Decentralization & Performance Evaluation: Responsibility Accounting

advertisement

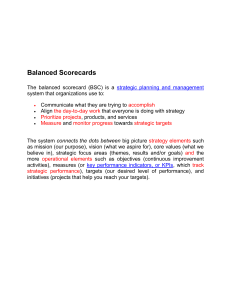

DECENTRALIZATION AND PERFORMANCE EVALUATION RESPONSIBILITY ACCOUNTING RESPONSIBILITY ACCOUNTING – a system of accounting wherein costs and revenues are accumulated and reported by levels of responsibility or by responsibility centers within the organization. Responsibility center (also called accountability center) – a clearly identified part or segment of an organization that is accountable for a specified function or set of activities. any part of the organization that a particular manager is responsible for – TYPES OF RESPONSIBILITY CENTERS: a. b. c. d. CostCenter (or expense center) – a segment of an organization in which managers are held responsible for the costs or expenses incurred in the segment. RevenueCenter– where management is responsible primarily for revenues. ProfitCenter– a segment of the organization in which the manager is held responsible for both revenues and costs. InvestmentCenter– a segment of the organization where the manager controls revenues, costs, and investments. The center’s performance is measured in terms of the use of the assets as well as the revenues earned and the costs incurred. The PERFORMANCE REPORT, which is often considered as the end-product of the responsibility accounting, shows and compares actual results with the intended (budgets or standards) results of a responsibility center, thereby highlighting material deviations that need corrective actions. The contents would normally depend on type of responsibility center presenting the performance report: RESPONSIBILITY CENTER KEY PERFORMANCE MEASURES Cost Center Variance Analysis: Actual vs. Budgeted/Standard Costs Revenue Center Variance Analysis: Actual vs. Budgeted/Target Sales Profit Center Variance Analysis: Actual vs. Budgeted/Target Profit Segmented Income Statement Investment Center Variance analysis: Actual vs. Budgeted/Target Profit Segmented Income Statement ROI, Residual Income, EVA CLASSIFICATIONS OF COSTS IN RESPONSIBILITY ACCOUNTING 1. 2. 3. By responsibility center By cost type, as to controllability By specific cost items or cost elements within each classification in (1) and (2). RESPONSIBILITY vs. ACCOUNTABILITY Responsibilityhas two facets, (1) the obligation to secure results, and (2) the obligation to report back the results achieved to higher authority. Accountabilitydenotes the obligation to report results achieved to higher authority. THE CONCEPT OF DECENTRALIZATION Decentralization refers to the separation or division of the organization into more manageable units wherein each unit is managed by an individual who is given decision authority and held accountable for his decisions. Goal congruence – all members of an organization have incentives to perform for a common interest. Sub-optimization – occurs when one segment of a company takes action that is in its own best interests, but is detrimental to the firm as a whole. BENEFITS OF DECENTRALIZATION 1. Better access to local information 2. 3. 4. 5. 6. 7. Cognitive limitations More timely response Focusing of central management Training and evaluation Motivation Enhanced competition. COSTS OF DECENTRALIZATION 1. Some decisions made in one sub-unit may bring about negative effect to the other sub-units or the organization as a whole. 2. Decentralization necessitates a more elaborate reporting system hence, the costs of gathering and reporting of data increase. 3. Job duplication or overlapping of functions is usually encountered in a decentralized set-up. MEASURING THE PERFORMANCE OF INVESTMENT CENTERS Performance measures for investment centers usually attempt to assess how well managers are utilizing invested assets of the division to produce profits by relating operating profits to assets. Return on investment (ROI) is the most common measure of performance for investment centers. ROI can be defined as follows: ROI = Operating Income Average Operating Assets Operating income refers to earnings before interest and taxes. Operating assets include all assets acquired to generate operating income, including cash, receivables, inventories, land, buildings, and equipment. The ROI formula can also be broken down into the product of margin and turnover. Margin is the ratio of operating income to sales. Turnover is defined as sales divided by average operating assets. ROI = Margin x Turnover or ROI = Operating Income Sales x Sales Average Operating Assets Three advantages of using ROI to evaluate the performance of investment centers: 1. It encourages managers to pay careful attention to the relationships among sales, expenses, and investment, as should be the case for a manager of an investment center. 2. It encourages cost efficiency. 3. It discourages excessive investment in operating assets. Two disadvantages of using ROI are: 1. It discourages managers from investing in projects that would decrease the divisional ROI but would increase the profitability of the company as a whole. (Generally, projects with an ROI less than a division’s current ROI would be rejected.) 2. It can encourage myopic behavior, in that managers may focus on the short run at the expense of the long run. Residual income (RI) - the difference between operating income and the minimum peso return required on a company’s operating assets. The equation for RI can be expressed as follows: RI = Operating Income (Minimum Rate of Return x Operating Assets) ECONOMIC VALUE ADDED (EVA) – a more specific version of residual income. It represents the segment’s true economic profit because it measures the benefit obtained by using resources in a particular way. After-tax operating income (EBIT x[1 – Tax Rate]) Less desired income (After-tax WACC* x [Total assets –Current liabilities]) Economic Value Added (EVA) xx xx xx * WACC = Weighted average cost of capital TRANSFER PRICING TRANSFER PRICE – the monetary value or the price charged by one segment of a firm for the goods and services it supplies to another segment of the same firm. OBJECTIVES OF TRANSFER PRICING 1. 