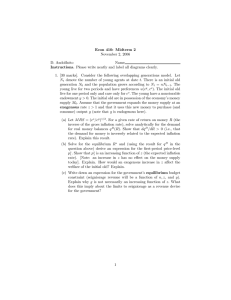

ECO 752: Macroeconomic Theory II Topic 3 1 Inflation, Expectations, Money and Monetary Policy Introduction: The Phillips Curve – short and longrun; Expectations – static, adaptive, rational Definition and Modelling the functions of Money Monetary Policy: Instruments; Targets; Monetary transmission channels Inflation, Money Growth and Interest Rate Seigniorage and Inflation Dynamic inconsistency of inflation Rules vs discretion of monetary policy Stabilization theory and policy 2 The Phillips Curve Theoretical Background and the Short-Run Phillips Curve • Generally, a correspondence one-to-one rise in nominal wage and productivity is not expected to generate rise in price level. However, this condition requires that labour supply curve (workers’ money wage demand) shift upward continuously. • The determination of the movement in money wage rate, W is found in the relationship between the rate of increase in W and the unemployment rate u, that is, the Phillips curve (PC). • From the labour market framework, an increase in the demand for labour – an outward shift in the P.f(N) curve - output (production function), leads to a rise in W, due to presence of excess demand. In figure 4.1 the excess demand is represented by Nd0 – Ns0. 3 W Pe.g(N) W0 P0.f(N) Ns0 Nd0 N Figure 3.1: Excess demand for labour • A basic assumption of the PC is that the rate of increase in money wage rate, W, is dependent on the magnitude of the excess demand for labour, Ns – Nd. That is, W f ( Nd Ns ); • • f ' 0. (3.1) In order to make our analysis simple, the excess demand function is expressed as excess supply, which the inverse of the excess demand. That is, Excess supply = Ns – Nd = - (Nd – Ns) (3.2) 4 • Using the expression for excess supply, the wage adjustment equation (3.1) can be re-written as W f ( N s N d ). (3.3) • Next, unemployment rate u is introduced as a proxy for excess supply. Note that as excess supply rises, the u also rises. • If unemployment rate is substituted for excess supply in equation (3.5), we have W g (u ); • g' 0 (3.4) Since Ẇ falls with an increase in excess supply, it also falls with an increase in u. Therefore, as unemployment rises, the rate of increase of wages falls, and vice versa as unemployment falls. Consequently, (3.4) is the basic short-run PC equation relating Ẇ to u. 5 • As depicted in Figure 3.2, the g(u) function is expected to be convex due to several reasons. First, as unemployment is reduced by constant amounts, the wage rate will rise at an increasing rate, with Ẇ approaching infinity as u approaches 0. This implies that a negative unemployment rate is not observable. Ẇ Figure 4.2: The Phillips curve 0 • u On the other hand, the wage rate cannot continue to fall infinitely, therefore, there must be some institutional lower boundary below which Ẇ cannot fall. Note that it takes time to change wage rates, especially to reduce them, so that Ẇ cannot approach - as unemployment rate grows larger and larger, but rather reaches some stable rate of decrease of wages. 6 • Perry (1966) specified the convexity of the U.S PC by estimating it as W • 1 u The convexity of the PC suggests that, on average, the economy will experience less inflation if the level of unemployment has narrow fluctuations about some average ū than if the fluctuations are wider with the same mean ū. Unemployment and Price Expectations • The PC equation (3.4) is based on two major assumptions: 1) static expectations (money wage does not respond to expectations of price increases; and 2) that there is a direct relationship between changes in W and u. • However, if expectation of economic agents about price changes is introduced, this will yield expectations-augmented PC which can be expressed as e W g (u ) P (3.5) 7 • Equation (3.5) implies that for any specific level of u, the more the rise in expected price, the more will be the rise in W. Short-run Phillips curves Ẇ g(u) + Ṗe1 u g(u) + Ṗe0 The Long-Run PC • This is usually derived by combining the short-run PC with the price changes equation. You are expected to read this up! Branson Chapter 20 8 Expectations in Economics • Generally, expectations affect behavior of economic agents and policy effectiveness – Policy Ineffectiveness Proposition (PIP). • There three types of expectations, each with its own critiques - static, adaptive and rational. Of these three, the two most popular are the Adaptive Expectation (AE) and Rational Expectation (RE). • Adaptive expectations - Use information from the recent past to predict the future of behaviour of variables - Backward looking - Individuals form new expectations by adapting to past mistakes • Rational Expectation - Use all available information that improves the accuracy of a forecast - Forward looking - Pay attention to what is happening in the present and what is likely to happen in the future. For further reading refer to Lecture 1 on ECO 712 9 Definition and Modelling the functions of Money • Money reduces high trading frictions and transaction costs associated with moneyless economy, that is, the barter system. • Although money is generally defined as any legal tender used for payment and settlement of debt purposes, it is best described by the functions it performs in the economy. • Money can be in the form of fiat money, near money, money substitute, inside or outside money • Basic functions of money include medium of exchange, medium (unit) of account, and store of value. • Of all the basic functions of money the only unique role is the medium of exchange function, this is because while some other items/commodities can serve as unit of account and store of value, only money can perfectly act as medium of exchange. 