Accounting Exam: Foreign Currency, Business Combinations

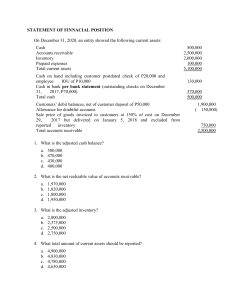

advertisement

4 CAMPUS / BRANCH (Please choose properly) * PUP Sta. Mesa PUP Sta. Maria, Bulacan PUP San Juan PUP Taguig PUP Maragondon, Cavite PUP Bataan PUP San Pedro, Laguna PUP Sta. Rosa, Laguna PUP Binan, Laguna PUP Alfonso, Cavite PUP Lopez, Quezon Province PUP Sto. Tomas, Batangas 5 Victory Corporation issued a promissory note denominated in foreign currency for the purchase made from a supplier in England on December 1, for a 60-day, 18% promissory note for 150,000 pounds, at a selling rate of 1FC to P74.50. On December 31, the selling spot rate is 1FC to P74.95. On January 30, the selling spot rate is 1FC to P75.65. On the settlement date, how much is the foreign exchange gain/loss? * (2 Points) P105,000 loss 6 The following are the acquisition related costs that is not considered as expenses in the period in which they are incurred, except * (1 Point) Listing Fees in issuing new shares Cost to issue debt securities Cost of Stock Certificates Audit Fee for SEC Registration 7 Hyperinflation is indicated by characteristics of the economic environment of a country, which of the following is NOT an indication that a particular economy is “hyperinflationary”? * (1 Point) Interest rates, wages and prices are linked to a price index. Sales and purchases on credit take place at prices that compensate for the expected loss of purchasing power during the credit period, even if the period is short. The general population prefers to keep its wealth in monetary assets or in a time bank deposit. The cumulative inflation rate over three years is approaching, or exceeds, 100%. 8 On January 01, 2021, Parent Corp. acquired 75% of the outstanding stock of Subsidiary Co. for P1,380,000 cash. The book value of Subsidiary Co.’s net assets was P1,200,000. Parent Corp. determined that the inventory and plant assets (remaining life of 5 years) of Subsidiary Co. were understated by P100,000 and P300,000, respectively. Subsidiary Co.’s net income for the year ended December 31, 2021 was P500,000. During the year 2021, Parent Corp. received P240,000 cash dividends from Subsidiary Co. The fair value of NCI was determined at P445,000. Loss on impairment of goodwill was P25,000. Net income of P Corp. under the cost method amounted to P1,000,000. P Corp. is using the fair value method in measuring NCI. How much is the Investment Balance on December 31, 2021 on the books of Parent Corp. under the equity method? * (2 Points) P1,380,000 P1,395,000 P1,375,000 P1,615,000 9 Sofia Inc., an SME, has completed the assessment of the fair value of the net assets of First Company to amount to P19,560,000. The consideration payable for the acquisition equals P19,000,000. Additional general transaction costs amount to P1,100,000. What must be recognized and recorded? * (1 Point) Sofia will book a gain of P560,000 through profit or loss and expense transaction costs. Sofia will book a gain P560,000 through OCI and expense transaction costs. Sofia will book a goodwill of P540,000. Sofia will book a negative goodwill of P560,000 as a liability and expense the transaction costs. 10 How much is the Non-Controlling Interest at December 31, 2021? * (2 Points) P840,280 P821,720 P805,625 P822,280 11 Juancho Company, a manufacturing company based in Laguna, Philippines, purchased raw materials from a foreign company denominated in foreign currency. Which of the following is correct? * (1 Point) If the foreign currency appreciates, Juancho will recognize foreign exchange loss. If the foreign currency appreciates, Juancho will recognize foreign exchange gain. If the foreign currency depreciates, Juancho will recognize foreign exchange loss. Any gain or loss will be deferred until the date of settlement. No gain nor loss will be recognized in the financial statement. 