2. 3. To facilitate optimal decision-making. To provide a basis in measuring divisional performance. To motivate the different department heads in improving their performance and that of their departments. APPROACHES FOR DETERMINING TRANSFER PRICE: 1. Negotiated transfer price 2. Cost-based transfer price 3. Market-based transfer price General Rules in Choosing a Transfer Price The maximum price should be no greater than the lowest market price at which the buying segment can acquire the goods or services externally. The minimum price should be no less than the sum of the selling segment’s incremental costs associated with the goods or services plus the opportunity cost of the facilities used. A good should be transferred internally whenever the minimum transfer price (set by the selling division) is less than the maximum transfer price (set by the buying division). By using this rule, total profits of the firm are not decreased by an internal transfer. TRANSFER PRICING one division of a manufacturing company supplies components or materials to another division, the price charged by the selling (producing) division to the buying division is known as the TRANSFER PRICE. the following methods: MARKET price – regarded as the best transfer price that maximizes the over-all company profit, provided that: (1) a competitive market price exists, and (2) divisions are independent of each other. COST-BASED price – easy to understand and convenient to use but inefficiencies of the selling division may be passed on to the buying division with little incentive to control costs. Cost-based price can be based on selling division’s variable cost, full (absorption) cost or cost-plus. NEGOTIATED price – widely used when market prices are subject to rapid fluctuation or no intermediate market price exists. In negotiating a transfer price, the usual range shall be based on the following: : market price ARBITRARY price – normally imposed by the corporate headquarters to promote over-all company goals with neither the selling division nor the buying division having a control over the price. organization may suffer from sub-optimization. Management hence establishes the methodology for setting transfer prices in such a way to promote GOAL CONGRUENCE, which occurs when division managers make decisions that are consistent with the goals and objectives of the organization as a whole. goal congruence, other important factors considered in setting the transfer price include cost structure, capacity constraints, segmental performance, negotiation flexibility and tax implications. Transfer price per unit = outlay cost per unit + opportunity cost per unit variable overhead) plus any additional costs incurred (e.g., storage, transportation, administrative). COST refers to the margin or profit sacrificed by transferring units internally rather than selling them to external customers. Depending on sales demand and production capacity of the selling division, there may or may not be an opportunity cost associated with the internal transfer: ity): market price is the ‘theoretically correct’ transfer price. apacity, transfer price must be based on the variable costs incurred to produce each unit. In practice, this price usually serves as the MININUM (floor) or lower threshold in a transfer price negotiation or as the basis for cost-based pricing. ING is an attempt to eliminate the internal conflicts associated with transfer prices by giving both the buying and selling divisions the price that works best for them: -out price to prevent decrease in divisional income -in price to minimize divisional costs and avoid ‘profit sharing’ with selling division by agreeing to a transfer price above cost. Dual pricing is rarely used nowadays because of the little incentive to control costs -- neither manager from both buying divisions (assured of a low price) and selling divisions (assured of high price) must exert much effort to show a profit on segmental performance reports THE BALANCED SCORECARD: STRATEGIC-BASED CONTROL The Balanced Scorecard BSC was created by David Norton and Robert Kaplan in response to VALUE-BASED MANAGEMENT, which is a performance evaluation technique that focuses on traditional financial measures. It is a strategic management system that defines a strategic-based responsibility accounting system. Strategy is defined as choosing the market and customer segments the business unit intends to serve, identifying the critical internal and business processes that the unit must excel at to deliver the value propositions to customers in the targeted market segments, and selecting the individual and organizational capabilities required for the internal, customer, and financial objectives. The Balanced Scorecard translates an organization’s mission and strategy into operational objectives and performance measures for four different perspectives: the financial perspective, the customer perspective, the internal business process perspective, and the learning and growth (infrastructure) perspective. Common characteristics of balanced scorecards a. It should be possible, by examining a company’s balanced scorecard, to infer its strategy and the assumptions underlying that strategy. b. The balanced scorecard should emphasize continuous improvement rather than just meeting present standards or targets. c. Some of the performance measures on the balanced scorecard should be non-financial. d. The scorecards for individuals should contain only those performance measures they can actually influence. e. The ultimate objectives of the organization are usually financial, but better financial results cannot be attained without improving customers’ perceptions of the company’s products and services. In order to improve customers’ perceptions of products and services, it