Partnership Accounting: Definition, Nature, and Characteristics

advertisement

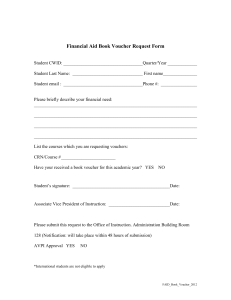

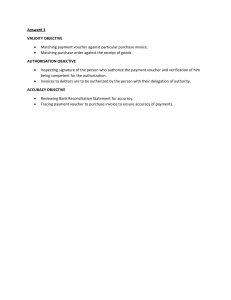

MODULE 1 = PARTNERSHIP ACCOUNTING Learning Objectives: At the end of the lesson the learner will be able to 1. Differentiate between the accounting for partnership, sole proprietorship, and corporation 2. Enumerate the essential elements of a partnership 3. Explain the nature of partnership 4. Enumerate the different characteristics of a partnership 1. DEFINITION, NATURE, ELEMENTS and CHARACTERISTICS 1.1 PARTNERSHIP - by the contract of partnership, two or more persons bind themselves to contribute money, property, or industry to a common fund with the intention of dividing profits among themselves. (Art. 1767 of the New Civil Code) Partnerships are governed by Articles 1767 to 1867 of the New Civil Code) 1.2 NATURE OF PARTNERSHIP 1. 2. 3. 4. 5. 6. Pooling of resources for common business purpose (money, noncash property or service) It could be employed for both small and large-scale operations It is an association of two or more persons having a legal capacity to enter into a contract There must be a valid contract, whether oral or written Art. 1772 and Art. 1773 of the New Civil Code provide that when the capital is P3,000 or more, it must be in public instrument and when the investment is in the form of immovable property. A partnership may be small enterprise selling goods or services at a single location or it may be a large enterprise with branches or offices at many different locations. 1.3 THE ESSENTIAL ELEMENTS OF A PARTNERSHIP UNDER ART. 1767 and 1770 OF THE NEW CIVIL CODE PROVIDE THE FOLLOWING: 1. There must be a consensual contract to create a partnership 2. There must be an agreement to contribute money, property or industry to a common fund 3. There must be an intention of dividing the profits among the partners 4. It must be established for a lawful purpose and for the common benefit or interest of the partners. 1.4 CHARACTERISTICS OF PARTNERSHIPS 1. EASE OF FORMATION As compared to corporation, the formation of a partnership requires less formality. 2. MUTUAL AGENCY Each partner is considered an agent of the partnership and any act of every partner including the execution in the name partnership name of any instrument for apparently carrying on in the usual way the business of the partnership of which he is a member, BINDS the partnership. (Art. 1818 of the New Civil Code) 3. JURIDICAL PERSONALITY The partnership has a juridical personality separate and distinct from that of each partners. (Art. 1768 of the Civil Code) 4. LIMITED LIFE The creation of a partnership is basically consensual. As such, a partnership may be dissolved: 4.1 - by express will of the any partner 4.2 - by the termination of a definite term stipulated in the contract 4.3 - by any event which makes it unlawful to carry out the partnership 4.4 - when a specific thing which a partner had promised to contribute to the partnership perishes before the delivery [ Art. 1830(4)]; 4.5 - expulsion, death, insolvency or civil interdiction of a partner 5. CO-OWNERSHIP OF PARTNERSHIP PROPERTY Partnership property belongs JOINTLY to all partners 6. PARTICIPATION IN PROFIT OR LOSSES Profits and losses are distributed among the partners in accordance with their agreement. In the absence of stipulation, the partners shall divide profit and losses in proportion to their capital contribution. The partnership is created as a busines (profitoriented entity), as such, each partner is entitled to his share in the partnership profits. A stipulation which exclude one or more partners from any share in the profits or losses is void. (Art. 1799 of the New Civil Code) 7. BASED UPON CONTRACT The contract may be written, orally expressed or implied. 8. UNLIMITED LIABILITY Each partner, including INDUSTRIAL PARTNER may be held personally liable for partnership debt after al partnership assets have been exhausted. A partnership in which ALL PARTNERS are individually liable is called a GENERAL PARTNERSHIP. A partnership in which at least one partner is personally liable is called a LIMITED PARTNERSHIP. Limited Partnership includes at least one general partner who maintains unlimited liability. The others, called “LIMITED PARTNERS”, may limit their liability up the extent of their contribution to the partnership. If partnership suffers losses and the partnership assets become insufficient to partnership liabilities, the creditors may satisfy their claims from the personal properties of the partners. (Article 1816 of the New Civil Code). 9. A VOLUNTARY ASSOCIATION Members of a partnership have the right to select the people with whom they will associate as partners. 2 - THE PARTNER’S ACCOUNT The accounting procedure of a partnership is the same as that of a single proprietorship. The day-to-day transactions are recorded in the same types of book of accounts. It is only in the accounting for transactions affecting net worth that partnership accounting differs from a single proprietorship. Since the ownership rights are divided among several partners, there must therefore be: 1. A CAPITAL ACCOUNT for each partner 2. A WITHDRAWAL ACCOUNT for each partner 3. An accurate computation and distribution of profits among the partners. CAPITAL ACCOUNT 3. Permanent withdrawals on 1. Original Investment investments 2. Subsequent investment DRAWING ACCOUNT 1. Withdrawals of the partner ( Cash, Merchandise, or other assets) 2. Payments made from partnership funds to settle personal obligations of the individual partner 3. Partnership receivable collected and retained by the individual partner 4. Partner’s share in the losses of the firm 5. Withdrawal of share in net income 1. Salary allowance and/or interest allowance to the partner as specified by the articles of incorporation 2. Payments made from personal fund of partner to settle certain outside liabilities of the partnership 3. Partner’s personal receivable collected and retained by the partnership 4. Partner’s share of the profit of the firm Proprietary Theory means that it looks at the entity through the eyes of the owners. Characteristics of a partnership that emphasizes that the entity is viewed as individual owners include the following: 1. Salaries to partners are viewed as distribution of income rather than a component of income 2. Unlimited liability of the general partner extends beyond the entity to the individual partner. 