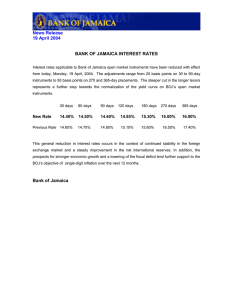

Module name: Top up Contemporary of issues in Banking and Finance ID student: 20055735 Word count: 1093 Inflation influences the global economy, so the market makers in the world decide and implement the monetary policy paradigm to tackle it. Each central banks have a different method to control it. According to the Bank of Japan (2013), the foundation of a nation’s economic activity is price stability, so it is significant for Japan to overcome deflation early and sustain economic growth. In order to achieve maintainable price stability, the central bank of Japan conducts its monetary policy framework with a target of 2% for the annual change in the consumer price index. In order to under the price stability target of 2%, BoJ introduced a comprehensive unconventional monetary policy tool to achieve price stability: “Quantitative and qualitative monetary easing (QQE)” based on Yield Curve Control and Inflation-overshooting Commitment. “Price stability” means a state where households and firms decide to consume and invest without variations in the general price stage; therefore, BoJ set a goal of 1%. However, a year-onyear change in CPI made Bank replace “the goal of 1%” with “a target at 2%” in 2013. This target was based on two perspectives. Firstly, the target was set to be consistent with the inflation rate in Japan’s economy because it was a sustainable basis for improving competitiveness and the growth of Japan’s economy. By examining the economic activity and price over the next two years, the market maker in Japan supposed that the price stability target of 2% would significantly increase the national economy. Secondly, the price stability target of 2% is an essential resilience in the conduct of monetary policy in Japan after examining various risk factors in the longer term, typically the impact of financial imbalances. Figure 1 CPI Inflation from 1990 to 2018 Specifically, according to figure 1, the CPI inflation between 1990 and 2010 witnessed a significant deflation, being 4 percent to approximately negative 3 percent. According to the research of UEDA (2011), Japan’s economy has been affected remarkably by a “liquidity trap” for 20 years, beginning in 1990. From 1999 to 2007, BoJ did a zero-interest-rate policy (ZIRP) in the short term to dispel deflationary concerns, with inflation being around zero. Also, research showed that BoJ had to use bank reserve as the operating policy target when the IT bubble collapsed in 2001 to increase the price. However, the financial crisis happened during 2008-2009, and a sharp increase in CPI inflation in 2015 made BoJ change its monetary policy. When deflation affected the whole economy of Japan led to the central bank switched from a target of price stability at 2% in 2013; the central bank decided to use the unconventional tool QQE with a new framework for strengthening quantitative easing. Figure 2 Transmission Mechanism of QQE Envisioned QQE was first introduced in April 2013, aiming to expand the monetary policy base to target massive government bond purchasing. Firstly, QQE was the update of QE, and QQE monetary policy is needed to boost demand to stabilize prices with a positive output gap in the medium term. Figure 2 shows the transmission mechanism of QQE, which decreases the nominal interest rate by purchasing Japanese Government Bonds (JGBs) to raise inflation expectations (at 2%) through monetary easing. So, the real interest rate decreases because of economic activity and price development improving. It also is no longer experiencing deflation in Japan's economy because of an improvement in the output gap with increasing inflation expectations. Additionally, QQE has two components: (1) “yield curve control” controls short and longterm interest rates, (2) “Inflation-overshooting Commitment” expands the monetary base in term of increasing over 2 percent of CPI inflation rate year-on-year. First, during short-term, current account balance of financial institution holds negative interest rate of minus 0.1% to the PolicyRate Balances at central bank in 2021 (BoJ, 2021). As a result, it decreases in short-term interest rate and reduce selling JGBs which hold by financial institution because of increasing current account. The figure 3 demonstrated that JGB yield curve was low, being under 0.5 percent when central bank decided to introduce QQE with a negative interest rate. Conversely, in long term BoJ will purchases JGBs, especially, 10-year JGB yields continues holding around zero percent to supply funding. Also, the negative interest rate policy dropped 0.2-0.3 percent long-term interest rate. QQE with negative interest rate has contributed to the flattening of the yield curve. Typically, the number of JGBs acquiring, the central bank does transaction buying more or less in line with the current pace, being about 80 trillion yen to achieve the long-term interest rate target. To let smoothy, BoJ purchases absolutely all JGBs with fixed-rate purchase by them. Figure 3 Change in the JGB yield curve The second component is the “inflation-overshooting committee”. BoJ will continue with “QQE with Yield Curve Control” to a stable price at 2%. When the market maker expands the monetary base policy, Bank could control CPI inflation at 2%. Meanwhile, during the short run, the interest rate in the monetary policy base might oscillate to discipline the yield curve in financial markets. Achieving the Bank of Japan’s “price stability at 2% target by using QQE” has been proven by Anand, Hong and Hul (2019) based on Quarterly Projection Model (QPM1). The research shows that the unconventional tool used by BoJ is good at controlling inflation, but BoJ should have more reserves for a bad situation. 