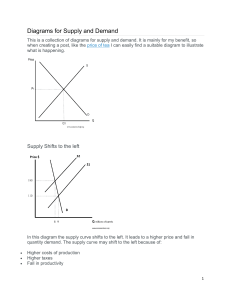

Identification Economics- A social science concerned with the production, distribution and consumption of goods and services to satisfy the unlimited wants and needs of the people. Managerial Economics – A discipline that deals with the application of economic theory to business management. It deals with the use of economic concepts and principles of business decision-making. Scarce – The best description that is always given to the resources. It means that the resources are not enough to produce goods and services for the unlimited needs and wants of the people. Win-win situation- It describes where participation in a business transaction gives mutual benefits. Economic Relationship – An atmosphere where relationships can be formed and people can interact for mutual gains is essential for growth. A market is often where the producers and consumers meet for a successful business transaction. Equi-Marginal Principle – A preposition that states that input should be allocated in such a way that value added by the last unit is the same in all uses. Equilibrium Quantity – The quantity bought and sold at the equilibrium. Marginal Benefit – Additional Revenue earned by selling an additional unit of the output. Demand Schedule – Tabular representation of different quantities of commodities demanded at varying price. The supply curve shifts when there is a change in quantity supplied due to the other factors other than the PRICE. When the supply increases the supply curve shifts to the RIGHT. Market Supply Curve – It shows the relationship between the price and quantity supplied of a particular product. True or False True – Opportunity Cost: is part of the decision-making that you sacrifice over the course of action and influences people’s choices. When there are a lot of options to choose from, people tend to go with the most convincing one. False – There is an attraction point when people do not get positive incentives with the offer they jump in. True – A booming economy means businesses meet consumer needs and therefore they also improve their living standards. False – When there is too much money in circulation, inflation sets in. People’s purchasing capacity decreases and the prices of goods would decrease astronomically. True – Managerial economics is multidisciplinary in nature wherein other related disciples such as mathematics, accounting, science, finance, and etc. Will be using the principle underlying in it. Enumerate and explain briefly The types of Managerial Economics - Normative Managerial Economics - Liberal Managerial Economics - Radical Managerial Economics The Principles of Managerial Economics - Principles of decision-making - Principles of Business Communication - Principles of Economic Function Nature of Managerial Economics - Scientific - As an Art - Administrative - Resource Control - Micro-Economic - Macroeconomic - Dynamic - Multidisciplinary - Prescriptive - Management-driven Factors of Production - Land - Labor - Capital - Entrepreneurship Multiple Choice 1. If a marginal benefit is greater than marginal cost, a rational choice involves: a more of the activity. 2. The quantity demanded for Pepsi has decreased. The best explanation for this is that: The price of Pepsi increased. 3. Demand curves are derived while holding constant: Income, tastes, and the price of other goods. 4. If the demand for coffee decreases as income decreases, coffee is an inferior good. 5. Market equilibrium exists when quantity demanded equals quantity supplied at the prevailing price. 6. There is a change in the quantity demanded of a product when: The product’s price falls. 7. If input price increase, all else equal, supply will decrease. 8. An excise tax placed on the producer of an item will shift the supply curve to the left. 9. In a competitive market, the market demand is 𝑄𝑑 = 48 − 5𝑃 and the market supply is 𝑄𝑠 = 7𝑃. A price ceiling of $5 will result in a shortage of: none of the above [surplus of 12 units] 10. The law of demand indicates that as the price of a good decrease, the quantity: a buyer’s desire increases. 