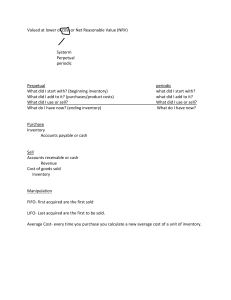

1. A bank statement provided by the bank includes ➢ the beginning and ending balance of the depositors account 2. The purpose of the purchase order is to ➢ Order goods from vendors 3. Which department is least likely to be involved in the revenue cycle? ➢ Credit 4. Which department is responsible for approving changes in pay rate for employees? ➢ Personnel 5. When searching for unrecorded liabilities at the end of an accounting period, the accountant would search all of the files except ➢ Cash receipts file 6. Which document is not prepared by the sales department? ➢ Bill of lading 7. in a computerized system that uses an economic order quantity (EOQ) model and the perpetual inventory method, who determines when to reorder inventory? ➢ the computer system 8. The document which will close the open purchase requisition file is the ➢ receiving report 9. Copies of a purchase order are sent to all of the following except ➢ general ledger 10. Which document triggers the update of the inventory subsidiary ledger? ➢ Stock release 11. Name a compensating control ➢ Supervision 12. The open purchase order in the purchasing department is used to determine? ➢ the orders that have not been received 13. All of the following departments have a copy of the purchase order except ➢ General ledger 14. The purchase order ➢ indicates item description, quantity, and price 15. The reason that a blind copy of the purchase order is sent to receiving is to ➢ force a count of the items delivered 16. The receiving report is used to ➢ accompany physical inventories to the storeroom or warehouse 17. When a copy of the receiving report arrives in the purchasing department, it is used to ➢ recognize the purchase order as closed 18. The financial value of a purchase is determined by reviewing the ➢ supplier's invoice 19. In a merchandising firm, authorization for the payment of inventory is the responsibility of ➢ accounts payable 20. In a merchandising firm, authorization for the purchase of inventory is the responsibility of ➢ inventory control 21. When purchasing inventory, which document usually triggers the recording of a liability? ➢ Supplier’s invoice 22. Because of time delays between receiving inventory and making the journal entry ➢ liabilities are usually understated 23. Usually the open voucher payable file is organized by ➢ payment due date 24. Which of the following statements is not correct? ➢ the sum of the paid vouchers represents the voucher payable liability of the firm 25. In the expenditure cycle, general ledger does not ➢ post the journal voucher from the purchasing department 26. The documents in a voucher packet include all of the following ➢ Purchase order ➢ Receiving report ➢ Supplier’s invoice 27. The cash disbursement clerk performs all of the following tasks ➢ reviews the supporting documents for completeness and accuracy ➢ prepares checks ➢ marks the supporting documents paid 28. When a cash disbursement in payment of an accounts payable is recorded ➢ the liability account is decreased 29. Authorization for payment of an accounts payable liability is the responsibility of ➢ accounts payable 30. Of the following duties, it is most important to separate ➢ warehouse from inventory control 31. In a firm with proper segregation of duties, adequate supervision is most critical in ➢ Receiving 32. The receiving department is not responsible to ➢ order goods from vendors 33. The major risk exposures associated with the receiving department include all of the following except ➢ the audit trail is destroyed 34. Which of the following situations represents a serious control weakness? ➢ Paychecks are distributed by the employees' immediate supervisor 35. Which document is least important in determining the financial value of a purchase? ➢ purchase requisition 36. Which document triggers the revenue cycle? ➢ The customer purchase order 37. The customer open order file is used to ➢ Respond to customer queries 38. The billing department is not responsible for? ➢ Updating the inventory subsidiary records 39. Customers should be billed for backorders when ➢ the backordered goods are shipped 40. Usually specific authorization is required for all of the following except ➢ sales of goods at the list price 41. Which of following functions should be segregated? ➢ opening the mail and making the journal entry to record cash receipts 42. Which situation indicates a weak internal control structure? ➢ the mailroom clerk authorizes credit memos 43. The most effective internal control procedure to prevent or detect the creation of fictitious credit memoranda for sales returns is to ➢ require management approval for all credit memoranda 44. The accounts receivable clerk destroys all invoices for sales made to members of her family and does