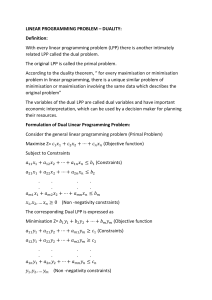

Course name: Quantitative Analysis for Management Decisions Course code: MBA 641 Credit Hour : 3 hrs Program: MBA This Lecture note is prepared by Moges Adisu (Ph.D in Management Studies) November 2015 E.C Chapter-2: Some Advanced Topics in LPP 2.1 Degeneracy and cycling in LPP 2.2 Primal and dual LPP 2.1 Degeneracy and cycling in LPP Definitions: • Basic Feasible Solution: A solution which satisfies all the constraints and non-negativity restrictions of an LPP is called a . If again the feasible solution is basic, then it is called a basic feasible solution (BFS). • A LP is degenerate if in a basic feasible solution, one of the basic variables takes on a zero value. • Degeneracy: a basic feasible solution (bfs) is called DEGENERATE iff at least one of the basic variables is 0. • A basic feasible solution is called degenerate if one of its RHS coefficients (excluding the objective value) is 0. This bfs is degenerate. So, In degeneracy, one of the RHS values is 0. • Degeneracy is a problem in practice, because it makes the simplex algorithm slower. Degeneracy ... • Degeneracy exists/occurs in two cases: When for one incoming variable there are two outgoing variables. This happens when there is tie in minimum positive ratios. That is, Another form of degeneracy is quantity value of a basic variable becomes zero. That is, when one or more of basic variables has ZERO value. Quantity value for a Basic variable is equal to zero in the simplex table. Degeneracy . . . • Basic Solution (BS): We consider the following system of equations: 2X1+ X2 –X3 = 2 3X1 + 2X2 +X3 = 3 And find the set of basic solutions by setting n-m variables equal to zero and then solve for the resulting equations. Since n=3 and m=2 and n-m =1 therefore,we set one variable at a time equal to zero. First setting x1=0, we have X2–X3=2 2X2+X3=3 • Solving the above equations, yield X2=5/3 and X3 =2/3 • Thus, we have X1=0, X2=5/3 and X3 =2/3 ------------------------(I) Degeneracy . . . • Similarly, setting X2=0, we get X1=1 and X3 =0 -----------------------(II) and setting, X3=0, we get, X1=1 and X2 =0 ----------------------------------------------------(III) and variables for which we solve the remaining system of equations are called basic variables. They will be equal to m in number. • In solution (I), variable X1is a non basic variable and X2andX3 are basic variables. • Degenerate Solution: If at least one of the basic variables is/are equal to zero, then, we call the solution as a degenerate solution. Normally, we do not prefer degenerate solution. In the above example, we have solutions (II) and (III) as Degenerate solutions. Cont’d ... • Non-Degenerate Solution: If none of the basic variables is zero, then we call the solution as a Non-degenerate solution. . In the above example, we have solution (I) as Non-Degenerate solution. Cycling • Cycling: If a sequence of pivots starting from some basic feasible solution ends up at the exact same basic feasible solution, then we refer to this as “cycling.” If the simplex method cycles, it can cycle forever. • Cycling occurs when a variable goes out of solution and then reentering. So, it forms a cycle by going out and re-entering. Or vice versa, i.e. entering the solution and going out in next tables. • In principle, cycling can occur if there is degeneracy. 2.2 Primal and dual LPP Duality: • The term ‘dual’ in a general sense implies two or double. • Every linear programming problem can have two forms. The original formulation of a problem is referred to as its Primal form. The other form is referred to as its dual LP problem or in short dual form. That is, every LPP has another LPP associated with it, which is called its dual. So, the given LPP is called the primal. Cont'd • The following rules which guide the formulation of the dual problem will give you the summary of the general relationship between primal and dual LP problems: a) If the primal’s objective is to minimize, the dual’s will be to maximize; and the vice