12 Which of the following statements is/are TRUE in reference to PFRS#10: Consolidated Financial Statements? i. An investor must be exposed, or have rights, to variable returns from its involvement with an investee to control the investee. Such returns must have the potential to vary as a result of the investee's performance and can be positive, negative, or both. ii. An investor that holds only protective rights cannot have power over an investee and so cannot control an investee. iii. Power arises from rights. Such rights can be complex (e.g. through voting rights) or be straight forward (e.g. embedded in contractual arrangements). iv. A parent must not only have power over an investee and exposure or rights to variable returns from its involvement with the investee, a parent must also have the ability to use its power over the investee to affect its returns from its involvement with the investee. * (1 Point) i, ii, iii, and iv i and iv i, ii, and iv i, ii, and iii 13 A business combination occurs when a company acquires an equity interest in another entity and has * (1 Point) At least 20% ownership in the entity. More than 50% ownership in the entity. 100% ownership in the entity. Control over the entity, irrespective of the percentage owned. 14 In 2020, P Company sold inventory costing P50,000 to S Company (90%-owned) for P100,000. By the end of the year, S sold 80% of the inventory. The elimination entries in 2021 would include: * (1 Point) Debit to Cost of Sales, P10,000 Credit to Inventory, P10,000. Debit to Retained Earnings, P10,000. Credit to Cost of Sales, P100,000. 15 The fair value of Subsidiary Company’s equipment is P153,000. Assuming Parent Company acquired 70% of the outstanding common stock of Subsidiary Company for P105,000 and Non-controlling interest is measured at fair value of P61,000. How much is the goodwill (gain on acquisition)? * (2 Points) P13,000 16 Two entities entered into a contractual arrangement to exercise joint control of a property, each taking a share of the rents received and bearing a share of the expenses. The entities are the registered joint owners of the property. The two entities have: * (1 Point) A jointly controlled operation The fair value model A jointly controlled asset A joint venture 17 The cumulative inflation rate is determined at 133.33% - hyperinflationary. How much is the CPI for the year ended December 31, 2022? * (2 Points) 150 180 210 140 18 Statement 1: A controlling interest in a company implies that the parent company has acquired all of the subsidiary’s shares of stock. Statement 2: When the fair value of acquiree’s inventory is higher than its book value on the date of acquisition, the elimination entry at the end of the period will have a decreasing effect in the reported profit of the parent. * (1 Point) Only statement 1 is true Both statements are incorrect Only statement 2 is true Both statements are correct 19 How much is the Consolidated Cost of Sales in 2021? * (2 Points) P3,745,833 P3,810,000 P4,812,500 P4,810,000 20 On January 1, 2021, Parent Company acquired 100% of Subsidiary Company for a consideration transferred of P85 million. On this date, the carrying amount of Subsidiary’s net assets was P75 million. During the acquisition, a provisional fair value of P95 million was attributed to the net assets. An additional valuation received on December 31, 2021 increased this provisional fair value to P100 million and on January 30, 2022 this fair value was finalized at P105 million. What amount should Parent Company present as goodwill in its statement of financial position on December 31, 2022, according to PFRS 3 – Business Combinations? * (2 Points) P110,000,000 21 Goodwill arising from business combination is * (1 Point) Amortized over 10 years or its useful life, whichever is shorter Never amortized Amortized over 10 years or its useful life, whichever is longer Charged to retained earnings after the acquisition is completed 22 How much is the Consolidated Inventory at December 31, 2021? * (2 Points) P587,500 P560,000 P600,000 P590,000 23 A corporation received a promissory note denominated in Singapore Dollar (SG$) for an export transaction made to a Singaporean customer. The following were the related transactions: On December 1, sold merchandise for SG$64,000, at a buying spot rate of SG$1 to PHP34.40. On December 31, the buying spot rate is SG$1 = PHP34.95. On January 30 (settlement date), the buying spot rate is SG$1 = PHP34.05. How much is the total receivable recorded in December 31 financial statement? * (2 Points) P2,236,800 24 In the year after an 85% owned subsidiary sells equipment to its parent company at a loss, the non-controlling