not record the sale in the accounts receivable subsidiary ledger. Which procedure will not detect this fraud? ➢ prepare monthly customer statements 45. Which department is least likely to be involved in the revenue cycle? ➢ accounts payable 46. Which document is included with a shipment sent to a customer? ➢ packing slip 47. Good internal controls in the revenue cycle should ensure all of the following except ➢ all sales are profitable 48. Which control does not help to ensure that accurate records are kept of customer accounts and inventory? ➢ authorize credit 49. Internal controls for handling sales returns and allowances do not include ➢ computing bad debt expense using the percentage of credit sales 50. The printer ran out of preprinted sales invoice forms and several sales invoices were not printed. The best internal control to detect this error is ➢ a batch total of sales invoices to be prepared compared to the actual number of sales invoices prepared 51. Which department prepares the bill of lading? ➢ Shipping 52. A remittance advice is ➢ is a turn-around document 53. A weekly reconciliation of cash receipts would include comparing ➢ the cash prelist with bank deposit slips 54. At which point is supervision most critical in the cash receipts system? ➢ mail room 55. An advantage of real-time processing of sales is ➢ current inventory information is available 56. Commercial accounting systems have fully integrated modules. The word "integrated" means that a. segregation of duties is not possible ➢ transfer of information among modules occurs automatically 57. The data processing method that can shorten the cash cycle is ➢ real-time file processing 58. Which of the following is not a risk exposure in a microcomputer accounting system? ➢ reliance on paper documentation is increased 59. Which journal is not used in the revenue cycle? ➢ purchases journal 60. Periodically, the general ledger department receives all of the following except ➢ total of all sales backorders 61. The credit department? ➢ authorizes the granting of credit to customers 62. Adjustments to accounts receivable for payments received from customers is based upon ➢ the remittance advice that accompanies payment 63. The revenue cycle utilizes all of the following files except ➢ cost data reference file 64. All of the following are advantages of real-time processing of sales ➢ The cash cycle is shortened ➢ Paper work is reduced ➢ Up-to-date information can provide a competitive advantage in the marketplace 65. A well-designed purchase order is an example of a ➢ preventive control 66. A physical inventory count is an example of a ➢ detective control 67. The bank reconciliation uncovered a transposition error in the books. This is an example of a ➢ detective control 68. Which of the following is not an element of the internal control environment? ➢ well-designed documents and records 69. Which of the following suggests a weakness in the internal control environment? ➢ performance evaluations are prepared every three years 70. When duties cannot be segregated, the most important internal control procedure is ➢ Supervision 71. An accounting system that maintains an adequate audit trail is implementing which internal control procedure? ➢ accounting records 72. The board of directors consists entirely of personal friends of the chief executive officer. This indicates a weakness in ➢ the control environment 73. The office manager forgot to record in the accounting records the daily bank deposit. Which control procedure would most likely prevent or detect this error? ➢ independent verification 74. The type of transaction most suitable for real-time processing is ➢ recording a sale on account 75. Which accounting application is least suited for batch processing? ➢ Payroll Principles of Internal Controls Establish Responsibilities ● Proper Internal control means that responsibility for a task is clearly established and assigned to one person. Maintain Adequate records ● Good record keeping is part of internal control and helps to protect assets and ensure that employees use prescribed procedures. Insure assets and bond key employees ● Good internal control means that assets are adequately insured against casualty and that employees are bonded. Separate record keeping from custody of assets ● A person who controls or has access to an asset must not keep that assets accounting records. Divide responsibility for related transactions ● Good internal control divides responsibility for a transaction or series of related transactions. Apply technological controls ● Technology improves effectiveness of control using cash register, time clocks, scanners. Perform regular and independent reviews ● Internal control needs to ensure that procedures are followed and reviewed from an impartial perspective.