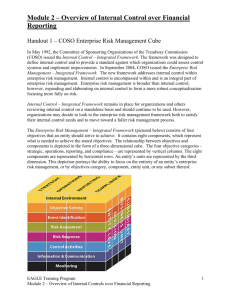

MAKERERE UNIVERSITY COLLEGE OF BUSINESS AND MANAGEMENT SCIENCES SCHOOL OF STATISTICS AND PLANNING DEPARTMENT OF PLANNING AND APPLIED STATISTICS BACHELOR’S DEGREE OF SCIENCE IN BUSINESS STATISTICS. COURSE WORK ASSIGNMENT F0R RISK MANAGEMENT FOR BUSINESS (BBS 3206) DETAILS OF MEMBERS NAME REGISTRATION NUMBER STUDENT NUMBER NANTONGO LYDIA 20/U/0393 2000700393 NABWONSWO PHIONA ELIZABETH 20/U/12046/PS 2000712046 SSERWADDA FAHAD 20/U/11937/PS 2000711937 SIGNATURE QUESTION ONE Over a decade ago, the Committee of Sponsoring Organizations of the Treadway Commission (COSO) issued Internal Control – Integrated Framework to help businesses and other entities assess and enhance their internal control systems. That framework has since been incorporated into policy, rule, and regulation, and used by thousands of enterprises to better control their activities in moving toward achievement of their established objectives. The Committee of Sponsoring Organizations of the Treadway Commission (COSO) released its updated Internal Control – Integrated Framework (2013 Framework). (a) Define the term internal control as stipulated in the 2013 Framework. (b) The 2013 Framework lists three categories of objectives, similar to the 1992 Framework. List and explain them. (c) The five components of internal control are the same in both the 1992 and 2013 Frameworks; State and explain the five components as well as their respective principles as per the 2013 framework. (d) What are the limitations of Internal Control as acknowledged by the 2013 Framework? (e) The 2013 Framework further points out the importance of effective documentation of the organization’s system of internal control. State the reasons why? 1a) Define the term internal control as stipulated in the 2013 Framework The Committee of Sponsoring Organizations of the Treadway commission was organized in 1985 and its goal is to provide thought leadership dealing with three interrelated subjects: enterprise risk management, internal control and fraud deterrence. In 1992 COSO published Internal Control – Integrated Framework which was revised and rereleased in May 2013 with various changes to its objectives. The 2013 COSO Framework defines internal control as a process effected by an entity’s board of directors, management, and other personnel, designed to provide reasonable assurance regarding the achievement of objectives relating to operations, reporting, and compliance. 1b) The 2013 Framework lists three categories of objectives, similar to the 1992 Framework. List and explain them Operations objectives This is meant to focus on efficiency of operations which looks at whether the operations procedures are efficient, effectiveness of operations which looks at whether the controls are properly designed and operating effectively, operation and financial performance goals which looks whether the goals are realistic and safeguarding assets against loss which looks at whether the organization safeguards its assets against loss. Reporting objectives This meant to focus on internal and external financial and non-financial reporting to stakeholders. This looks at whether the organizations reports are; reliable i.e. free from bias, errors or misleading information timely i.e. delivered or produced promptly within expected or required timeframe transparency i.e. providing a comprehensive view of data, methods and assumptions used to produce report findings. Compliance objectives This meant to focus on adhering to laws and regulations by the entity. This ensures that the entity remains in compliance with the standards and regulations that its clients care about. 1c) The five components of internal control are the same in both the 1992 and 2013 Frameworks; State and explain the five components as well as their respective principles as per the 2013 framework Control Environment The control environment is the set of standards, processes, and structures that provide the basis for carrying out internal control across the organization. Control environment factors include; integrity, ethical values and competence of the entity’s people. The principles of the control environment as per 2013 framework include; Management establishes, with board oversight, structures, reporting lines, and appropriate authorities and responsibilities in the pursuit of objectives. The organization demonstrates a commitment to attract, develop, and retain competent individuals in alignment with objectives. The organization demonstrates a commitment to ethical values and integrity by setting the tone at the top and establishing a culture that promotes ethical behavior. The board of directors demonstrates independence from management and exercises oversight of the development and performance of internal control. The organization holds individuals accountable for their internal control responsibilities and takes corrective action when necessary. Risk assessment This is the identification and analysis of the relevant risks to achievement of objectives, forming a basis for determining how the risks should be managed. Risk assessment are performed to evaluate internal and external factors. Assessments provide reasonable assurance that organizations are managing risks to an acceptable tolerance. The principles of the risk assessment as per 2013 framework include; The organization specifies its objectives at the entity, division, and operating unit levels and identifies risks to the achievement of those objectives. The organization identifies and analyzes risks to the achievement of its