11. When an economist refers to a product as a “normal good” it implies that when income declines, demand for that product will fall. 12. If the government decreased the restrictions on allowable pollution emission levels, then the supply curve for a chemical manufacturer that emits some air pollutants will shift to the right. 13. Which of the following is most likely to shift the supply curve for electricity to the right? A decrease in the price of coal, an input to producing electricity. 14. If an increase in the price of hot tea decreases the demand for honey, this indicates that the two goods are complements. 15. Producer surplus is measured as the area above the supply curve and below the market price. 16. Holding all else constant, as additional firms enter an industry more output is available at each given price. Application of Market Forces 1. The demand curve for product X is given by 𝑄𝑥𝑑 = 300 − 2𝑃𝑥. Find the inverse demand 𝟏 𝟐 curve 𝑷𝒙 = 𝟏𝟓𝟎 − 𝑸𝒙𝒅 2. Suppose demand and supply are given by 𝑄𝑑 = 60 − 𝑃 and 𝑄𝑠 = 𝑃 − 20. What is the equilibrium quantity and price in this market? Q= 20 P=40 Solution: 60 − 𝑃 = 𝑃 − 20 𝑃 + 𝑃 = 60 + 20 2𝑃 = 80 = 𝑄𝑑 = 60 − 40 𝑸𝒅 = 𝟐𝟎 𝑷 = 𝟒𝟎 3. Suppose demand and supply are given by 𝑄𝑥𝑑 = 14 − 12 𝑃𝑥 and 𝑄𝑥𝑠 = 14𝑃𝑥 − 1. a. Determine the equilibrium price and quantity. Show the equilibrium graphically Solution: 14 − 12𝑃𝑥 = 14𝑃𝑥 − 1 15 14𝑃𝑥 + 12𝑃𝑥 = 14 + 1 𝑄𝑥𝑠 = 14( ) − 1 26 26𝑃𝑥 15 = 26 26 𝑸𝒙𝒔 = 𝟕. 𝟎𝟖 𝟏𝟓 𝑷𝒙 = 𝟐𝟔 b. Suppose a $12 excise tax is imposed on the good. Determine the new equilibrium price and quantity. 4. Suppose the demand for good X is given by 𝑄𝑑𝑥 = 10 − 2𝑃𝑥 + 𝑃𝑦 + 𝑀. The price of good X is $1, the price of good Y is $10, and income is $100. Given these prices and income, how much of good X will be purchased? Solution: 𝑄𝑑𝑥 = 10 − 2(1) + 10 + 100 = 10 − 2 + 10 + 100 = 𝟏𝟏𝟖 𝒖𝒏𝒊𝒕𝒔 𝒘𝒊𝒍𝒍 𝒃𝒆 𝒔𝒐𝒍𝒅. 5. Supposed the demand for X is given by 𝑄𝑥𝑑 = 100 − 2𝑃𝑥 + 4𝑃𝑌 + 10𝑀 + 2𝐴, where Px represents the price of good X, Py is the price of good Y, M is income, and A is the amount of advertising on good X. If advertising in Good X increases by $10,000, then demand for X will increase by $20,000. 6. Suppose the demand –for X is given by 𝑄𝑥𝑑 = 100 − 2𝑃𝑥 + 4𝑃𝑦 + 10𝑀 + 2𝐴, where Px represents the price of good X, Py is the price of good Y, M is income, and A is the amount of advertising on good X. Good X is normal good. 7. The supply function for good X is given by 𝑄𝑥𝑠 = 1,000 + 𝑃𝑥 − 5𝑃𝑦 − 2𝑃𝑤, where Px is the price of X Py is the price of good Y, and Pw is the price of input W. If Px = 100. Py= 150, and Pw= 50, the supply curve is: Qxs= 250 Solution: 𝑄𝑥𝑠 = 1,000 + 100 − 5(150) − 2(50) = 1,000 + 100 − 750 − 100 𝑸𝒔𝒙 = 𝟐𝟓𝟎 8. Given a linear demand function of the form 𝑄𝑥𝑑 = 100 − 0.5𝑃𝑥, find the inverse linear demand function. 𝑷𝒙 = 𝟐𝟎𝟎 − 𝟐𝑸𝒙𝒅 𝑸𝒙𝒅 𝟏𝟎𝟎 𝟎.𝟓𝑷𝒙 Solution : = 𝟎.𝟓 𝟎.𝟓 𝟐𝑸𝒙𝒅 = 𝟐𝟎𝟎 − 𝑷𝒙 𝑷𝒙 = 𝟐𝟎𝟎 − 𝟐𝑸𝒙𝒅 9. Given a linear demand function of the form 𝑄𝑥𝑑 = 500 − 2𝑃𝑥 − 3𝑃𝑦 + 0.01𝑀,find the inverse linear demand function assuming M=20,000 and Py= 10 𝑄𝑥𝑑 = 500 − 2𝑃𝑥 − 3(10) + .01(20,000) 670 1 𝑃𝑥 = − 𝑄𝑥𝑑 𝑄𝑥𝑑 = 500 − 2𝑃𝑥 − 30 − 200 2 2 𝑸𝒅𝒙 = 𝟔𝟕𝟎 − 𝟐𝑷𝒙 𝑷𝒙 = 𝟑𝟑𝟓 − 𝟎. 𝟓𝑸𝒙𝒅 10. Given a linear supply function of the form 𝑄𝑥𝑠 = −10 + 5𝑃𝑥, find the inverse linear supply function. 𝑷𝒙𝒔 = 𝟐 + Solution: 𝟓𝒑𝒙 𝟓 𝟏 𝑸𝒙𝒔 𝟐 𝟏𝟎 𝑸𝒙𝒔 = 𝟏 𝟓 𝑷𝒙𝒔 = 𝟐 + 𝑸𝒙𝒔 𝟐 11. The demand curve for product X is given by 𝑄𝑥 = 50 − 2𝑃𝑥. How much consumer surplus do consumers receive when Px= $5? $40 Solution: 𝑄𝑥 = 50 − 2(40) = 50-80 = -40 12. Consider a market characterized by the following inverse demand and supply functions : Psx= 40-4Qx and Px = 10 + 2 Qx. Compute the surplus received by the consumers and producers. Application of Comparative statistics analysis 1. In early 1998, crude oil prices fell to a nine-year low at $13.28 a barrel. Falling crude oil prices were due in part to the technological advances that made locating reservoirs and extraction