interest in the net income is computed by multiplying the non-controlling interest percentage to the subsidiary’s net income after: * (1 Point) Adding the unrealized loss on sale of equipment Deducting the unrealized loss on sale of equipment Adding the loss on sale of equipment realized on the current year Deducting the loss on sale of equipment realized on the current year 25 A jointly controlled entity is: * (1 Point) An entity over which the investor has significant influence or joint control and that is not a subsidiary An entity over which the investor has significant influence An entity over which the investor has significant influence and that is neither a subsidiary nor an interest in a joint venture An entity over which the investor has joint control 26 On January 07, 2022, Flash Co., acquired 35% interest in Point Co., for P4,300,000. Flash already held a 20% interest which had been acquired for P1,600,000 which was valued at P1,800,000 at January 07, 2022. The fair value of the identifiable net assets of Point Co., was P8,400,000. How much is the goodwill to be recognized as a result of the business combination assuming that NCI is measured at fair value? * (2 Points) P1,550,000 P2,300,000 P1,750,000 P0 27 On August 1, 2019 Binibining Marikit Corp issued 100,000 P 35.50 par value shares for the entire net assets of Ganda, Inc. The market value of the issued shares on that date was P 36 per share. Binibining Marikit paid a fee of P 160,000 to the consultant who arranged this acquisition. Costs of registering and issuing the equity securities amounted to P 60,000, one-fifth of which amount were legal fees and the balance paid to SEC. Ganda’s net assets on August 1, had a book value of P 3,256,000, which is appraised to be 12% understated in terms of its fair value. The net increase (decrease) to Binibining Marikit Corp.’s accumulated profits arising from the above combination assuming Binibining Marikit Corp. is an SME. * (2 Points) P13,280 28 Minor Corporation (SME) reports net assets of P300,000 at book value. These assets have an estimated market value of P350,000. If Major Corporation buys 80 percent ownership of Minor for P275,000. Minor opted to use the most appropriate method in measuring NCI for the said acquisition. Goodwill will be reported in the consolidated balance sheet in the amount of: * (2 Points) P0 29 The resulting goodwill in the reverse acquisition assuming 100% of Big Company’s shares were exchanged for Small Company’s share is: * (2 Points) P0 30 Statement 1: A parent shall prepare consolidated financial statements using uniform accounting policies for new transactions and other events in similar circumstances. Statement 2: Consolidation of an investee shall begin from the date the investor obtains control of the investee and cease when the investor loses equity interests of the investee. * (1 Point) False, False True, True True, False False, True 31 On January 31, 2020, Peculiar Inc. issued 100,000 shares of its P100 par value ordinary shares for the net assets of Shipwrecked, Inc. The market value of Peculiar's ordinary shares on January 31 was P116 per share. Peculiar paid a fee of P80,000 to the consultant who arranged this acquisition. Costs of registering and issuing the equity securities amounted to P40,000. No goodwill was involved in the purchase. The business combination is between two (2) SMEs. The charged to business combination expenses is: * (2 Points) P120,000 None P80,000 P40,000 32 Statement 1: A joint operation is a joint arrangement whereby the parties that have joint control of the arrangement have rights over the assets, and obligations for the liabilities, relating to the arrangement. Statement 2: A joint venture is not a joint arrangement. * (1 Point) Only statement 1 is correct Only statement 2 is correct Both statements are correct. Both statements are incorrect. 33 Which of the following is CORRECT regarding the application of Section 15 of IFRS for SMEs? * (1 Point) Under the cost model, dividend is recognize in the profit or loss. Under the equity model, year-end fair value adjustment is recognize in the profit or loss. Under the fair value model, the proportionate share in the reported profit of the investee is recognize in the profit or loss. Transactions costs are capital, regardless of the model employed by the entity. 