objectives, considering both the likelihood and impact of those risks. The organization assesses the risk of fraud that could result in a material misstatement of the financial statements, and evaluates the design and effectiveness of the related controls. The organization identifies and assesses changes that could significantly impact its internal control system, including changes in personnel, systems, and processes, as well as changes in the external environment. Control activities This refers to policies, procedures and practices that an organization puts in place to minimize the risk of errors, fraud or other irregularities. They include a range of activities such as approvals, authorizations, verifications, reconciliations, review of operating performance and security of assets. The three principles relating to Control Activities as per 2013 framework are; The organization selects and develops control activities that contribute to the mitigation of risks to the achievement of objectives to acceptable levels. The organization selects and develops general control activities over technology to support the achievement of objectives. The organization deploys control activities through policies that establish what is expected and in procedures that put policies into action. Information and communication Information is necessary for an organization to carry out internal control responsibilities such as generating reports and providing feedback to management in support of achievement of organizations objectives Effective communication must occur in a broader sense, flowing down across and up the organization this enables personnel to understand internal control responsibilities and there importance to achievement of the objectives The three principles relating to Information and Communication as per 2013 framework are; The organization obtains or generates and uses relevant, quality information to support the functioning of internal control. The organization internally communicates information, including objectives and responsibilities for internal control, necessary to support the functioning of internal control. The organization communicates with external parties about matters affecting the functioning of internal control. Monitoring Activities Monitoring is a process that assesses the quality of the systems performance over time. The purpose of monitoring is to identify potential weaknesses or failures in internal control, to correct them and provide feedback to management about effectiveness of internal control. Evaluations are made to find out each of the five components of the internal control are present and functioning. The two principles relating to Monitoring Activities are: The organization selects, develops, and performs ongoing and/or separate evaluations to ascertain whether the components of internal control are present and functioning. The organization evaluates and communicates internal control deficiencies in a timely manner to those parties responsible for taking corrective action, including senior management and the board of directors, as appropriate. 1d) What are the limitations of Internal Control as acknowledged by the 2013 Framework? Internal control is a vital component of any organization, and it is recognized as a means of ensuring that the organization achieves its objectives. However, the 2013 Framework on Internal Control acknowledges that there are some limitations to internal control. Below are the limitations of Internal Control as acknowledged by the 2013 Framework Management Override: Managers of the organization in some situations may ignore established internal control measures to achieve their goals. This can take form of misappropriating assets for personal gains, intentionally ignoring control weaknesses which limits internal control as acknowledged by the 2013 Framework. Cost: Implementation of internal control systems is expensive especially for small businesses. For example, hiring external consultants, purchasing software and hardware, redesigning existing processes. This limits the implementation of internal control system due to the failure to meet the related costs. Limited Scope: Internal control only provides reasonable assurance that the objectives of the organization are achieved. But does not guarantee that the organization's objectives will be fully met. For instance, an internal control system may not detect all fraudulent activities, and it is not a guarantee that a company will avoid financial losses caused by economic factors beyond its control. Collusion: This refers to the conspiring of two or more people with an aim of achieving a fraudulent or illegal objective. For instance, a sales agent may team up with a customer to fabricate sales transactions. Such collusion can bypass the internal control system, leading to financial misstatements. Human error: People who design and put into effect the internal control systems are prone to making errors For example, an accountant may post a transaction to the wrong account or enter wrong figures in financial statements which may lead to misinterpretation of the financial position of the company. External factors: Internal control systems are designed to operate within the boundaries of the organization. However, external factors may prevent an organization from reaching its objectives such as changes in economic conditions, laws, and regulations can affect the effectiveness of internal control. An example could be change in the laws that an organization is meant to comply with, this would make the system less efficient. Size