cheaper. What impact do lower crude oil prices have on the price of gasoline? Use a graph for your explanation. S1 S2 $13.2 P2 EQ Q2 2. Apples and oranges are substitutes. A freeze in Florida destroyed most of the orange crop. What would you expect to happen to the market for the following? Z Oranges? b. Apples? C. Orange juice? Use the diagram to illustrate your answer. P The market price for orange increased and the quantity supply for orange will decrease. S2 S1 P2 P1 Q2 Q1 Q P The market price for apple will increased and the quantity demanded for apple will increase as well. S2 S1 P2 P1 Q1 Q2 Q P S2 The market price for orange juice will increase and the quantity supply for orange juice will decrease. S1 P2 P1 Q2 Q1 Q Important notes: Accounting Profits : =total amount of money taken from sales – cost of producing goods or services (explicit cost). Economic Profits: = total revenue – economic cost Note: economic cost = implicit + explicit cost Implicit cost- cost of the resource Explicit cost- cost of giving up the best alternative use of the resource. Profit = Revenue- Cost Consumer-Producer Rivalry = competing interest of consumers and producers Consumer-consumer rivalry= rivalry among consumers, reduces negotiating power of consumers in the market. Producer-Producer rivalry= consumers compete with one another for the right to service the customers available. Present Value = ( ) Net Benefit = Total Benefits – Total Cost Marginal Benefit = Change in total Benefit divided by Change in the control variable [Q] Marginal Cost = Change in the total cost divided by change in the control variable [Q] Marginal Principle = Benefits equal cost Note: if MB>MC = we benefit MB<MC = no benefits Shift to the right means increase Shift to the left means decrease Law of Demand: As price of a good rises (falls) and all other things remain constant, the quantity demanded of the good falls (rises) Demand Shifters: Income - Normal good: good for which an increase (decrease) in an income leads to an increase (decrease) in the demand for that good. - Inferior good: good for which an increase (decrease) in an income leads to a decrease (increase in the demand for that good. Prices of related goods - Substitute goods: goods for which an increase (decrease) in the price of one good leads to an increase (decrease) in the demand for the other good. - Complement goods: goods for which an increase (decrease) in the price of one good leads to a decrease (increase) in the demand for the other good. Advertising and consumer taste - Informative advertising - Persuasive advertising Population Consumer’s expectation Other factors Linear Demand Function : 𝑄𝑥𝑑 = 𝑎 + 𝑎 𝑃 + 𝑎 𝑃 + 𝑎 𝑀 + 𝐴 𝐻 Qxd: the number of units of good x demanded Px: Price of good x Py: Price of a related good y M: income H: value of any other variable affecting demand Magnitude - If price of x is less than 0, law of demand prevails - If price y is more than 0, good y is a good substitute - If price y is less than 0, good y is a complementary good - If income is less than 0, good x is an inferior good - If income is more than 0, good x is a normal good Consumer Value: maximum amount a consumer is willing to pay at different quantities Total Expenditures: price times the number of units consumed Consumer Surplus: extra value that consumers derive from a good but do not pay extra for. Law of Supply: As price of a good rises (falls). The quantity supplied of the good rises(falls), holding other factors affecting constant. Supply Shifters: Input prices (if input prices increase, supply decreases) Technology or government regulation (if technology increase, production and supply will increase) Number of firms - Entry - Exit Substitute of production Taxes - Excise Tax - Ad valorem Tax Producers expectation Producer Surplus- the amount of producers receive in excess of the amount necessary to induce them to produce goods. Market Equilibrium- price balances supply and demand Price restriction Price floor(to avoid