versa; b) the coefficient’s of the primal’s objective function become the RHS values for the dual’s constraints; c) the primal’s RHS values become the coefficients of the dual’s objective function; d) the coefficients of the first “row” of the primal’s constraints become the coefficients of the first “column” of the dual’s constraint …..; e) the ≤ constraints become ≥ and the vice versa. When the primal problem is a maximization problem with all ≤ constraints, the dual is a minimization problem with all ≥ constraints. Cont'd • The dual of the dual is primal. • In the context of LP, duality implies that each LP problem can be analyzed in two different ways, but having equivalent solution. • the optimal solutions for the primal and the dual are equivalent. That is, whether we follow the dual or primal system, the optimal solution will remain equal. • if the primal has optimal solution, the dual will have optimal solution. • if the primal has no optimal solution, the dual will not have optimal solution. Cont'd • Primal-dual relationship Primal objective is minimization ≥ type constraints # of columns # of rows # of decision variables # of constraints coefficients of objective function RHS values Dual objective is maximization ≤ type constraints # of rows # of columns # of constraints # of decision variables RHS values coefficient of objective function Cont'd • Example 1: write the duals to the ffing problems Max. Z = 5X1 + 6X2 Stc 2X1 + 3X2 ≤ 3000 5X1 + 7X2 ≤ 1000 X1 + X2 ≤ 5000 and X1, X2 ≥ 0 Solution Let Y1, Y2, Y3 are dual variables Cont'd Dual variables X1 X2 Constraints Y1 2 3 ≤3000 Y2 5 7 ≤1000 Y3 1 1 ≤5000 Max. Z 5 6 Cont'd • By referring to the above table, dual can be constructed as: Min. Z = 3000Y1 + 1000Y2 + 5000Y3 Stc 2Y1 + 5Y2 + Y3 ≥ 5 3Y1 + 7Y2 + Y3 ≥ 6 And Y1, Y2, Y3 ≥ 0 Therefore, the RHS values of primal become the coefficients of objective function in the dual. the 1st column in the primal.......the 1st row in the dual. the 2nd column in the primal......the 2nd row in the dual. coefficients of objective function in the primal ......RHS values in the dual Cont'd • Example 2: Consider this primal problem Minimize Z = 40x1 + 44x2 + 48x3 Subject to: 1x1 + 2x2 + 3x3 ≥ 20 4x1 + 4x2 + 4x3 ≥30 And x1, x2, x3 ≥ 0 • The dual of this problem is: Maximise Z = 20y1 + 30y2 Subject to: 1y1 + 4y2 ≤ 40 2y1 + 4y2 ≤ 44 3y1 + 4y2 ≤ 48 And y1, y2 ≥ 0 Cont'd • Formulating the Dual when the Primal has Mixed Constraints: • In order to transform a primal problem into its dual, it is easier if all constraints in a maximization problem are of the ≤ variety, and in a minimization problem, every constraint is of the ≥ variety. • To change the direction of a constraint, multiply both sides of the constraints by -1. For example, -1(2x1 + 3x2≥ 18) is -2x1-3x2≤ -18 • If a constraint is an equality, it must be replaced with two constraints, one with a ≤ sign and the other with a ≥ sign. For instance, 4x1 + 5x2 = 20 will be replaced by 4x1 + 5x2≤ 20 4x1 + 5x2 ≥ 20 , depending on whether the primal is maximization or a minimization problem. Cont'd • Example 3: Formulate the dual of this LP model. Maximize z = Subject to: C1 C2 C3 50X1+ 80X2 3X1+ 5X2≤ 45 4X1+ 2X2 ≥16 6X1+6X2= 30 X1 , X 2 ≥ 0 Solution: Since the problem is a max problem, put all the constraints in to the ≤ form. Subsequently, C2 and C3 will be first adjusted in to ≤ constraints. Cont'd C2 will be multiplied by -1: -1(4X1+ 2X2 ≥16) becomes -4X1- 2X2≤ -16 C3 is equality, and must be restated as two separate constraints. Thus, it becomes: 6X1+6X2≤ 30 and 6X1+6X2 ≥30. Then the second of these must be multiplied by -1. -1(6X1+6X2 ≥30) becomes -6X1-6X2≤ -30 After making the above adjustments, rewrite the LP model again. Cont'd Maximize z = Subject to: C1 C2 C3 C4 50X1+ 80X2 3X1+ 5X2≤ 45 -4X1- 2X2≤ -16 6X1+6X2≤ 30 -6X1-6X2≤ -30 X1 , X 2 ≥ 0 The dual of the above problem will be: Minimize Z = 45y1 - 16y2 + 30y3 – 30y4 Subject to C1 3y1 -4y2 + 6y3 – 6y4 ≥ 50 C2 5y1 - 2y2 + 6y3 – 6y4 ≥ 80 y1, y2, y3, y4 ≥ 0 Questions & Suggestions?