of the organization: The size of an organization can also limit the effectiveness of internal control systems in that, small businesses may not have the resources to implement and maintain a fortified internal control system. For instance, a sole proprietorship may not have the staff, technology, or financial resources required to implement internal control systems. As a result, the owner may be forced to rely on manual processes that are prone to errors. Unforeseeable circumstances: These are events that cannot be predicted and therefore are invulnerable to internal controls that have been set up by an organization. Such events include natural disasters like earthquakes that could disrupt the organizations operations even with the most impenetrable internal controls in place. Inherent limitations: These are limitations that arise in any system regardless of the nature of the internal controls. They come up due to many reasons such as collusion, management override and human error. In conclusion, internal control systems have limitations that organizations should be aware of to ensure that the systems are effective in achieving their objectives. Organizations should periodically assess their internal control systems to identify weaknesses and limitations and make necessary improvements. 1e) The 2013 Framework further points out the importance of effective documentation of the organization’s system of internal control. State the reasons why? The 2013 framework defines effective documentation of an organization's system of internal control as documentation that provides a clear understanding of the organization`s system of internal control. Below are the reasons why the 2013 Framework further points out the importance of effective documentation of the organization’s system of internal control. Providing Evidence of Compliance: Proper documentation of internal controls provides evidence that the organization is complying with laws, regulations, and industry standards by providing a record of controls that have been implemented and the processes used to manage risks and achieve objectives. This can be useful in case of audits or legal challenges. Improving Communication: Documentation ensures that employees understand the internal control system hence promoting better communication among team members. This brings about togetherness which in turn improves internal control systems and avoid errors. Facilitating Training: Documentation can also serve as a training tool for new employees of the organization to understand the organization's internal control system, as well as provide ongoing training to existing employees. Supporting Continuous Improvement. Through documentation, an organization is able to identify gaps and weaknesses in its internal control systems and this information enables the organization identify areas that need enhancement. Regular reviews of documentation can help refine and strengthen internal control systems. Enhancing Accountability: With proper documentation, individuals with specific control activities can be identified and held accountable should errors or fraud occur. This establishes accountability for internal control in the organization. Facilitating Oversight: Documentation helps to facilitate oversight of internal control activities by the board of directors, audit committee, and external auditors i.e. management and other stakeholders get a clear understanding of the processes, procedures and controls in place to mitigate risks. This oversight can help to identify weaknesses in the internal control system and prevent fraud and errors. Increasing Efficiency: Proper documentation of internal control processes can help to streamline operations, reduce redundancies, and improve efficiency. This can result in cost savings for the organization and better use of resources. Enabling Risk Management: Documentation helps the organizations to better understand the effectiveness of its internal controls and the level of risk associated with its operations. This can enable the organization to develop risk mitigation strategies and prioritize control activities based on their impact on the organization. Ensuring Consistency: Documentation helps to ensure that internal control activities are performed consistently across the organization i.e. it provides a clear understanding of the organizations control systems across all levels of the organization. This consistency is important for maintaining the integrity of the internal control system and achieving the organization's objectives. Providing Historical Records: Documentation provides a historical record of internal control activities, which can be useful for tracking changes in the system over time and identifying trends that may require attention. In summary, effective documentation of an organization's system of internal control is essential for promoting compliance, communication, training, continuous improvement, accountability, oversight, efficiency, risk management, consistency, and historical record-keeping. QUESTION TWO (a) Define the term Enterprise risk management as per COSO. (b) What are the seven fundamental concepts reflected in the definition provided in (a) above? (c) The enterprise risk management framework is geared to achieving an entity’s objectives, set forth in four categories. State and briefly explain them. (d) Enterprise risk management consists of eight interrelated components. State and briefly explain them. 2a) Define the term Enterprise risk management as per COSO. Enterprise risk management is a process, effected by an entity’s board of directors, management and other personnel, applied in strategy setting and across the enterprise, designed to identify potential events that may affect the entity, and manage risk to be within its risk appetite, to provide reasonable assurance regarding the achievement of entity objectives. 