Internal Controls Worksheet

advertisement

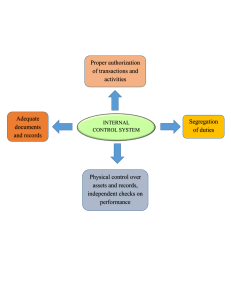

Rolling Hills Ltd. has the following internal controls over cash payments. Identify the control activity that is applicable to each procedure. 1 2 3 4 5 6 Company cheques are prenumbered. The bank statement is reconciled monthly by the assistant controller. Blank cheques are stored in a safe in the controller’s office. Both the controller and the assistant controller are required to sign cheques or authorize electronic payments. Cheque signers are not allowed to record cash payments. All payments are made by cheque or electronic transfer. Documentation Review and Reconciliation Physical Controls Assignment of Responsibility Segregation of Duties Physical Controls Tene Ltd. has the following internal controls over cash receipts. Identify the control activity that is applicable to each procedure. 1 2 3 4 5 (a) (b) (c) (d) (e) All over-the-counter receipts are recorded on cash registers. Daily cash counts are performed by the accounting supervisor. The duties of receiving cash, recording cash, and maintaining custody of cash are assigned to different individuals. Only cashiers may operate cash registers. All cash is deposited intact in the bank account every day. All transactions should include original, detailed receipts. Undeposited cash should be stored in the company safe. Surprise cash counts are performed by internal audit. Responsibility for related activities should be assigned to specific employees. Cheque signers are not allowed to record cash transactions. Documentation and Physical Controls Review and Reconciliation Segregation of duties Assignment of Responsibility Physical Controls Documentation Physical Controls Review and Reconciliation Assignment of Responsibility Segregation of Duties