34 A joint venture is: * (1 Point) A contractual arrangement whereby two or more parties undertake an economic activity A contractual arrangement whereby two or more parties undertake an economic activity that is subject to joint control An entity whose equity is owned in equal shares (i.e. 20 percent) by five investors An entity whose equity is owned in equal shares (i.e. 25 percent) by four investors 35 How much is the Net Income Attributable to Parent? * (2 Points) P762,245 P834,245 P763,130 P778,900 36 The consolidated net income of the parent and subsidiary using the equity method compare to the cost method will be: * (1 Point) Lower Higher Either higher or lower, depending on the results of operations The same 37 On January 1, 2020, PEARLS Corporation acquired the identifiable net assets of START UP Company. On this date, the identifiable assets acquired and liabilities assumed have fair values of P6.4M and P3.6M, respectively. PEARLS incurred the following acquisition-related costs: legal fees – 40,000; due diligence costs – 400,000 and general admin costs – 80,000. As consideration, PEARLS issued 8,000 shares with par value and fair value per share of P400 and P500 respectively. Costs of registering and listing the shares amounted to P160,000. How much is the goodwill (gain on bargain purchase) on the business combination, assuming both companies qualified as SME? * (2 Points) P1,320,000 P1,720,000 P1,880,000 P1,200,000 38 In an acquisition where there is an exchange of assets for assets, how does the ownership structure of the acquirer change? * (1 Point) The acquirer stockholders become acquiree stockholders The acquirer and acquiree stockholders share ownership of the acquire There is no change in the acquirer ownership structure It is not possible to determine if there is a change in the acquire ownership structure 39 Statement I: Intercompany transfer of inventory at cost need not be eliminated in consolidation. Statement II. Downstream intercompany transfer of inventory to a 100%owned subsidiary need not be eliminated in consolidation. * (1 Point) Statement I is false; Statement II is true. Both statements are false. Statement I is true; Statement II is false. Both statements are true. 40 On December 31,2019, entity Alpha acquired 30 percent of the ordinary shares that carry voting rights of Entity Bravo for P100,000. In acquiring those shares, entity Alpha incurred transaction costs of P1,000. Entity Alpha has entered into a contractual arrangement with another party (entity Charlie) that owns 25 percent of the ordinary shares of entity Bravo, hereby entities Alpha and Charlie jointly control entity Bravo. Entity Alpha uses the cost model to account for its investment in jointly controlled entities. A published price quotation does not exist for entity Bravo. In January 2020,entity Bravo declared and paid a dividend of P20,000 out of profits earned in 2019. No further dividends were paid in 2020,2021 or 2022. At Dec 31,2019,2020 and 2021 in accordance with Section 27 Impairment of Assets , management assessed the fair values of its investment in entity Bravo as P102,000,P110,000 and P90,000 respectively. Costs to sell estimated at P4,000 throughout. The facts are the same in the immediately preceding question. However, in this scenario, a published price quotation exists for entity Bravo and entity Alpha uses the fair value model. Entity Alpha measures its investment in entity Bravo on Dec 31,2019,2020 and 2021 respectively at: * (2 Points) P98,000,P106,000,P86,000 P102,000,P110,000,P90,000 P98,000,P101,000,P86,000 P95,000,P95,000,P86,000 41 How much is the consolidated shareholders’ equity to be reported in the consolidated statement of financial position on December 31, 2021? * (2 Points) P10,651,800 P13,500,000 P11,781,000 P7,035,000 42 Lester and Jaime formed a joint venture to acquire and sell a special type of merchandise. Lester is to manage the venture and to furnish the capital. The participants are to share equally any gain or loss on the joint venture. On April 1, 2022, Jaime sent Lester P10,000 cash, which was all used to purchase merchandise. On April 27, one half of the merchandise was sold for P7,200 cash. Lester paid