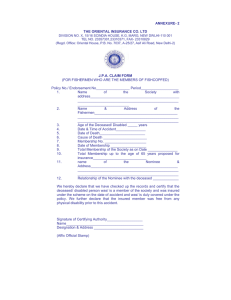

Succession Handbook: Managing Deceased's Financial Assets

advertisement