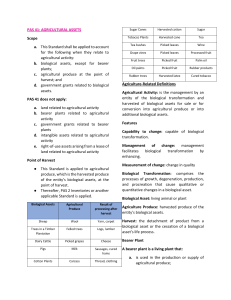

UNIVERSITY OF RIZAL SYSTEM BINANGONAN CAMPUS COLLEGE OF ACCOUNTANCY UPDATES IN FINANCIAL REPORTING STANDARDS ACCTG ELEC 3 BIOLOGICAL ASSETS JOSHUA TITO L. TANGCA Instructor Multiple Choice: Identify the choice that best completes the statement or answers the question. 1. 1. Biological assets are measured at a. Cost b. Lower of cost or net realizable value c. Net realizable value d. Fair value less cost to sell 2. Agricultural produce is measured at a. Fair value b. Fair value less costs to sell at the point of harvest c. Net realizable d. Net realizable value less normal profit margin 3. Agricultural activity includes all of the following, except a. Raising livestock b. Perennial cropping c. Aquaculture d. Ocean fishing 4. Biological transformation results from asset changes through all of the following, except a. Growth b. Degeneration c. Procreation d. Production of agricultural produce 5. When the fair value of the biological asset cannot be determined reliably, the biological asset shall be measured at a. Cost b. Cost less accumulated depreciation c. Cost less accumulated depreciation and accumulated impairment losses d. Net realizable value 6. Which of the following costs should not be included in costs to sell? a. Commissions to brokers and dealers b. Levies by regulatory agencies c. Transfer taxes and duties d. Transport costs 7. Which of the following is unlikely to be used in fair value measurement? a. Quoted price in a market b. The most recent market transaction price c. The present value of the expected net cash flows from the asset d. External independent valuation 8. Land that is related to agricultural activity is measured a. At fair value. b. In accordance with PAS 16 or PAS 40. c. At fair value in combination with the biological asset that is being grown on the land. d. At the resale value separate from the biological asset that is being grown on the land. 9. An unconditional government grant related to a biological asset that has been measured at fair value less cost to sell shall be recognized as a. Income when the grant becomes receivable. b. A deferred credit when the grant becomes receivable. c. Income when the grant application has been submitted. d. A deferred credit when the grant has been approved. 10. All of the following criteria must be satisfied before a biological asset can be recognized in an entity’s financial statements, except a. The entity controls the asset as a result of past event. b. It is probable that future economic benefits relating to the asset will flow to the entity. c. An active market for the asset exists. d. The fair value or cost of the asset can be measured reliably. BIOLOGICAL ASSETS 1