the cost of delivering merchandise to customers which amounted to P260. No further transactions occurred until the end of the month. The profit (loss) of the venture for the month of April: * (2 Points) P12,460 43 In the years subsequent to the year of sale a 90% owned subsidiary sells equipment to its parent company at a gain, the non-controlling interest in consolidated income is computed by multiplying the non-controlling interest percentage by the subsidiary’s reported income: * (1 Point) Plus intercompany gain considered realized in the current period. Plus the net amount of unrealized gain on the intercompany sale. Minus the net amount of unrealized gain on the intercompany sale. Minus intercompany gain considered realized in the current period. 44 When a company determine its functional currency: * (1 Point) It is permanent and cannot be change. The functional currency is not change unless there is a change in the underlying transactions, events, and conditions. It is changing every other year, depending on the functional currency the entity desires to use. It is changing every year, as a matter of company’s policy. 45 On December 31,2019, entity Alpha acquired 30 percent of the ordinary shares that carry voting rights of Entity Bravo for P100,000. In acquiring those shares, entity Alpha incurred transaction costs of P1,000. Entity Alpha has entered into a contractual arrangement with another party (entity Charlie) that owns 25 percent of the ordinary shares of entity Bravo, hereby entities Alpha and Charlie jointly control entity Bravo. Entity Alpha uses the cost model to account for its investment in jointly controlled entities. A published price quotation does not exist for entity Bravo. In January 2020,entity Bravo declared and paid a dividend of P20,000 out of profits earned in 2019. No further dividends were paid in 2020,2021 or 2022. At Dec 31,2019,2020 and 2021 in accordance with Section 27 Impairment of Assets , management assessed the fair values of its investment in entity Bravo as P102,000,P110,000 and P90,000 respectively. Costs to sell estimated at P4,000 throughout. Entity Alpha measures its investment in entity Bravo on Dec 31,2019,2020 and 2021, respectively at: * (2 Points) P102,000,P110,000,P90,000 P98,000,P106,000,P86,000 P98,000,P101,000,P86,000 P95,000,P95,000,P86,000 46 What is the cumulative inflation rate in 2023 to be used in determining if there is hyperinflation? * (2 Points) 120% 90.68% 190.68% 150% 47 What is the amount of expense to be recognized in the statement of comprehensive income for the year ended December 31, 2022? * (2 Points) P412,500 P307,400 P517,200 P257,200 48 Which of the following would be considered a vertical integration? * (1 Point) The merger of Walt Disney Company and Pixar The acquisition of Faceshift (a Star Wars motion-capture company) by Apple The acquisition of Instagram by Facebook (now Meta) The merger of Exxon and Mobil 49 How much is the Net Income Attributable to NCI? * (2 Points) P58,550 P62,500 P55,600 P60,000 50 On January 01, 2021, Parent Corp. acquired 75% of the outstanding stock of Subsidiary Co. for P1,380,000 cash. The book value of Subsidiary Co.’s net assets was P1,200,000. Parent Corp. determined that the inventory and plant assets (remaining life of 5 years) of Subsidiary Co. were understated by P100,000 and P300,000, respectively. Subsidiary Co.’s net income for the year ended December 31, 2021 was P500,000. During the year 2021, Parent Corp. received P240,000 cash dividends from Subsidiary Co. The fair value of NCI was determined at P445,000. Loss on impairment of goodwill was P25,000. Net income of P Corp. under the cost method amounted to P1,000,000. P Corp. is using the fair value method in measuring NCI. How much is the consolidated net income attributable to parent in 2021? * (2 Points) P995,000 51 What is the amount of goodwill to be recognized in the statement of financial position as of December 31, 2022? * (2 Points) P308,500 P295,450 P326,550 P314,550 52 Which of the following income items shall affect both Consolidated Net Income attributable to Parent and Non-Controlling Interest Net Income? * (1 Point) Gain on bargain purchase arising from business combination Unrealized/realized income/expense arising from transactions between two subsidiaries owned by the same parent. Unrealized/realized income/expense arising from downstream transactions. Impairment loss of goodwill from business combination initially measured using proportionate share of fair value of net asset acquired. 