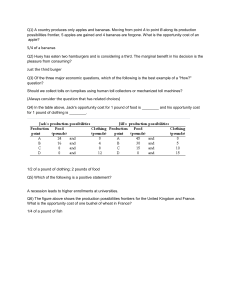

CHAPTER 2 Production possibilities and opportunity cost KEY POINTS • • • • • The three fundamental economic questions Opportunity cost Marginal analysis The production possibilities frontier Present investment and future production possibilities frontier • Gains from trade THE THREE FUNDAMENTAL ECONOMIC QUESTIONS The fundamental economic questions around production are: What? Scarcity imposes restrictions on ability to produce How? What production technique should be used? For whom? Who receives the goods and services that are produced? OPPORTUNITY COST • Because of scarcity, people must make choices, and each choice incurs a cost (sacrifice) known as opportunity cost. • It is the best alternative sacrificed for a chosen alternative. • It applies to personal, group and national decision-making and underpins all aspects of economics, as it is linked closely to scarcity. OPPORTUNITY COST EXAMPLES • What would you be doing if you were not currently studying? • How many new roads have to be forgone if the government spends tax revenues on hospitals? MARGINAL ANALYSIS • Marginal analysis examines the effects of additions to or subtractions from a current situation. • It is a very valuable tool in economics because it considers the effects of change resulting from decision-making. • Individuals, firms and governments all face marginal analysis. MARGINAL ANALYSIS EXAMPLES • Would you devote one extra hour in preparation for economics exam, or nap for an hour? (What is the scarce resource?) • Should the economy allocate more of its resources in producing capital goods or consumer goods? MARGINAL ANALYSIS APPLIED To fertilise or not to fertilise … that is the question … A farmer will only add fertiliser to an area of land if the value of the extra yield exceeds the cost of the fertiliser. Marginal analysis helps decide between options. THE PRODUCTION POSSIBILITIES FRONTIER (PPF) • The economic problem of scarcity means that society’s capacity to produce combinations of goods is constrained by its limited resources. • This condition can be represented in a model called the production possibilities frontier. • The PPF shows the maximum combinations of two outputs that an economy can produce, given its available resources and technology. THE PRODUCTION POSSIBILITIES FRONTIER (PPF) Three basic assumptions underlie the production possibilities frontier model: 1. Fixed resources during the time period: • quantities and qualities of all resource inputs remain unchanged. THE PRODUCTION POSSIBILITIES FRONTIER (PPF) 2. Fully employed resources: • economy operates with all its factors of production fully employed and producing the greatest output possible without waste or mismanagement. 3. Technology unchanged: • Holding existing technology fixed creates limits, or constraints, on the amounts and types of goods and services any economy can produce. THE PRODUCTION POSSIBILITIES FRONTIER (PPF) THE PRODUCTION POSSIBILITIES FRONTIER (PPF) • All the points along the frontier are maximum output levels with the given resources and technology, they are all efficient points. • Points outside the PPF represent unattainable production possibilities, given current resources and technology. • Points inside the PPF represent an inefficient use of current resources. THE LAW OF INCREASING OPPORTUNITY COSTS • Opportunity cost increases as production of one output expands at the expense of another. • This occurs because factors of production are generally not equally suited to producing one good, compared to another good. • That is, opportunity costs rise as resources are shifted away from their best use. THE LAW OF INCREASING OPPORTUNITY COSTS • From Exhibit 2.1, if we wish to move from point A to B (i.e. in order to produce 40 billion units of consumer services), 20 billion units of consumer goods must be forgone. • But to move from point B to C (i.e. to gain another 40 billion units of consumer services), 60 billion units of consumer goods must be forgone. • This rising cost demonstrates the law of increasing opportunity costs. SHIFTING THE PRODUCTION POSSIBILITIES FRONTIER • The PPF can be used to represent changes in the level of technology and available resources. • Economic growth (the ability of an economy to produce greater levels of output) is represented by an outward shift of the production possibilities curve. SHIFTING THE PRODUCTION POSSIBILITIES FRONTIER SHIFTING THE PRODUCTION POSSIBILITIES FRONTIER • Economic growth could be caused by: – Changes in amount of resources: any increase in resources such as natural resources, immigration or more factories. – Technological change: through research and development of new technologies. PRESENT INVESTMENT AND FUTURE POSSIBILITIES FRONTIER • Deciding the output combination of capital and consumer goods now can determine future production capacity. • Countries that forgo current consumption today in favour of investment (producing capital equipment) tend to expand their growth rate: the PPF shifts outward. For example, high levels of positive net investment include Singapore, China and South Korea. PRESENT AND FUTURE PRODUCTION POSSIBILITIES FRONTIER PRESENT AND FUTURE PRODUCTION POSSIBILITIES FRONTIER • Assume Splurgeland spends just enough capital output to replace the capital being worn out each year. • Splurgeland’s PPF remains the same. Why? • To shift its PPF to the right by 2020, Splurgeland would need to sacrifice consumer goods for capital formation, which means that the current standard of living has to fall. PRESENT AND FUTURE PRODUCTION POSSIBILITIES FRONTIER • Assume Thriftyland spends more than enough capital output to replace the capital being worn out each year. • Thriftyland is thus adding to its capital stock and creating extra production. • Thriftyland’s PPF will shift to the right by 2020 and have a higher standard of living than Splurgeland. GAINS FROM TRADE • Individuals and countries should specialise in activities they can efficiently produce and the surplus traded rather than produce everything they need. • By engaging in trade, all parties can benefit from levels of output beyond the confines of their own production possibilities frontiers. • This is known as the theory of comparative advantage. GAINS FROM TRADE Australia specialises in: • extracting minerals • producing wheat and grains • tourism New Zealand • milk production specialises • eco-tourism in: