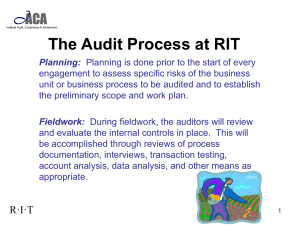

The third phase of the audit is the communication of results, often referred to as reporting. When auditees know about the auditor’s observation, there is no possibility that the individuals involved will modify their behavior so it is viewed favorably by the auditor. FALSE While increases in sales is always welcome news, if these figures appear dubious, internal audit may review the related transactions to verify they are all legitimate, they have not been recorded in the correct amount, and posted during the correct period. FALSE This involves the “reverse-trace” of a transaction from the destination (e.g., financial, operational, or regulatory report) to its source (e.g., sales order, purchase, and time sheet). Vouch Examples of Testimonials include the steps performed while processing a loan application, how the employee pays incoming invoices, the procedures to record the purchase of inventory in the accounting system, or the steps followed when notified that an employee has been hired and access needs to be granted to the computer systems. The reporting phase includes scoping, budgeting, defining the population of interest, how testing will be performed, and announcing the audit. Planning is arguably the most important part of an audit. FALSE Professional Skepticism. Although internal auditors are encouraged to use a conversational and participative approach when conducting their reviews, they must also remember that they are tasked with verifying the integrity of the information gathered and make sure their conclusions are sound. An internal control questionnaire (ICQ) helps to evaluate internal controls in specific areas by asking key questions. Verify that user access rights are revoked immediately upon termination. Verify that the controls in place are performing as designed by management Recalculation of Billing amount Verify that employees received the correct payment based on prevailing base and overtime pay rules. FALSE A flowchart is a diagram of the sequence of movements or actions of people or things involved in a process or activity. Fieldwork. This phase is when most of the testing is performed, and it includes interviewing, documenting, applying testing methodologies, managing fieldwork, and providing status updates. Verify that procedures are in place and are working effectively to process incoming customer calls promptly and provide accurate answers to customer inquiries. Compliance issues , can be the result of external quality control initiatives that identify anomalies. FALSE Auditors typically observe conditions and dynamics related to the subject of the review. Trace. This involves tracing a transaction from the source (e.g., a cash receipt, file creation) to its destination, which could be a financial, operational, or regulatory report. Workpapers are documents created by auditors to record the work done. They are a collection of evidentiary material showing the planning done, the fieldwork activities performed, and the support for all information mentioned in the audit report or other communication of results. Documents can be internal or external, financial or nonfinancial, and an auditor may be searching for specific items on the document. TRUE No rules can be established internally (e.g., policies and procedures) or externally (e.g., new or updated laws and regulations), or a combination (e.g., a contract signed by the organization and one or more external parties). FALSE Recalculation/Reperformance Mathematical recalculation is a form of audit evidence and it consists of checking the accuracy of documents or records. Recalculation of depreciation expense confirm the accuracy of the price tables for items sold. In cases where the invoicing is done manually, it is even more important due to the increased possibility of human error. FALSE Cross-foot. Add the items in a row Compliance issues, in the case of regulators and inspector reviews that identify instances of compliance at other organizations, the internal audit department may investigate conditions at their organization. FALSE Reconcile. Tie information from two separate sources to verify the accuracy or expected discrepancies Defining the objectives of any engagement is essential as an initial step to put it on the right footing for success. TRUE Fieldwork is determining if the process or program under review is designed effectively so that the related goals and objectives are likely to be achieved. Document Inspection. This is one of the most common procedures performed by auditors who examine documents to verify the date and amount of transactions, agreements made between various parties, evidence of authorizations and record of decisions made, among others. Efficiencies, waste, rework, or complaints from customers and vendors may trigger management involvement, resulting in their request to have the matter reviewed by internal audit. FALSE Recalculation of overtime hours verify that the assets were classified correctly and the appropriate depreciation schedule applied. FALSE Workpapers should be neat, easy to read, easy to review, and their appearance should be uniform. TRUE After findings are reported, it is incumbent on both management and auditors not to verify that the corrective actions are in fact applied and the problems fixed as expected. FALSE Risk factors play an important role during planning, and in particular, during risk assessments. TRUE In the case of internal audits, anyone being audited may be asked to give testimonial evidence during interviews about a variety of topics. Foot. Add the items in a column. Verify. Confirm, prove, or corroborate that a fact is true Observe /tour. For an area of interest, observe and note physical conditions (e.g., fencing, temperature, cleanliness, and demarcation). Verify that all deposits and withdrawals were recorded in the corresponding GL account, in the correct period, and were authorized by the appropriate manager. Reporting consists of communicating findings, observations, and best practices noted during the review, and developing recommendations for corrective action. Testimonial evidence consists of verbal or written statements or assertions given by someone as proof regarding the matter being discussed. Follow-Up. After findings are reported, it is incumbent on both management and auditors to verify that the corrective actions are in fact applied and the problems fixed as expected.