53 In reference to the downstream or upstream sale of depreciable assets, which of the following statements is correct? * (1 Point) Gains, but not losses, appear in the parent company accounts in the year of sale and must be eliminated by the parent in determining its investment income under the equity method of accounting. Upstream sales always result in unrealized gains or losses. The initial effect of unrealized gains and losses from the downstream sales is different from the sale of non-depreciable assets. Gains and losses appear in the parent company accounts in the year of sale and must be eliminated by the parent in determining its investment income under the equity method of accounting. 54 If the foreign operation reports in a currency of a non-hyperinflationary economy, income and expenses, for practical reason, shall be translated at: * (1 Point) Exchange rate on date of transaction Closing rate Average rate for the period Forward rate 55 Kind Company, an SME, issued 120,000 shares of P25 par value ordinary shares for all the outstanding stock of Clever Company in business combination consummated on July 1, 2020. Kind Company's ordinary shares were selling at P40 per share at the time of consummation of the combination. The book value of Clever’s net assets was P3.8M. Out of pocket costs of combination were as follows: legal fees for the business combination, P12,000; printing cost for stock certification, P9,400; finder's fee, P27,000 and CPA audit fees for business combination, P19,000. A contingent consideration which is probable and can be reasonably estimated amounted to P18,200. The total amount capitalized as cost of investment in Kind Company is: * (2 Points) P4,876,200 P4,818,200 P4,858,000 P4,800,000 56 How much is the Consolidated Net Income? * (2 Points) P716,500 P750,000 P725,000 P727,500 57 On February 28, 2022, P Corp. purchased 80% of S Co.’s P10 par ordinary shares for P986,000. On this date, the carrying amount of S’s net assets was P1,000,000. The fair values of S Co.’s identifiable assets and liabilities were the same as their carrying amounts except for inventory which is overvalued by P15,000 and plant assets (net), which were P120,000 in excess of the carrying amount. The estimated remaining life of the asset is 5 years. For the year ended December 31, 2022, S had net income of P354,000 and paid cash dividends to P Corp. of P112,000 (all coming from post-acquisition Retained Earnings). Loss on impairment of goodwill in 2022 amounted to P20,000. P Corp. uses the fair value method in measuring non-controlling interest. Revenues were earned evenly throughout the year Determine the non-controlling interest in net asset of subsidiary on December 31, 2022. * (2 Points) P272,500 58 Under PFRS for SMEs: * (1 Point) Both direct and indirect costs are to be expensed. Both direct and indirect costs are to be capitalized Direct costs are to be capitalized and indirect costs are to be expensed. Indirect costs are to be capitalized and direct costs are to be expensed 59 Ernest Company acquired 80% interest of Nikki Company in a business combination accounted as an acquisition. Ernest issued 10,000 shares of its ordinary shares at par (12 per share) and paid cash of P50,000. Ernest incurred the following cost in relation to the acquisition: finder’s fee – P5,000; share issue cost – P3,000; indirect business combination expenses – P2,000. Ernest Company always issue its shares of stocks at par. Which of the following statements is CORRECT? * (1 Point) P7,000 and P3,000 is chargeable to Ernest Company’s Expense and Share Premium, respectively P7,000 and P3,000 is chargeable to Nikki Company’s Expense and Share Premium, respectively P10,000 is chargeable to Ernest Company’s Expense P2,000 and P3,000 is chargeable to Ernest Company’s Expense and Share Premium, respectively 60 On the date of acquisition, the NCI to appear in the consolidated statement of financial position is * (2 Points) P730,000 61 How much is the consolidated retained earnings at