Corporate Finance (B02030)

Ton Duc Thang University

Module 2

HOW TO CALCULATE PRESENT VALUES

Future Value and Compounding

The future value (FV) is the amount to which an investment will grow after earning interest.

If you invest $ today at an interest rate of r, you will have $ + $(r) = $(1 + r) in one year.

Example: $100 at 10% interest per year gives $100(1.1) = $110.

Reinvesting the interest, we earn interest on interest, i.e., compounding FV = $(1 + r)(1 + r) = $(1 + r)2

Example: $100 at 10% interest per year for 2 years gives $100(1.1)(1.1) = $100(1.1)2 = $121.

In general, for t periods, FV = $(1 + r)t where (1 + r)t is the compound interest or interest earned on

interest at the rate, r, for t periods. It is also called future value interest factor, FVIF(r,t).

Example: $100 at 10% interest per year for 10 years gives $100(1.1)10 = $259.37.

Interest can be compounded more than once a year. In such cases, the formula for FV becomes: FV

= $ (1 + (r / m))t x m, where m is the number of total compounding periods in a year.

Example: $100 at 10% interest per year compounded semi-annually for 3 years gives $100(1+(0.10 /

2))3 x 2 = $100(1 + 0.5)6 = $134.

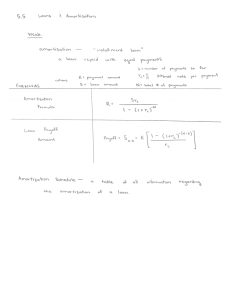

Present Value and Discounting

The value today of a future cash flow is called the present value (PV). Remember that FV = $(1 + r).

Rearrange and solve for $, which is the present value. Therefore, PV = FV / (1 + r).

Example: $110 in 1 period with an interest rate of 10% has a PV = $110 / (1.1) = $100.

PV of future amount in t periods at r is: PV = FV [1 / (1 + r)t] where [1 / (1 + r)t] is the discount factor,

or the present value interest factor, PVIF(r,t).

Example: If you have $259.37 in 10 periods and the interest rate was 10%, how much did you deposit

initially?

PV = $259.37 [1/(1.1)10] = $259.37(.3855) = $100

Present values are directly related to the future cash flows and inversely related to the discount rate,

r, and time, t. The higher the future cash flows, the higher the PV; the higher the discount rate

and longer the term, the lower the PV.

More on Present and Future Values

Present Value versus Future Value. Present value interest factors are reciprocals of future value

interest factors: PVIF(r,t) = 1 / (1 + r)t and FVIF(r,t) = (1 + r)t

Example: FVIF(10%,4) = 1.14 = 1.464; PVIF(10%,4) = 1 / 1.14 = 0.683

Basic present value equation: PV = FV [1 / (1 + r)t] = FV / (1 + r)t

1

Corporate Finance (B02030)

Ton Duc Thang University

Determining the Discount Rate. Rearrange the PV equation to solve for r: r = (FV / PV)1/t – 1

Example: What interest rate makes a PV of $100 become a FV of $150 in 6 periods?

r = (150 / 100)1/6 – 1 = 7%

Finding the Number of Periods. Rearrange the PV formula and solve for t.

t = ln(FV / PV) / ln(1 + r)

Example: How many periods before $100 today grows to $150 at 7%?

t = ln(150 / 100) / ln(1.07) = 6 periods

Multiple Cash Flows

Many finance situations involve more than one cash flow. Whether they are equal, consecutive

payments or irregular, unequal cash flows over time, they are referred to as a stream of cash flows.

Present Value of Multiple Cash Flows. Calculating the present value of an unequal series of future

cash flows is determined by summing the present values of each discounted single future cash flow.

Example: An investor has determined that the expected future cash flows of an asset will follow the

following schedule: $5,000 at the beginning of year 1, $2,000 at the beginning of year 2, $500 at the

beginning of year 3, and $10,000 at the beginning of year 4. Suppose that the discount rate from the

cash flows above is 8%. What is the present value of the cash flows at 8%?