2b) What are the seven fundamental concepts reflected in the definition provided in (a) above? Below are the seven fundamental concepts reflected in the definition in (a) above. Enterprise risk management is: A process: It is ongoing and continuous. It involves a series of interconnected activities or steps that are performed over time. Effected by people at every level of an organization: These include the board of directors, management and other personnel of the organization. These actively make the process of enterprise risk management happen. Applied in strategy setting: This is by integrating risk management considerations into the development and implementation of an organization’s overall strategic plan. Applied across the enterprise: The enterprise risk management considerations are integrated into all aspects of the organization, from strategic planning to daily operations. Designed to identify potential events that, if they occur, will affect the entity: By identifying these potential events in advance, organizations can develop strategies and plans to mitigate the risks associated with them and minimize their impact. Able to provide reasonable assurance to an entity’s management and board of directors: It gives the organization confidence that it is likely to achieve its objectives Geared to achievement of objectives in one or more separate but overlapping categories: It is designed to help an organization achieve its objectives across multiple areas that may be distinct but also interconnected. 2c) The enterprise risk management framework is geared to achieving an entity’s objectives, set forth in four categories. State and briefly explain them Compliance: This related to complying with laws and regulations applicable law to an organization. Compliance helps organizations to ensure that they are operating within legal and ethical boundaries, and that they are meeting their obligations to stakeholders hence mitigating risks related to non-compliance. Operations: This relates to efficient and effective use of an organization’s resources. Efficient use of resource involves using resources in a way that minimizes waste and maximizes output. Effective use of resources involves using resources in a way that contributes to the achievement of the organization’s objectives. Strategic: This relates to organization’s long-term goals and plans for achieving its mission and vision. These goals and plans guide an organization’s overall direction and decision-making. Reporting: This relates to the reporting of financial and non-financial information of an organization. It focuses on reliability of reporting that is to say accuracy completeness and trustworthy of reports. 2d) Enterprise risk management consists of eight interrelated components. State and briefly explain them? Enterprise Risk Management is a structured, continuous process used by organizations to identify, assess, and manage potential risks that may affect their operations, goals, objectives, and reputation. Below are the eight components of Enterprise Risk Management (ERM) that you need to know: Internal Environment: This component refers to the organization's culture, values, ethics, and tone at the top. It sets the foundation for how risk management is viewed and practiced within the organization. Objective Setting: This component involves setting goals and objectives that are aligned with the organization's mission and vision. It also involves identifying the risks that may affect the achievement of these objectives. Event Identification: This component involves identifying the events or risks that may affect the organization's objectives. This step helps the organization to be proactive in managing risks rather than reactive. Risk Assessment: This component involves evaluating the likelihood and impact of identified risks on the organization's objectives. This step helps the organization to prioritize risks and allocate resources accordingly. Risk Response: This component involves developing strategies to manage the risks that have been identified. This step helps the organization to reduce, avoid, transfer, or accept risks depending on their appetite for risk. Control Activities: This component involves implementing policies, procedures, and processes to manage the risks that have been identified. This step helps the organization to ensure that the risk management strategies are effective. Information and Communication: This component involves communicating information about risks and their management across the organization. This step helps the organization to ensure that everyone is aware of the risks and their roles in managing them. Monitoring: This component involves monitoring and reviewing the effectiveness of the risk management strategies that have been implemented. This step helps the organization to continuously improve its risk management practices. REFERENCES Rejda, G. E., & McNamara, M. J. (2018). Principles of Risk Management and Insurance (14th ed.). Pearson. Aven, T. (2016). Risk assessment and risk management: Review of recent advances on their foundation. European Journal of Operational Research, 253(1), 1-13. Hillson, D., & Murray-Webster, R. (2017). Understanding and managing risk attitude (2nd ed.). Routledge.