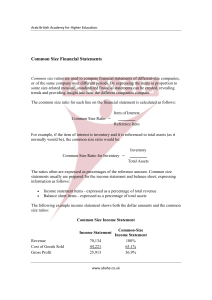

WORKING WITH FINANCIAL STATEMENTS 14-1 Financial Statement Analysis 14-2 Horizontal analysis (Comparative Analysis), also called trend analysis Vertical analysis (Common Size Analysis) Ratio Analysis 3-2 Horizontal Analysis Horizontal analysis, also called trend analysis, is a technique for evaluating a series of financial statement data over a period of time. 14-3 Purpose is to determine the increase or decrease. Commonly applied to the ► balance sheet, ► income statement, and ► statement of retained earnings. LO 1 Horizontal Analysis 14-4 Horizontal Analysis Illustration 14-5 Horizontal analysis of balance sheets Changes suggest that the company expanded its asset base during 2013 and financed this expansion primarily by retaining income rather than assuming additional long-term debt. 14-5 LO 1 Horizontal Analysis 14-6 LO 1 Horizontal Analysis Illustration 14-6 Horizontal analysis of Income statements Overall, gross profit and net income were up substantially. Gross profit increased 17.1%, and net income, 26.5%. Quality’s profit trend appears favorable. 14-7 LO 1 Horizontal Analysis Illustration 14-7 Horizontal analysis of retained earnings statements 14-8 The ending retained earnings increased 38.6%. As indicated earlier, the company retained a significant portion of net income to finance additional plant facilities. LO 1 Vertical Analysis Vertical analysis, also called common-size analysis When comparing the financial statements to those of other similar companies, we may have a problem : Differences in size GM and Ford Differences in Currency GM and Toyota. Therefore we do prepare Common-Size Statements 14-9 Common-Size Balance Sheets Common-Size Income Statements Common-size Balance Sheets 14-10 Common-size Balance Sheets restates the balance sheets items as a percentage of total assets • In other words, we compute all accounts as a percent of total assets Basket Wonders’ Common Size Balance Sheets Regular (thousands of $) Assets 2002 2003 2001 2002 2003 Cash AR Inv Other CA 148 283 322 10 100 410 616 14 90 394 696 15 12.10 23.14 26.33 0.82 4.89 20.06 30.14 0.68 4.15 18.17 32.09 0.69 Tot CA Net FA LT Inv Other LT 763 349 0 111 1,140 631 50 223 1,195 701 50 223 62.39 28.54 0.00 9.08 55.77 30.87 2.45 10.91 55.09 32.32 2.31 10.28 1,223 2,044 2,169 100.0 100.0 100.0 Tot Assets 14-11 2001 Common-Size (%) Basket Wonders’ Common Size Balance Sheets Regular (thousands of $) Liab+Equity 14-12 2001 2002 2003 Common-Size (%) 2001 2002 2003 Note Pay Acct Pay Accr Tax Other Accr 290 81 13 15 295 94 16 100 290 94 16 100 23.71 6.62 1.06 1.23 14.43 4.60 0.78 4.89 13.37 4.33 0.74 4.61 Tot CL LT Debt Equity 399 150 674 505 453 1,086 500 530 1,139 32.62 12.26 55.11 24.71 22.16 53.13 23.05 24.44 52.51 Tot L+E 1,223 2,044 2,169 100.0 100.0 100.0 Common-size Income Statement Common-size income statement restates the income statement items as a percentage of sales. • In other words, we compute all line items as a percent of sales 14-13 Basket Wonders’ Common Size Income Statements Regular (thousands of $) 2001 Net Sales COGS 14-14 2002 2003 Common-Size (%) 2001 2002 2003 1,235 849 2,106 1,501 2,211 1,599 100.0 68.7 100.0 71.3 100.0 72.3 Gross Profit Adm. 386 180 605 383 612 402 31.3 14.6 28.7 18.2 27.7 18.2 EBIT Int Exp 206 20 222 51 210 59 16.7 1.6 10.5 2.4 9.5 2.7 EBT 186 171 151 15.1 8.1 6.8 EAT 112 103 91 9.1 4.9 4.1 Cash Div 50 50 50 4.0 2.4 2.3 Vertical Analysis Illustration 14-8 Vertical analysis of balance sheets Quality is choosing to finance its growth through retention of earnings rather than through issuing additional debt. 14-15 LO 1 Vertical Analysis Illustration 14-8 Vertical analysis of balance sheets These results indicate the company shifted toward equity financing by relying less on debt and by increasing the amount of retained earnings. 