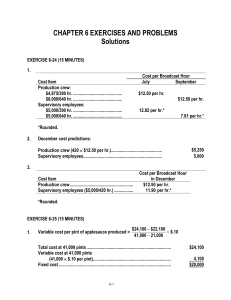

CIA 1004- SEMINAR 4 SOLUTIONS TO QUESTIONS ON COSTS ESTIMATES 6-3 a. Hotel: Percentage of rooms occupied or the number of occupancy-days, where an occupancy-day is defined as one room occupied for one day. b. Hospital: Patient-days, where a patient-day is defined as a one-day stay by one patient. c. Computer manufacturer: Number of computers manufactured, throughput, engineering specifications, engineering change orders, or number of parts in the finished product. d. Computer sales store: Sales revenue. e. Computer repair service: Repair calls or hours of repair service. f. Public accounting firm: Hours of auditing service provided by each classification of personnel (partner, manager, supervisor, senior accountant, and staff accountant). 6-5 As the level of activity (or cost driver) increases, total fixed cost remains constant. However, the fixed cost per unit of activity declines as activity increases. 6-6 A manufacturer's cost of supervising production might be a step-fixed cost, because one supervisor is needed for each shift. Each shift can accommodate a certain range of production activity; when activity exceeds that range, a new shift must be added. When the new shift is added, a new production supervisor must be employed. This new position results in a jump in the step-fixed cost to a higher level. 6-7 As the level of activity (or cost driver) increases, total variable cost increases proportionately and the variable cost per unit remains constant. 6-13 An outlier is a data point that falls far away from the other points in the scatter diagram and is not representative of the data. One possible cause of an outlier is simply a mistake in recording the data. Another cause of an outlier is a random event that occurred, which caused the cost during a particular period to be unusually high or low. For example, a power outage may have resulted in unusually high costs of idle time for a particular time period. Outliers should be eliminated from a data set upon which cost estimates are based. 6-16 The chief drawback of the high-low method of cost estimation is that it uses only two data points. The rest of the data are ignored by the method. An outlier can cause a significant problem when the high-low method is used if one of the two data points happens to be an outlier. In other words, if the high activity level happens to be associated with a cost that is not representative of the data, the resulting cost line may not be representative of the cost behavior pattern. 1 EXERCISE 6-22 (15 MINUTES) 1. Cost per Broadcast Hour August October Cost Item Production crew: $5,330/410 hr. ........................................... $8,840/680 hr. ........................................... Supervisory employees: $6,000/410 hr. ........................................... $6,000/680 hr. ........................................... $13.00 per hr. $13.00 per hr. $14.63 per hr.* $ 8.82 per hr.* *Rounded. 2. December cost predictions: Production crew (440 $13.00 per hr.) ............................................. Supervisory employees ..................................................................... $5,720 $6,000 3. Cost Item Production crew ........................................................ Supervisory employees ($6,000/440 hr.).................. Cost per Broadcast Hour in December $13.00 per hr. 13.64 per hr.* *Rounded. EXERCISE 6-29 (15 MINUTES) 1. Variable cost per pint of applesauce produced = $95,200 - $55,200 = $.50 140,000 - 60,000 Total cost at 140,000 pints ......................................................................... Variable cost at 140,000 pints (140,000 $.50 per pint) ................................................................... Fixed cost.................................................................................................... $95,200 70,000 $25,200 Cost equation: Total energy cost = $25,200 + $.50X, where X denotes pints of applesauce produced 2. Cost prediction when 95,000 pints of applesauce are produced Energy cost = $25,200 + ($.50)(95,000) = $72,700 2 PROBLEM 6-36 (15 MINUTES) An appropriate activity measure for the school would be hours of instruction. The costs are classified as follows: 1. Variable 6. Variable 2. Semivariable (or mixed)* 7. Fixed 3. Fixed 8. Fixed 4. Fixed 9. Semivariable (or mixed) 5. Fixed *The fixed-cost component is the salary of the school's repair technician. As activity increases, one would expect more repairs beyond the technician's capability. This increase in repairs would result in a variable-cost component equal to the dealer's repair charges. PROBLEM 6-43 (35 MINUTES) 1. The regression equation's intercept on the vertical axis is $250. It represents the portion of indirect material cost that does not vary with machine hours when operating within the relevant range. The slope of the regression line is $8 per machine hour. For every machine hour, $8 of indirect material costs are expected to be incurred. 2. Estimated cost of indirect material at 900 machine hours of activity: S = $250 + ($8 900) = $7,450 3. Several questions should be asked: (a) Do the observations contain any outliers, or are they all representative of normal operations? (b) Are there any mismatched time periods in the data? Are all of the indirect material cost observations matched properly with the machine hour observations? (c) Are there any allocated costs included in the indirect material cost data? (d) Are the cost data affected by inflation? 4. Beginning inventory ............................................................ April $1,500 August $1,200 3 + Purchases ......................................................................... – Ending inventory .............................................................. Indirect material used ......................................................... 5. 7,500 (1,600) $7,400 8,300 (3,500) $6,000 High-low method: Variable cost per machine hour = difference in cost levels difference in activity levels = $7,400 - $6,000 $1,400 = = $2.00 per machine hour 2,000 - 1,300 700 Fixed cost per month: Total cost at 2,000 hours .............................................................................. Variable cost at 2,000 hours ($2.00 2,000) ......................................................................................... Fixed cost....................................................................................................... $7,400 4,000 $3,400 Equation form: Indirect material cost = $3,400 + ($2.00 machine hours) 6. The regression estimate should be recommended because it uses all of the data, not just two pairs of observations when developing the cost equation. 4 Syarikat Novati 1. Maintenance cost at the 90,000 machine-hour level of activity can be isolated as follows: Total factory overhead cost ........... Deduct: Utilities cost @ $0.80 per MH*.... Supervisory salaries ................... Maintenance cost ......................... Level of Activity 60,000 MHs 90,000 MHs $174,000 $246,000 48,000 21,000 $105,000 72,000 21,000 $153,000 *$48,000 ÷ 60,000 MHs = $0.80 per MH 2. High-low analysis of maintenance cost: High activity level ..................... Low activity level ...................... Change .................................... Machine- Maintenance Hours Cost 90,000 60,000 30,000 $153,000 105,000 $ 48,000 Variable rate: Change in cost $48,000 = =$1.60 per MH. Change in activity 30,000 MHs Total fixed cost: Total maintenance cost at the high activity level .... $153,000 Less variable cost element (90,000 MHs × $1.60 per MH) ........................... 144,000 Fixed cost element .............................................. $ 9,000 Therefore, the cost formula for maintenance is: $9,000 per month plus $1.60 per machine-hour or Y = $9,000 + $1.60X. 5 3. Maintenance cost ........... Utilities cost ................... Supervisory salaries cost. Totals ............................ Variable Cost per Machine-Hour $1.60 0.80 $2.40 Fixed Cost $ 9,000 21,000 $30,000 Thus, the cost formula would be: Y = $30,000 + $2.40X. 4. Total overhead cost at an activity level of 75,000 machine-hours: Fixed costs .................................................. Variable costs: 75,000 MHs × $2.40 per MH .. Total overhead costs .................................... $ 30,000 180,000 $210,000 6