is usually necessary to improve internal business processes so that the products and services are actually better. And in order to improve the business processes, it is necessary that employees learn. The balanced scorecard as a motivation and feedback mechanism. The performance measures on the balanced scorecard provide motivation and feedback for improving. BSC translates an organization’s mission and strategy into a comprehensive set of financial (lagging indicators) and non-financial performance (leading indicators) metrics classified into four (4) perspectives The Financial Perspective The financial perspective establishes the long- and short-term financial performance objectives. The financial perspective is concerned with the global financial consequences of the other three perspectives. Thus, the objectives and measures of the other perspectives must be linked to the financial objectives. The financial perspective has three strategic themes: revenue growth, cost reduction, and asset utilization. Customer Perspective The customer perspectiveis the source of the revenue component for the financial objectives. This perspective defines and selects the customer and market segments in which the company chooses to compete. Process Perspective To provide the framework needed for this perspective, a process value chain is defined. The process valuechain is made up of three processes: the innovation process, the operations process, and the postsalesprocess. Cycle time is the time required to produce one unit of product. Velocity is the number of units that can be produced in a given period of time (e.g., units per hour). Learning/Innovation and Growth Perspective The learning and growth perspective is the source of the capabilities that enable the accomplishment of the other three perspectives’ objectives. STRATEGY MAPPING is a process that links the four BSC perspectives with company strategies based on a cause-and-effect pattern to see where value can be added further. A typical BSC report contains: – statements of what strategy must achieve and what is critical to its success. – key action programs required to achieve strategic objectives. – describe how success in achieving the strategy will be measured. – the current level of performance for the performance measure. – the level of performance or rate of improvement needed in the performance measure. NOTE: Strategic objectives focus on WHAT is to be achieved. Strategic initiatives focus on HOW it will be achieved. Performance measures, baseline performance and targets relate to how it will be MEASURED. KEY PERFORMANCE INDICATORS (KPIs) are specific, measureable financial and non-financial elements of a firm’s performance that are vital to its competitive advantage. of company strategies by helping management identify what needs to be done and how its achievement can be measured to determine organizational success SOME INTERNAL BUSINESS PROCESS PERFORMANCE MEASURES. a. Delivery Cycle Time. This is the total elapsed time between when an order is placed by a customer and when it is shipped to the customer. Part of this time is wait time that occurs before the order is placed into production. b. Throughput (Manufacturing Cycle) Time. This is the total elapsed time between when an order is initiated into production and when it is shipped to the customer. It consists of process time, inspection time, move time, and queue time. The only element that adds value is processing time. Inspection time, move time, queue time, and their associated activities do not add value and should be minimized. c. Manufacturing Cycle Efficiency (MCE). MCE is the ratio of value-added time (i.e., process time) to total throughput time. It represents the percentage of time an order is in production in which useful work is being done. The rest of the time represents non-value-added time (i.e., inspection time, move time, and queue time). Manufacturing Cycle Efficiency (MCE) can be found as follows: MCE = Processing time Processing time + Move Time + Inspection Time + Wait time QUALITY COST MEASUREMENT: Quality-linked activities are those activities performed because poor quality may or does exist. Costs of quality are costs that exist because poor quality may or does exist. Control activitiesare performed by an organization to prevent or detect poor quality. Control costs are the costs of performing control activities. There are two broad categories of control costs: prevention costs and appraisal costs. Prevention costs are incurred to prevent poor quality in the products or services being produced. Appraisal costs are incurred to determine whether products and services are conforming to their requirements or customer needs. Failure activitiesare performed by an organization or its customers in response to poor quality. Failure costs are the costs incurred by an organization because failure activities are performed. There are two broad categories of failure costs: internal failure costs and external failure costs. Internal failure costs are incurred because products and services do not conform to specifications or customer needs and the nonconformance is detected prior to being delivered to outside parties. External failure costs are incurred because products or services fail to conform to requirements or satisfy customer needs and the nonconformance is detected after being delivered to outside parties. PRODUCTIVITY MEASUREMENT Productivity – measures the relationship between actual inputs used (both quantities and costs) and actual outputs produced. Partial productivity – compares the quantity of output produced with the quantity of an individual input used. Partial Productivity = 𝑄𝑢𝑎𝑛𝑡𝑖𝑡𝑦 𝑜𝑓 𝑜𝑢𝑡𝑝𝑢𝑡 𝑝𝑟𝑜𝑑𝑢𝑐𝑒𝑑 𝑄𝑢𝑎𝑛𝑡𝑖𝑡𝑦 𝑜𝑓 𝑖𝑛𝑝𝑢𝑡 𝑢𝑠𝑒𝑑 Total Factor Productivity – the ratio of quantity of output produced to the costs of all inputs used based on current period prices. Total factor productivity = 𝑄𝑢𝑎𝑛𝑡𝑖𝑡𝑦 𝑜𝑓 𝑜𝑢𝑡𝑝𝑢𝑡 𝑝𝑟𝑜𝑑𝑢𝑐𝑒𝑑 𝐶𝑜𝑠𝑡𝑠 𝑜𝑓 𝑎𝑙𝑙 𝑖𝑛𝑝𝑢𝑡𝑠 𝑢𝑠𝑒𝑑