14-16 LO 1 Vertical Analysis Illustration 14-9 Vertical analysis of Income statements Quality appears to be a profitable enterprise that is becoming even more successful. 14-17 LO 1 Vertical Analysis Enables a comparison of companies of different sizes. Illustration 14-10 Intercompany income statement comparison 14-18 LO 1 Ratio Analysis Ratio analysis expresses the relationship among selected items of financial statement data. Financial Ratio Classifications 14-19 Measuring Key Financial Relationships: Six Key Questions 14-20 1. How liquid is the firm? 2. Is management generating adequate operating profits on the firm’s assets? 3. How is the firm financing its business? 4. Is management providing a good return on the capital provided by the shareholders? (Management Effectiveness) 5. Is the management team creating shareholder value? (Valuations Ratios) 6. Efficiency Ratio Analysis Liquidity Ratios Measure the short-term ability of the company to pay its maturing obligations and to meet unexpected needs for cash. Short-term creditors such as bankers and suppliers are particularly interested in assessing liquidity. Ratios include the current ratio, the acid-test ratio, accounts receivable turnover, inventory turnover, and working capital. 14-21 LO 2 QUALITY DEPARTMENT STORE INC. Balance Sheet (partial) 2013 2012 QUALITY DEPARTMENT STORE INC. Condensed Income Statements For the Years Ended December 31 2013 2012 Illustration 14-12 14-22 LO 2 Ratio Analysis Liquidity Ratios 1. CURRENT RATIO 2013 Illustration 14-12 2012 1.52:1 Ratio of 2.96:1 means that for every dollar of current liabilities, Quality has $2.96 of current assets. 14-23 LO 2 Ratio Analysis Liquidity Ratios 2. ACID-TEST RATIO (Quick Ratio) Illustration 14-13 2013 14-24 2012 LO 2 QUALITY DEPARTMENT STORE INC. QUALITY DEPARTMENT STORE INC. Balance Sheet (partial) Balance Sheet (partial) 2013 2012 2013 2012 Illustration 14-12 14-25 LO 2 Ratio Analysis Liquidity Ratios 2. ACID-TEST RATIO (Quick Ratio) Illustration 14-14 2013 2012 0.47:1 Acid-test ratio measures immediate liquidity. 14-26 LO 2 The Operating Cycle 14-27 Operating cycle = time between purchasing the inventory and collecting the cash from sale of the inventory Inventory period = time required to purchase and sell the inventory the days in inventory Accounts receivable period = time required to collect on credit sales average collection period QUALITY DEPARTMENT STORE INC. Balance Sheet (partial) 2013 14-28 2012 QUALITY DEPARTMENT STORE INC. Condensed Income Statements For the Years Ended December 31 2013 2012 LO 2 Ratio Analysis Liquidity Ratios 3. ACCOUNTS RECEIVABLE TURNOVER Illustration 14-15 2013 2012 69.1 times Measures the number of times, on average, the company collects receivables during the period. 14-29 LO 2 Ratio Analysis Liquidity Ratios 3. ACCOUNTS RECEIVABLE TURNOVER $2,097,000 = 10.2 times ($180,000 + $230,000) / 2 A variant of the accounts receivable turnover ratio is to convert it to an average collection period in terms of days. 365 days / 10.2 times = every 35.78 days Accounts receivable are collected on average every 36 days. 14-30 LO 2 QUALITY DEPARTMENT STORE INC. Balance Sheet (partial) 2013 2012 QUALITY DEPARTMENT STORE INC. Condensed Income Statements For the Years Ended December 31 2013 2012 Illustration 14-12 14-31 LO 2 Ratio Analysis Liquidity Ratios 4. INVENTORY TURNOVER Illustration 14-16 2013 2012 3.1 times Measures the number of times, on average, the inventory is sold during the period. 14-32 LO 2 Ratio Analysis Liquidity Ratios 4. INVENTORY TURNOVER $1,281,000 = 2.3 times ($500,000 + $620,000) / 2 A variant of inventory turnover is the days in inventory. 365 days / 2.3 times = every 159 days Inventory turnover ratios vary considerably among industries. 