3. Income of the partnership is not taxed at the partnership level rather than, is included as part of the partners’ individual taxable income. 4. An original partnership is dissolved upon admission or withdrawal of a partner. The articles of co-partnership specify the permanent capital of the partners. To keep the same intact and not combined with the temporary changes in equity, the drawing or personal account of a partner is not closed to his capital. SELF CHECK 1.1 MULTIPLE CHOICE: 1. Which of the following is not a characteristic of a partnership? A. Limited liability B. Limited life C. Mutual Agency D. Ease of formation 2. Which of the following statements is correct with respect to a limited partnership? A. A limited partner may not be an unsecured creditor of the limited partnership. B. A general partner may not also be limited partner at the same time C. A general partner may be a secured creditor of the limited partnership D. A limited partnership can be formed with limited liability for all partners. 3. Which of the following is not a characteristic of the proprietary theory that influences accounting for partnership? A. Partners’ salaries are viewed as a distribution of income rather than a component of net income. B. partnership is not viewed as separate entity, distinct, taxable entity. C. A partnership is characterized by limited liability. D. Changes in the ownership structure of a partnership result in the dissolution of the partnership 4. An advantage of the partnership as a form of business organization would be A. Partners do not pay income taxes on their share in partnership income. B. A partnership is bound by the act of the partner. C. A partnership is created by mere agreements of the partners. D. A partnership may be terminated by the death or withdrawal of a partner. 5. Partnership capital and drawings accounts are similar to the corporate A. Paid in capital, retained earnings, and dividends accounts B. Retained earnings account C. Paid in capital and retained earnings accounts D. Preferred and common shares accounts 6. When a partnership is formed, equity dictates that assets and liabilities contributed to the partnership be recorded at what amount / value? A. Historical Cost B. Current values C. Adjusted tax basis D. Book values (NET BOOK VALUES) E. None of the above 7. The partnership form of organization is A. A legal entity B. A taxable entity C. A legal entity and a taxable entity D. Closer to being a corporation than a sole proprietorship E. None of the above It can also (1) Purchases – Raw Materials Purchases – Direct Materials THE VOUCHER SYSTEM The resources of the business must be protected from damage, loss, misuse. One of the characteristics of an effective and efficient accounting information system that it must make use of methods, procedures, and techniques that will allow for the proper control and monitoring of the business activities. The use of the VOUCHER SYSTEM is one way of protecting the business’ assets, more specifically CASH, by monitoring the purchases of goods and services, and the corresponding payments related to such purchase. VOUCHER SYSTEM DESCRIBED It is not enough to protect only the collection aspects of the handling of cash. The payment activities must be equally guarded and controlled. It is important to be assured that only authorized payments are made, and that the payments get to the proper parties. One common method of guarding and controlling payments is through the use of the voucher system. Payment of other factory costs incurred Credit- Cash not voucher payable (1) A voucher is a document used by a company's accounts payable department containing the supporting documents for an invoice. A voucher is essentially the backup documents for accounts payable, which are bills owed by companies to vendors and suppliers. The voucher is a document for recording liability while Invoice is a list of goods sold or services rendered, issued by the supplier to the customer when sales are made. ... On the contrary, an invoice includes details of the goods purchased from a particular company. A voucher is an internal document within a company that is issued by the accounts payable. Accounts payables are expected to be paid off within a year's time, or within one operating cycle (whichever is longer). What is the voucher system in accounting? : a system of accounting in which a voucher (as for an account payable) is prepared usually with supporting documents attached for each transaction or a series of transactions affecting a single account and when approved is entered in a voucher register. What Is a Voucher? A voucher is a document used by a company's accounts payable department to gather and file all of the supporting documents needed to approve the payment of a liability. A voucher is essentially the backup document for accounts payable.