives a picture of the company’s financial position at the end of an accounting period. • It reports three main categories of items: – Assets; – Liabilities; – Shareholders’ equity. • Assets are the economic resources of a business that are expected to be of benefit in the future (examples: cash, merchandise, buildings, furniture, etc.). • Liabilities are “outsider claims”, that is economic obligations (debts) payable to outsiders (creditors) (example: a loan). • Shareholders’ (or Owners’) Equity represents the “insider claims” to the business resources. These are the assets held by the owners who invested money in the firm. 22 Accounting Balance Sheet Assets Cash Short-Term Investments Accounts Receivable Notes Receivable Inventory (to be sold) Supplies Prepaid Expenses Long-Term Investments Equipment Buildings Land Intangibles The Balance Sheet is a financial snapshot at a specific point in time. 23 Elements of the Balance Sheet Liabilities Accounts Payable Accrued Expenses Notes Payable Taxes Payable Unearned Revenue Bonds Payable Stockholders’ Equity Common Stock Retained Earnings Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 1-23 Exhibit 1.2 Balance Sheet EXPLANATION LE-NATURE’S INC. Balance Sheet At December 31, 2015 (in millions of dollars) Assets: Cash Accounts receivable Inventories Property, plant, and equipment Total assets Liabilities and stockholders’ equity: Liabilities Accounts payable Notes payable to banks Total liabilities Stockholders’ equity Common stock Retained earnings Total stockholders’ equity Total liabilities and stockholders’ equity Name of the entity Title of the statement Specific date of the statement Unit of measure $ 10.6 6.6 51.2 459.0 $527.4 $ 26.0 381.7 407.7 55.7 64.0 119.7 $527.4 Resources controlled by the company Amount of cash in the company’s bank accounts Amounts owed by customers from prior sales Ingredients and beverages ready for sale Factories, production equipment, and land Total amount of company’s resources Sources of financing for company’s resources Financing supplied by creditors Amounts owed to suppliers for prior purchases Amounts owed to banks on written debt contracts Financing provided by stockholders Amounts invested in the business by stockholders Past earnings not distributed to stockholders Total sources of financing for company’s resources The notes are an integral part of these financial statements. 24 Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 1-24 The Accounting Equation A = L + SE Assets Economic Resources Liabilities Stockholders’ Equity Sources of Financing for Resources Stockholders’ Liabilities: Equity: from from Creditors Stockholders The balance sheet reports a company's assets, liabilities, and stockholders' equity at a specific point in time. 25 Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 1-25 The Income Statement ( IS ) • The Income Statement reports the company’s revenues, expenses and net earnings (or income) for the accounting period. • In order to define revenues and expenses we need first to define net earnings • Net earnings represent the result of the business operations. It is the amount earned by income-producing activities. • Revenues are increases in net earnings deriving from sales of goods or services to customers or clients • Expenses are decreases in net earnings. They are the cost of doing business, that is the cost of all the resources used to perform the business’ activity. • Net earnings = revenues - expenses • If net earnings < 0, it is called net loss 26 Accounting Income Statement Revenues Cash and promises received from delivery of goods and services. Examples: Sales Revenue Fee Revenue Interest Revenue Rent Revenue The Income Statement is a measure of performance of the business. 27 Elements of the Income Statement Expenses Resources used to earn period’s revenues. Examples: Cost of Goods Sold Wages Expense Rent Expense Depreciation Expense Insurance Expense Repair Expense Income Tax Expense Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 1-27 The Income Statement Equation R - E = NI Revenues Expenses Cash and promises received from delivery of goods and services. Resources used to earn period’s revenues Net Income Revenues earned minus expenses incurred. Also called “profit”, “net earnings”, or “the bottom line.” If total expenses exceed total revenues, a net loss is reported. 28 Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 1-28 Exhibit 1.3 Income Statement EXPLANATION LE-NATURE’S INC. Income Statement For the Year Ended December 31, 2015 (in millions of dollars) Revenues Sales revenue Expenses Cost of goods sold Selling, general, and administrative expenses Interest expense Income before income taxes Income tax expense Net income Name of the entity Title of the statement Accounting period Unit of measure $275.1 140.8 77.1 17.2 40.0 17.1 $ 22.9 Cash and promises received from sale of beverages Cost to produce beverages sold Other operating expenses (utilities, delivery costs, etc.) Cost of using borrowed funds Income taxes on period’s income before income taxes Revenues earned minus expenses incurred The notes are an integral part of these financial statements. 29 Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 1-29 Statement of Stockholders’ Equity (1 of 2) Common Stock Amounts invested in the business by stockholders. Beginning Common Stock + Stock Issuance Ending Common Stock Retained Earnings Past earnings not distributed to stockholders. Elements of the Statement of Stockholders’ Equity The Statement of Stockholders’ Equity reports the change in each stockholders’ equity account during the period. Beginning Retained Earnings + Net Income − Dividends declared Ending Retained Earnings 30 Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 1-30 Exhibit 1.4 Statement of Stockholders’ Equity EXPLANATION LE-NATURE’S INC. Statement of Stockholders’ Equity For the Year Ended December 31, 2015 (in millions of dollars) Balance December 31, 2014 Net income for 2015 Dividends for 2015 Balance December 31, 2015 Name of the entity Title of the statement Accounting period Unit of measure Common Stock Retained Earnings $55.7 $43.1 22.9 (2.0) $64.0 $55.7 Last period’s ending balances Net income reported on the income statement Dividends declared during the period Ending balances on the balance sheet The notes are an integral part of these financial statements. 