14-33 LO 2 Ratio Analysis 5. WORKING CAPITAL Illustration 2-14 Working capital is the difference between the amounts of current assets and current liabilities. Best Buy had working capital in 2011 of $1,810 million ($10,473 million - $8,663 million). 14-34 The Balance Sheet 14-35 2-35 Ratio Analysis 14-36 Larger the working capital, better the firm’s ability to repay its debt Working capital can be positive or zero or negative. It is generally positive. Usually positive in a healthy firm An increase in working capital may not always be good news. For example, if the level of inventory goes up, current assets will increase and thus Working capital will also increase. However, increasing inventory level may well be a sign of inability to sell. Measuring Key Financial Relationships: Six Key Questions 14-37 1. How liquid is the firm? 2. Is management generating adequate operating profits on the firm’s assets? 3. How is the firm financing its business? 4. Is management providing a good return on the capital provided by the shareholders? (Management Effectiveness) 5. Is the management team creating shareholder value? (Valuations Ratios) 6. Efficiency Ratio Analysis Profitability Ratios Measure the income or operating success of a company for a given period of time. Income affects the company’s ability to obtain debt and equity financing, their liquidity position, and their ability to grow. 14-38 Ratios include profit margin asset turnover return on assets LO 2 QUALITY DEPARTMENT STORE INC. Condensed Balance Sheets 2013 14-39 2012 QUALITY DEPARTMENT STORE INC. Condensed Income Statements For the Years Ended December 31 2013 2012 LO 2 Ratio Analysis Profitability Ratios 6. PROFIT MARGIN Illustration 14-17 2013 2012 5.3% Measures the percentage of each dollar of sales that results in net income. 14-40 LO 2 QUALITY DEPARTMENT STORE INC. Condensed Balance Sheets 2013 2012 QUALITY DEPARTMENT STORE INC. Condensed Income Statements For the Years Ended December 31 2013 2012 Illustration 14-12 14-41 LO 2 Ratio Analysis Profitability Ratios 7. ASSET TURNOVER Illustration 14-18 2013 2012 1.3 times Measures how efficiently a company uses its assets to generate sales. 14-42 LO 2 QUALITY DEPARTMENT STORE INC. Condensed Balance Sheets 2013 2012 QUALITY DEPARTMENT STORE INC. Condensed Income Statements For the Years Ended December 31 2013 2012 Illustration 14-12 14-43 LO 2 Ratio Analysis Profitability Ratios 8. RETURN ON ASSET Illustration 14-19 2013 2012 7.0% An overall measure of profitability. 14-44 LO 2 Measuring Key Financial Relationships: Six Key Questions 14-45 1. How liquid is the firm? 2. Is management generating adequate operating profits on the firm’s assets? 3. How is the firm financing its business? 4. Is management providing a good return on the capital provided by the shareholders? (Management Effectiveness) 5. Is the management team creating shareholder value? (Valuations Ratios) 6. Efficiency Ratio Analysis Solvency Ratios Solvency ratios measure the ability of a company to survive over a long period of time. Debt to Assets Debt to Equity Is ratio that provide information about debt-paying ability. 14-46 LO 2 QUALITY DEPARTMENT STORE INC. Condensed Balance Sheets 2013 2012 QUALITY DEPARTMENT STORE INC. Condensed Income Statements For the Years Ended December 31 2013 2012 Illustration 14-12 14-47 LO 2 Ratio Analysis Solvency Ratios 9. DEBT TO TOTAL ASSETS RATIO Illustration 14-25 2013 2012 71.1% Measures the percentage of the total assets that creditors provide. 14-48 LO 2 10. DEBT TO EQUITY RATIO QUALITY DEPARTMENT STORE INC. Condensed Balance Sheets 2013 2012 QUALITY DEPARTMENT STORE INC. Condensed Income Statements For the Years Ended December 31 2013 2012 Illustration 14-12 $832,000 = 82,95% 1,003,000 14-49 LO 2 Measuring Key Financial Relationships: Six Key Questions 14-50 1. How liquid is the firm? 2. Is management generating adequate operating profits on the firm’s assets? 