Year

1

2

3

4

Cash Flows

$5,000

$2,000

$500

$10,000

PVIF(r,t)

-(1 + 0.8)

(1 + 0.8)2

(1 + 0.8)3

PV

$5,000.00

$1,851.85

$428.67

$7,938.32

$15,218.84

PV = $5,000 + $2,000 / (1 + 0.8) + $500 / (1 + 0.8)2 + $10,000 + (1 + 0.8)3 = $15,218.84

Perpetuities

A perpetuity is a perpetual annuity; that means, cash flows go on forever. The PV of a perpetuity is

equal to the periodic cash flow divided by the appropriate discount rate, or PV = C / r.

Example: If a person receives $500 per year forever, beginning next year, and the interest rate is a

constant 5% forever, what is the present value of the cash flows?

PV = C / r = $500 / 0.05 = $10,000

Cash flows growing at a constant rate. The present value of a stream of cash flows growing at a

constant rate, g, is given by the following formula: PV = C / (r - g).

For example: Assume that the cash flows are annually adjusted for expected growth of 6%. How

much should the present value be if the first year’s cash flow is $100 and the discount rate is 8%?

PV = C / (r - g) = $100 / (0.08 - 0.06) = $5,000

2

Corporate Finance (B02030)

Ton Duc Thang University

Annuities

An annuity is a series of equal cash flows that occur at regular intervals for a fixed number of time

periods.

Present Value for Annuity Cash Flows. The present value of an annuity of cash flow C per period

for t periods at r percent interest: PV = C[1 – 1/(1 + r)t] / r

Example: If a person is willing to make 36 monthly payments of $100 at 1.5% per month, what size

loan can you obtain?

PV = 100[1 – 1/(1.015)36] / .015 = 100(27.6607) = $2,766.07

To find the payment, C, given PV, r, and t, use C = PV {r / [1 – 1/(1 + r)t]}

To find the number of payments given PV, C, and r, use t = ln[1 / (1 – rPV/C)] / ln(1 + r)

Example: How many P100 payments will pay off a P5,000 loan at 1% per period?

t = ln[(1 / 1 - .01(5,000)/100)] / ln(1.01) = 69.66 periods

Example: If you borrow $400, promising to repay in 4 monthly installments at 1% per month, how

much are your payments?

C = $400 {.01 / [1 – 1/(1.01)4]} = $400(0.2563) = $102.51

Future Value for Annuities. FV = C[(1 + r)t – 1] / r

Example: If you make 20 payments of $1,000 at the end of each period at 10% per period, how much

will your account grow to be?

FV = $1,000[(1.1)20 – 1] / .1 = $1,000(57.275) = $57,275

EAR and APR

Consider a bank which pays 6% interest per year, compounded quarterly; this is equivalent to 1.5%

interest each quarter. The 6% rate in this example is sometimes referred to as the annual

percentage rate, stated interest rate, the quoted rate or the nominal rate. However, when interest

is compounded more than once a year, the actual rate the depositor receives is greater than the

quoted rate. The true rate is often called the effective annual rate or the effective annual yield.

EAR = [1 + APR / m]m – 1 where m is the number of periods per year

Example: 6% compounded monthly is [1 + (0.06/12)]12 – 1 = 16.67%.

Compounding

Period

Annually

Semiannually

Quarterly

Monthly

Weekly

Daily

Continuously

Periods per

Year (m)

1

2

4

12

52

365

∞

Per-Period Interest

Rate (APR / m)

0.06

0.12 / 2 = 0.03

0.12 / 4 = 0.015

0.12 / 12 = 0.005

0.12 / 52 = 0.0011538

0.12 / 365 = 0.0001644

--

Growth Factor of Invested

Funds ((1 + APR)m)

1.06

1.032

1.0154

1.00512

0.001153852

1.0001644365

e0.06

Effective

Annual Rate

6.000%

6.090%

6.136%

6.168%

6.180%

6.183%

6.184%

3

Corporate Finance (B02030)

Ton Duc Thang University

To compute the APR given the EAR, APR = m[(1 + EAR)1/m – 1].

For example: 13.54% EAR is 4[(1 + 01354)1/4 – 1] = 12.9% APR compounded quarterly.