14000000 12000000 10000000 8000000 6000000 4000000 2000000 2010/01 2010/06 2010/11 2011/04 2011/09 2012/02 2012/07 2012/12 2013/05 2013/10 2014/03 2014/08 2015/01 2015/06 2015/11 2016/04 2016/09 2017/02 2017/07 2017/12 2018/05 2018/10 2019/03 2019/08 2020/01 2020/06 2020/11 2021/04 2021/09 2022/02 2022/07 0 Japanese Government Securities (Assets) Total (Assets, or Liabilities and Net Assets) Figure 4 the Securities and Total Asset/Liabilities Doing “QQE with Yield Curve Control” effect significantly on Assets and Liabilities in the balance sheet, especially Securities of BoJ and Non-performing Loans. It witnessed an increase significantly in Securities from 725,539 to 5,614,526 thousand Yen from 01/2010 to 07/2022. Also, a similar trend was Assets/Liabilities, being 1,132,336 to 7,386,915 thousand Yen. Moreover, the research of Ryuzo, Okimoto and Rieti (2017) showed that the QQE regime affected the macroeconomic, for example, stock prices, exchange rates, interest rate channels and asset prices. A declining interest rate forces higher asset prices, a credit advance, increasing securities, 1 QPM for Japan is a semi-structural gap model, which is based on the New-Keynesian paradigm and has characteristics explicitly derived from microeconomic foundations and a decrease in currency because of the more current account. Furthermore, the challenge of BoJ is a decline in bank loans to maintain productivity and profitability in the corporate sector. QQE affects the expansionary monetary base generating more. In conclusion, bank of Japan aimed price stabilities target at 2% with unconventional QQE tool to control inflation. However, this tool has effect on the macroeconomic creating challenges for Bank of Japan. Therefore, BoJ has always adapted. References: 1. Anand, R., Hong, G.H. and Hul, Y. (2019). Achieving the Bank of Japan’s Inflation Target. SSRN Electronic Journal. doi:10.2139/ssrn.3496707. 2. Bank of Japan (2013a). Cabinet Office Ministry of Finance Bank of Japan Joint Statement of the Government and the Bank of Japan on Overcoming Deflation and Achieving Sustainable Economic Growth. [online] Available at: https://www.boj.or.jp/en/announcements/release_2013/k130122c.pdf. 3. Bank of Japan (2013b). Introduction of the ‘Quantitative and Qualitative Monetary Easing’ (Announced at 1:40 p.m.). [online] Available at: https://www.boj.or.jp/en/announcements/release_2013/k130404a.pdf. 4. Bank of Japan (2013c). The ‘Price Stability Target’ under the Framework for the Conduct of Monetary Policy. [online] Available at: https://www.boj.or.jp/en/announcements/release_2013/k130122b.pdf [Accessed 14 Dec. 2022]. 5. Bank of Japan (2014). Expansion of the Quantitative and Qualitative Monetary Easing (Announced at 1:44 p.m.). [online] Available at: https://www.boj.or.jp/en/announcements/release_2014/k141031a.pdf. 6. Bank of Japan (2016a). Bank of Japan New Framework for Strengthening Monetary Easing: ‘Quantitative and Qualitative Monetary Easing with Yield Curve Control’. [online] Available at: https://www.boj.or.jp/en/announcements/release_2016/k160921a.pdf [Accessed 14 Dec. 2022]. 7. Bank of Japan (2016b). Comprehensive Assessment: Developments in Economic Activity and Prices as well as Policy Effects since the Introduction of Quantitative and Qualitative Monetary Easing (QQE). [online] Available at: https://www.boj.or.jp/en/announcements/release_2016/rel160930d.pdf [Accessed 14 Dec. 2022]. 8. Bank of Japan (2016c). Introduction of ‘Quantitative and Qualitative Monetary Easing with a Negative Interest Rate’. [online] Available at: https://www.boj.or.jp/en/announcements/release_2016/k160129a.pdf. 9. Bank of Japan (2018). Strengthening the Framework for Continuous Powerful Monetary Easing. [online] Available at: https://www.boj.or.jp/en/announcements/release_2018/k180731a.pdf [Accessed 14 Dec. 2022]. 10. Bank of Japan (2021). Bank of Japan Further Effective and Sustainable Monetary Easing 1. Assessment for Further Effective and Sustainable Monetary Easing At the Monetary Policy Meeting held today, the Bank of Japan conducted an assessment for. [online] Available at: https://www.boj.or.jp/en/announcements/release_2021/k210319a.pdf [Accessed 14 Dec. 2022]. 11. Iwata, K. and Takenaka, S. (2014). Central bank balance sheet expansion: Japan’s experience. [online] Available at: https://www.bis.org/publ/bppdf/bispap66g.pdf. 12. Ryuzo, M., Okimoto, T. and Rieti (2017). The Macroeconomic Effects of Japan’s Unconventional Monetary Policies. RIETI Discussion Paper Series. 13. UEDA, K. (2011). THE EFFECTIVENESS OF NON-TRADITIONAL MONETARY POLICY MEASURES: THE CASE OF THE BANK OF JAPAN*. Japanese Economic Review, 63(1), pp.1–22. doi:10.1111/j.1468-5876.2011.00547.x.