surplus)- minimum legal price that can be charged Price ceiling (to avoid shortage)- Maximum legal price that can be charged Linear Supple Function: 𝑄𝑥𝑠 = 𝛽 + 𝛽 𝑃 + 𝛽 𝑊 + 𝛽 𝑃 + 𝛽 𝐻 Qxs: the number of units of good x produces Px: Price of good x W: Price of an input Pr: Price of technologically related goods H: value of any other variable affecting supply Magnitude - If price of x is more than 0, law of supply prevails - If price of input is less than 0, increase in input price - If price of technologically related goods is more than 0, technology lowers the cost of producing good x Converting Linear supply function to Inverse Supply Function Example: 𝑄𝑥 = 3𝑃𝑥 − 400 400 1 𝑃𝑥 = + 𝑄𝑥𝑠 4 3 1 𝑃𝑥 = 100 + 𝑄𝑥𝑠 3 Elasticity- measure of responsiveness of one variable to changes in another variable Elastic demand- when an increase in price reduces the quantity a lot and vice versa Inelastic demand- change in price causes a smaller percentage change in demand Determinants of Elasticity Demand 1. Numbers of substitute 2. Time horizon 3. Classification of good 4. Necessities vs luxury 5. Size of purchases Cross Price Elasticity of the demand- measures the responsiveness of demand for good X following a change in the price of good Y (a related good) % 𝑐ℎ𝑎𝑛𝑔𝑒 𝑖𝑛 𝑞𝑢𝑎𝑛𝑡𝑖𝑡𝑦 𝑑𝑒𝑚𝑎𝑛𝑑𝑒𝑑 𝑜𝑓 𝑝𝑟𝑜𝑑𝑢𝑐𝑡 𝐴 𝐶𝐸𝐷 = % 𝑐ℎ𝑎𝑛𝑔𝑒 𝑖𝑛 𝑝𝑟𝑖𝑐𝑒 𝑜𝑓 𝑝𝑟𝑜𝑑𝑢𝑐𝑡 𝐵 Point Elasticity Formula (𝑄2 − 𝑄1)/𝑄1 𝐸𝑑 = (𝑃2 − 𝑃1)/𝑃1 Arc or Midpoint CED formula 𝑄2 + 𝑄1 (𝑄2 − 𝑄1)/[ ] 2 𝐶𝐸𝐷 = (𝑃2 + 𝑃1} (𝑃2 − 𝑃1)/[ ] 2 In cross elasticity, if the elasticity is positive, they are substitute goods, if the elasticity is negative, they are complementary. Income Elasticity of demand (YED)- shows how the demand shows how responsive the demand for a product is to a change in (real) income. % 𝑐ℎ𝑎𝑛𝑔𝑒 𝑖𝑛 𝑡ℎ𝑒 𝑞𝑢𝑎𝑛𝑡𝑖𝑡𝑦 𝑑𝑒𝑚𝑎𝑛𝑑𝑒𝑑 𝑌𝐸𝐷 = % 𝑐ℎ𝑎𝑛𝑔𝑒 𝑖𝑛 𝑟𝑒𝑎𝑙 𝑖𝑛𝑐𝑜𝑚𝑒 In income elasticity, we distinguish the following: 1. Normal good- they have a positive income elasticity 2. Luxury goods- Where the income elasticity is greater than 1 3. Necessities- here the income elasticity is greater than 0 and between 1 4. Inferior products- they have negative income elasticity Income elasticity of Normal, luxury good Income elastic demand > 1 Income elasticity of Normal, necessity Income inelastic demand is a positive number less than 1 Income elastic= 1 Normal Unit income elastic Income elasticity of Inferior good Income inelastic demand is a negative number Elasticity and total revenue- total revenue is maximized when demand is unitary elastic Elastic demand: price increase (decrease) leads to a decrease (increase) in total revenue. [P and R move together] Inelastic demand: Price increase (decrease) leads to an increase (decrease) in total revenue [P and R Move opposite] Perfectly elastic: infinite elasticity of demand, demand elasticity is zero [P moves and R stays the same] Elasticity of Supply: percentage change in quantity supplied over the change in the price % change in quantity supplied % change in the price If supply is elastic, producers can increase their output without a rise in cost or time delay Ex: supplier has plenty of spare capacity to increase output high stock levels are available to meet rising demand short production time frame to get products to market ease of factor substitution is high If supply is inelastic, firms find it hard to change their production in a given time period. Ex: Firm operating close to full capacity. Running out of raw materials. The Short term. Limited factors of production. Low levels of stocks. Planning restrictions. Magnitude - When the Price elasticity supply is greater than 1, then supply is elastic - When the Price elasticity supply is less than 1, then supply is inelastic - When the Price elasticity supply is equal 0, then supply is perfectly inelastic. Factors affecting Price elasticity of supply/ determinants of elasticity supply 1. Spare production capacity 2. Stocks of finished products and components 3. Ease and cost of factor substitution/factor mobility 4. Time period and production speed