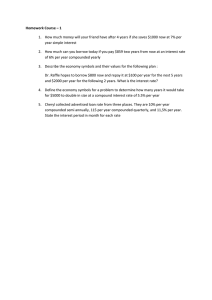

Exercises

1. First City Bank pays 8 percent simple interest on its savings account balances, whereas Second

City Bank pays 8 percent interest compounded annually. If you made a $5,000 deposit in each

bank, how much more money would you earn from your Second City Bank account at the end of

10 years? $10,794.62

2. Compute the future value of $1,000 compounded annually for:

a. 10 years at 5 percent. $1,628.89

b. 10 years at 10 percent. $2,593.74

c. 20 years at 5 percent. $2,653.30

3. For each of the following, compute the present value:

Present Value

$9,213.51

$12,465.48

$110,854.15

$13,124.66

Years

6

9

18

23

Interest Rate

7%

15%

11%

18%

Future Value

$13,827

$43,852

$725,380

$590,710

4. Solve for the unknown interest rate in each of the following:

Present Value

$242

$410

$51,700

$18,750

Years

4

8

16

27

Interest Rate

6.13%

10.27%

7.41%

12.79%

Future Value

$307

$896

$162,181

$483,500

5. Solve for the unknown number of years in each of the following:

Present Value

625

810

18,400

21,500

Years

8.35 years

16.09 years

19.65 years

27.13 years

Interest Rate

9%

11%

17%

8%

Future Value

$1,284

$4,341

$402,662

$173,439

6. At 8 percent interest, how long does it take to double your money? To quadruple it? (2) 9.01

years; (4) 18.01 years

7. Conoly Co. has identified an investment project with the following cash flows. If the discount rate

is 10 percent, what is the present value of these cash flows? What is the present value at 18

percent? At 24 percent? (10%) $3,191.49; (18%) $2,682.22; (24%) $2,381.91

Years

1

2

3

4

Cash Flow

$960

$840

$935

$1,350

4

Corporate Finance (B02030)

Ton Duc Thang University

8. An investor purchasing a British consol is entitled to receive annual payments from the British

government forever. What is the price of a consol that pays $150 annually if the next payment

occurs one year from today? The market interest rate is 4.6 percent. $3,260.87

9. Investment X offers to pay you $4,500 per year for nine years, whereas Investment Y offers to

pay you $7,000 per year for five years. Which of these cash flow streams has the higher present

value if the discount rate is 5 percent? If the discount rate is 22 percent? (5%) $31,985.20,

$30,306.34; (22%) $17,038.28, $20,045.48

10. An investment offers $4,900 per year for 15 years, with the first payment occurring one year from

now. If the required return is 8 percent, what is the value of the investment? What would the value

be if the payments occurred for 40 years? For 75 years? Forever? (15 year) $41,941.45; (40

years) $58,430.61; (75 years) $61,059.31

11. The Perpetual Life Insurance Co. is trying to sell you an investment policy that will pay you and

your heirs $15,000 per year forever. If the required return on this investment is 5.2 percent, how

much will you pay for the policy? Suppose the Perpetual Life Insurance Co. told you the policy

costs $320,000. At what interest rate would this be a fair deal? (a) $288,461.54; (b) 4.69%

12. Find the EAR in each of the following cases:

Stated Rate (APR)

7%

16

11

12

Number of Times

Compounded

Quarterly

Monthly

Daily

Infinite

Effective Rate (EAR)

7.19%

17.23%

11.63%

12.75%

13. Find the APR, or stated rate, in each of the following cases:

Stated Rate (APR)

9.57%

18.03%

7.98%

13.28%

Number of Times

Compounded

Semiannually

Monthly

Weekly

Infinite

Effective Rate (EAR)

9.8%

19.6%

8.3%

14.2%

17. First National Bank charges 11.2 percent compounded monthly on its business loans. First United

Bank charges 11.4 percent compounded semiannually. As a potential borrower, to which bank

would you go for a new loan? (National) 11.79%; (United) 11.72%

18. One of your customers is delinquent on his accounts payable balance. You’ve mutually agreed to

a repayment schedule of $700 per month. You will charge 1.3 percent per month interest on the

overdue balance. If the current balance is $21,500, how long will it take for the account to be paid

off? 39.46 months

5