December 31, 2022? * (2 Points) P589,950 62 If the entity is using the equity method to account for investment in subsidiary, the entry to recognize the proportionate share on the profit reported by the subsidiary will: * (1 Point) Decrease the carrying amount of investment Increase the carrying amount of investment Be recognized in other comprehensive income Not affect carrying amount of investment Ignored 63 Section ____ of the PFRS for SMEs provides the principles in accounting for Business Combinations and Goodwill for an SME. * (1 Point) Section 19 Sections 19 & 18 Section 18 Section 9 64 On January 01, 2021, Parent Corp. acquired 75% of the outstanding stock of Subsidiary Co. for P1,380,000 cash. The book value of Subsidiary Co.’s net assets was P1,200,000. Parent Corp. determined that the inventory and plant assets (remaining life of 5 years) of Subsidiary Co. were understated by P100,000 and P300,000, respectively. Subsidiary Co.’s net income for the year ended December 31, 2021 was P500,000. During the year 2021, Parent Corp. received P240,000 cash dividends from Subsidiary Co. The fair value of NCI was determined at P445,000. Loss on impairment of goodwill was P25,000. Net income of P Corp. under the cost method amounted to P1,000,000. P Corp. is using the fair value method in measuring NCI. How much is the Non-Controlling Interest in Net Assets of the subsidiary on December 31, 2021? * (2 Points) P450,000 P445,000 P405,000 P400,000 65 The accounting for reverse acquisition applied the principle of substance of the transaction rather than the form of transaction, accounting for acquisition is taken from the point of view of: * (1 Point) Legal Acquiree Legal Acquirer Accounting Acquiree Accounting Subsidiary 66 On January 1, 2023, Artemis Company purchased 80% of the outstanding share of Diana Corporation for P1,840,000. The book value of Diana’s net assets amounted to P2,000,000. Book values approximate the fair values at acquisition date. Artemis chose the fair value method in estimating the value of NCI. At acquisition date, NCI has a fair value of P440,000. On October 31, 2023, Artemis sold 10% of the share capital to several investors for P260,000. The fair value of the 10% share at that time is P240,000. How much is the gain to be reported in the consolidated statement of income for the year ended December 31, 2023 as a result of the sale of 10% ownership? * (2 Points) P0 67 An investee’s only business activity is to purchase receivables and service them on a day-to-day basis. Servicing involves collection and passing on of principal and interest payments. Upon default, the investee automatically puts the receivable to investor X as agreed separately in a put agreement with investor X. Is Inventor X required to consolidate Investee in its consolidated financial statements? * (1 Point) Yes but only if X owns 51% or more of voting stocks of investee. No because there is no link of power over the investee to the exposure/right to variable returns of investment. Yes because X controls the investee’s relevant activity that is managing the receivables upon default which significantly affects the investee’s returns. No because there is no statement as regards to majority ownership of stocks. 68 How much is the Goodwill to be presented in the consolidated financial statements at December 31, 2021? * (2 Points) P160,000 P195,000 P135,000 P137,500 69 How much is the Consolidated Gross Profit in 2021? * (2 Points) P4,555,800 P3,444,200 P4,000,000 P2,051,800 70 Under Business Combinations and Goodwill Section of the PFRS for SMEs, the acquirer, after initial recognition, shall follow the principles in Intangible Assets Section of the PFRS for SMEs for amortization of goodwill. If an entity is unable to make a reliable estimate of the useful life of goodwill, the life shall be presumed to be how many years? * (1 Point) 10 years not amortized but tested for impairment at least 1 year 5 years 20 years Submit This content is created by the owner of the form. The data you submit will be sent to the form owner. Microsoft is not responsible for the privacy or security practices of its customers, including those of this form owner. Never give out your password. Powered by Microsoft Forms | Privacy and cookies | Terms of use