3. How is the firm financing its business? 4. Is management providing a good return on the capital provided by the shareholders? (Management Effectiveness) 5. Is the management team creating shareholder value? (Valuations Ratios) 6. Efficiency Ratio Analysis Profitability Ratios Measure the income or operating success of a company for a given period of time. Income affects the company’s ability to obtain debt and equity financing, their liquidity position, and their ability to grow. Ratios include 14-51 return on common stockholders’ equity LO 2 QUALITY DEPARTMENT STORE INC. Condensed Balance Sheets 2013 2012 QUALITY DEPARTMENT STORE INC. Condensed Income Statements For the Years Ended December 31 2013 2012 Illustration 14-12 14-52 LO 2 Ratio Analysis Profitability Ratios 11. RETURN ON COMMON STOCKHOLDERS’ EQUITY 2013 Illustration 14-20 2012 24.2% Shows how many dollars of net income the company earned for each dollar invested by the owners. 14-53 LO 2 Measuring Key Financial Relationships: Six Key Questions 14-54 1. How liquid is the firm? 2. Is management generating adequate operating profits on the firm’s assets? 3. How is the firm financing its business? 4. Is management providing a good return on the capital provided by the shareholders? (Management Effectiveness) 5. Is the management team creating shareholder value? (Valuations Ratios) 6. Efficiency Quality of Earnings Price-Earnings Ratio Reflects investors’ assessment of a company’s future earnings. P-E ratio will be higher if investors think that earnings will increase substantially in the future. P-E ratio will be lower when there is the belief that a company has poor-quality earnings. Illustration 13-19 14-55 LO 7 Understand the concept of quality of earnings. Quality of Earnings Price-Earnings Ratio Illustration 13-19 Illustration 13-20 Earnings per share and P-E ratios of various companies 14-56 LO 7 Understand the concept of quality of earnings. Book value balance sheet assets liabilities equity Assets 14-57 = Liabilities + Equity Book value • • • • • • 14-58 Book value is a relatively straightforward concept Book value is literally the value of a company that can be found on the accounting ledger Book value per share = Shareholder’s equity Number of share outstanding If you then take share price and divide by the current book values, you have the price-to-book ratio The closer to book value you can buy something at, the better it is To value the financial companies like banks, multi finance, leasing, brokerages and credit card companies, the book value is extremely relevant. 58 Book value / price-to-book value 14-59 59 14-60 60 14-61 61 PT Astra International Tbk 14-62 62 Price-to-book value Compares the market value of a share of stock to the book value per share of the reported equity on the balance sheet. Formula: = Price per share/Equity book value per share 14-63 A ratio greater than 1 indicates that the shares are more valuable than what the shareholders originally paid. Measuring Key Financial Relationships: Six Key Questions 14-64 1. How liquid is the firm? 2. Is management generating adequate operating profits on the firm’s assets? 3. How is the firm financing its business? 4. Is management providing a good return on the capital provided by the shareholders? (Management Effectiveness) 5. Is the management team creating shareholder value? (Valuations Ratios) 6. Efficiency 6. Efficiency 14-65 We can use five approaches to answer this question: Revenue / Employee Net Income / Employee Receivable Turnover Inventory Turnover Total Asset Turnover These ratios indicate how efficient of management’s past performance.