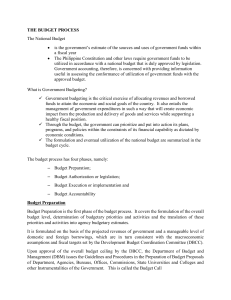

CHAPTER II Budget Process Learning Objectives • ENUMERATE THE STEPS IN THE BUDGET PROCESS. • DESCRIBE BRIEFLY THE PRINCIPLES OF RESPONSIBILITY ACCOUNTING. National Budget The National Budget (Government Budget) is the government’s estimate of the sources and uses of government funds within a fiscal year. This forms the basis for expenditures and is the government’s key instrument for promoting its socio-economic objectives. Performance-Informed Budgeting (PIB) National Expenditure Plan (NEP) and GAA 2014 will show the link between the fund allocated for government programs and the projected results and outcomes of these. National Budget The 1987, Philippine Constitution and other laws require government funds to be utilized in accordance with a national budget that is duly approved by lower and upper house. Government accounting, therefore, is concerned with providing information useful in assessing the conformance of utilization of government funds with the approved budget. National Budget The information and eventual utilization of the national budget are summarized in the Budget Cycle. Budget Cycle Has four (4) phases, namely: 1. 2. 3. 4. Budget Preparation Budget Legislation Budget Execution Budget Accountability BUDGET PREPARATION 1) Budget Call 2) Budget Hearings 3) Presentation to the Office of the President BUDGET LEGISLATION 1) House Deliberations 2) Senate Deliberations 3) Bicameral Deliberations 4) President’s Enactment THE APPROVED BUDGET The approved budget consists of the following: 1. New General Appropriations 2. Continuing Appropriations 3. Supplemental Appropriations 4. Automatic Appropriations 5. Unprogrammed Funds 6. Retained Income/Funds 7. Revolving Funds 8. Trust Receipts APPROPRIATION Appropriation – is the authorization made by a legislative body to allocate funds for purposes specified by the legislative or similar authority. 1. New General Appropriations - annual authorizations for incurring obligations, as listed in the GAA. 2. Continuing Appropriations - authorizations to support the incurrence of obligations beyond the budget year (e.g., multi-year construction projects). 3. Supplemental Appropriations – additional appropriations to augment the original appropriations which proves to be insufficient. 4. Automatic Appropriations - authorizations programmed annually which do not require periodic action by Congress. APPROPRIATION 5. Unprogrammed Funds – standby appropriations which may be availed only upon the occurrence of certain instances. 6. Retained Income/ funds - collections which the agencies can use directly in their operations. 7. Revolving funds – receipts from business-type activities of agencies which are authorized to be constituted as such. These are self-liquidating and all obligations and expenditures incurred by virtue of said business-type activity shall be charged against the fund. 8. Trust Receipts- receipts by a government agency acting as agent. BUDGET EXECUTION 1) Release Guidelines and BEDs Major recipients of budget: a. NGAs b. LGUs c. GOCCs 2) Allotment 3) Incurrence of Obligations 4) Disbursement Authority Disbursement Authority 1. Notice of Cash Allocation (NCA) – authority issued by the DBM to central, regional and provincial offices and operating units to cover their cash requirements. The NCA specifies the maximum amount of cash that can be withdrawn from a government servicing bank in a certain period. 2. Notice of Transfer of Allocation – authority issued by an agency’s Central Office to its regional and operating units to cover the latter’s cash requirements. 3. 4. Non-Cash Availment Authority – authority issued by the DBM to agencies to cover the liquidation of their actual obligations incurred against available allotments for availment of proceeds from loans/grants through supplier’s credit/constructive cash. Cash Disbursement Ceiling – authority issued by the DBM to agencies with foreign operations allowing them to use the income collected by their Foreign Service Posts to cover their operating requirements. BUDGET ACCOUNTABILITY Thank You!