31 Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 1-31 Statement of Cash Flows +/- Cash Flows from Operating Activities (CFO) +/- Cash Flows from Investing Activities (CFI) +/- Cash Flows from Financing Activities (CFF) Change in Cash + Beginning Cash Balance Ending Cash Balance /32 Note that each of the three cash flow sources can be positive (net cash inflow) or negative (net cash outflow) Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 1-32 Statement of Stockholders’ Equity (2 of 2) Cash Flows from Operating Activities Cash collected from customers less cash paid for operating expenses such as cash paid to suppliers and employees. Elements of the Statement of Cash Flows Cash Flows from Investing Activities Cash flows related to acquisition or sale of the company’s plant and equipment and investments. Cash Flows from Financing Activities Cash flows from the receipt or payment of money to investors and creditors (except suppliers) The Statement of Cash Flows reports inflows and outflows of cash during the accounting period. 33 Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 1-33 Exhibit 1.5 Statement of Cash Flows EXPLANATION LE-NATURE’S INC. Statement of Cash Flows (Summary) For the Year Ended December 31, 2015 (in millions of dollars) Cash flows from operating activities Cash flows from investing activities Cash flows from financing activities Net increase (decrease) in cash Cash balance December 31, 2014 Cash balance December 31, 2015 $ 87.5 (125.5) 47.0 9.0 1.6 $ 10.6 Name of the entity Title of the statement Accounting period Unit of measure Cash flows directly related to earning income Cash flows from purchase/sale of plant, equipment, & investments Cash flows from investors and creditors Change in cash during the period Last period’s cash on the balance sheet Ending cash on the balance sheet The notes are an integral part of these financial statements. 34 Copyright ©2020 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 1-34 Relationship between Balance Sheet and Income Statement • The income statement reports net earnings (or net loss) as difference between revenues and expenses. • At the same time, net earnings (or net loss) is part of the owners’ equity, since it represents the remuneration for the investment they made in the firm. • We can say that income statement gives details about the increase (in case of net earnings) or decrease (in case of net loss) in the owners’ equity due to the operations performed by the company during an accounting period. 35 Accounting Relationship between Balance Sheet, Income Statement and Cash Flow Statement of Stockholders’ Equity Income Statement Revenues − Expenses Net Income $ 275.1 252.2 $ 22.9 Statement of Cash Flows +/− Cash Flows from Operating Activities $ 87.5 +/− Cash Flows from Investing Activities (125.5) +/− Cash Flows from Financing Activities 47.0 Change in Cash 9.0 + Cash at Beginning of Period 1.6 Cash at End of Period $ 10.6 36 1 Beginning + Net Income − Dividends Ending Common Stock $55.7 $55.7 Retained Earnings $43.1 22.9 (2.0) $64.0 Balance Sheet 3 Cash Other Assets Total Assets Liabilities Common Stock Retained Earnings Total Liabilities & Stockholders’ Equity $ 10.6 516.8 $527.4 $407.7 55.7 64.0 2 $527.4 Accounting The Notes • Did you notice this sentence at the bottom of each financial statement? • All financial statements should be accompanied by notes that provide the reader with supplemental information to help the reader better understand the financial statements. • The notes are also called footnotes. 37 Accounting Financial Statements Format Assets are listed on the balance sheet by ease of conversion to cash. Liabilities are listed by the maturity (due date). Place a single underline below the last item in a group before a total or subtotal, and a double underline below the group totals. Include the monetary unit sign ($) beside the first dollar amount in a group of items and by group total 38 Accounting Accounting Standards Guides and rules that govern accounting practice, regarding how financial statements are prepared and accounting information is presented • GAAP (Generally Accepted Accounting Principles) • IFRS (International Financial Reporting Standards) Prior to 1930’s, each company has self-defined financial reporting practices. Thus, no uniform standard across companies was in practice. Why do we need accounting standards? 39 Accounting Types of Business Entities Sole Proprietorship: owned by a single individual Partnership: owned by two or more individuals Corporation: ownership represented by shares of stock that can be bought and sold and operates separately from its owners Advantages of a Corporation: ➢Stockholders have limited liability ➢Continuity of life ➢Ease in transferring ownership (stock) ➢Opportunity to raise large amounts of money by selling shares of stock to a large number of people Disadvantage of a Corporation: ➢Double taxation (income is taxed when earned and again when distributed to stockholders as dividends) 40 Accounting Quiz and Exercises Determine if each of the following items “belongs” to the income statement or to the balance sheet. Use “IS” for Income Statement, “BS” for Balance Sheet. If the item belongs to the income statement, specify if it is a revenue (R) or an expense (E); if it is a balance sheet item, indicate if it is an asset (A), a liability (L), or a portion of the owners’ equity (OE). 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. 11. 12. 13. 14. 15. 16. 17. 18. 19. 20. 41 Items Cash and cash equivalents Dividends received Dividends paid Inventories Trade payables Investments in subsidiaries Income taxes Cost of goods sold Goodwill Bank loan Interest expense Net income of the current year Property, Plant and equipment Rent revenue Leased assets Provisions for risks and charges Revaluation reserve Trade receivables Retained earnings Depreciation / Amortization expense IS BS Accounting Suggested Bibliography • P. Tettamanzi, G. Blandano & S. Goodman, BASIC ACCOUNTING – How to Prepare and Analyze Financial Statements, IPSOA, Last Edition, ISBN: 978-88-217-5060-1. • M. Barber & S. Parry, Accounting and Finance for Managers: a Business Decision-Making Approach, Kogan Page, 3rd Edition, 2021, ISBN: 978-1-78966-751-6. 42 Accounting