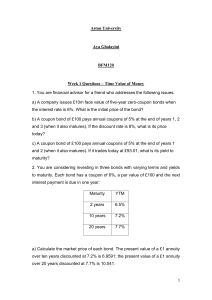

1. Both Bond S and Bond D have 7.3% coupons, make semiannual payments, and are priced at par value. Bond S has three years to maturity, whereas Bond D has 20 years to maturity. If interest rates suddenly rise by 2%, what is the percentage change in the price of the Bond S? of Bond D? What if rates suddenly fall by 2% instead? What dost this problem tell you about the interest rate risk of bonds? 2.