10 Money as medium of exchange • In order to model money as medium of exchange, we built on the BaumolTobin inventory-theoretic model of money demand, by assuming the role of money as a help to “grease the wheel” of the economy by minimising liquidity costs. • Assume an individual agent lives for two periods, 1 and 2, and possesses stocks of bonds (B0) and money (M0) accumulated in the past. The individual has fixed real endowment income in the two periods (Y1 and Y2, respectively) and consumes C1 and C2 respectively. Prices of goods in the two periods are P1 and P2, respectively. The budget identities in the two periods can be represented as P1Y1 M 0 (1 R0 ) B0 P1C1 M 1 B1 , (3.6) P2Y2 M1 (1 R1 )B1 P2C2 M 2 B2 , (3.7) where Ri denotes nominal interest rate on bonds in period i. • The individual is assumed to live for only two periods, but does not exist in period 3, thus, he tries to exhaust all his stock of money and bonds in period 2 (i.e., M2 0 and B2 0. Also, he is not allowed to die indebted nor create money. 11 • The requirements imposed on the agents second period asset holding imply that M2 = B2 = 0. using this, equation (3.6) and (3.7) can be combined to form a consolidated budget constraint: A Y1 • C Rm m0 (1 r0 )b0 C1 2 1 1 , 1 r1 1 R1 Pt (1 Rt ) 1. Pt 1 (3.9) The agent life time utility depends on consumption in the two periods in a separable manner: 1 U (C 2 ), V U (C1 ) 1 • (3.8) where mt is real money balances, bt Bt/Pt is real bonds (or real debt if bt is negative), and rt is the real rate of interest which is defined as rt • P Y2 0 1 r1 P1 (3.10) where > 0 is the pure rate of time preference. The agent chooses the path of C1, C2, and m1 that maximise its utility, subject to the non-negativity constraint imposed on m1 (m1 0) and the initial stocks of money and bonds (m0 and b0). 12 • The Lagrangean associated with the agent’s problem is: C Rm 1 U (C 2 ) A C1 2 1 1 , L U (C1 ) 1 r1 1 R1 1 • (3.11) Differentiating the Lagrangean w.r.t. C1, C2, and m1 yields the following: L U ' (C1 ) 0, C1 (3.12) L 1 U ' (C 2 ) 0 C 2 1 1 r1 (3.13) Rt L m1 1 Rt (3.14) L 0, m1 0, m1 0 m1 • Combination of equations (3.12) - (3.14) yields the usual Euler equation, that is the intertemporal substitution between C1 and C2. This suggests that money does not affect the rate of consumption substitution. • Equation (3.14) on the other hand reflects the impact of nominal interest rate, Rt on the stock of money at a given time. If Rt is strictly positive, Rt > 0, then (-Rt/1+Rt) will be strictly negative, and no money will be held (m1 = 0). On the other hand, if Rt is strictly negative, then money balances will be held indefinitely, that is, m1 → , if R1 < 0. 13 Shopping Costs • The main importance of money as medium of exchange is that it helps in reducing transactions costs. To incorporate this aspect of money into the model, we examine the way by which money affects an individual agent leisure time, following McCallum (1983b, 1989a). • Suppose the agent has a time endowment of unity, works for a fixed amount of units of time, N, and spends St units of time on shopping, this implies that the amount of time available for leisure is (1 – N – St) units. Subsequently, the agent’s utility function can be modified as: 1 U (C 2 ,1 N S 2 ), V U (C1 ,1 N S t ) 1 • 0 And the budget constraint remains as (3.8), however, the agent’s income is now the real labour income, Yt (Wt/Pt)N. the shopping technology takes the form of: 1 N St (mt 1 , Ct ), m (.) 0, mm (.) 0, C (.) 0, CC (.) 0; 0 () (0) 1 N • (3.15) (4.11) The agent’s optimisation is based on the choice of Ct, St (for t = 1, 2), and m1, given the that m1 0. 14 • The Lagrangean for the above problem can be written as: 1 U (C 2 ,1 N S 2 ) L U (C1 ,1 N S1 ) 1 2 C2 Rm A C1 1 1 t [1 N S t (mt 1 , Ct )] 1 r1 1 R1 t 1 • (3.17 ) Differentiating the above w.r.t. C1, C2, S1, S2, and m1 yield the following: L U C (C1 ,1 N S1 ) 1 C (m0 , C1 ) 0, C1 (3.18) L 1 U C (C 2 ,1 N S 2 ) 2 C (m1 , C 2 ) 0 C 2 1 1 r1 (3.19) L U L (C1 ,1 N S1 ) 1 0 S1 (3.20) 1 L U L (C 2 ,1 N S 2 ) 2 0 S 2 1 (3.21) R1 L L 2 m (m1 , C 2 ) 0, m1 0, m1 0 m1 1 R m 1 1 (3.22) where UC(.) and UL(.) denote the marginal utility of consumption and leisure, respectively. 15 • • Equation (3.22) shows that the inclusion of the shopping costs gives rise to additional positive term in the (3.14). Note also that the UL(C2,1-NS2)m(m1,C2)/(1+) represent the marginal utility of money. The marginal utility of money determines the willingness of the individual agent to hold real money balances. Equation (3.22) can be expressed as equality, and 1 and 2 eliminated by combining (3.18) – (3.21). This will result in the following optimality condition: U C (C1 ,1 N S1 ) U L (C1 ,1 N S1 ) C (m0 , C1 ) 1 r1 [U C (C2 ,1 N S 2 ) U L (C2 ,1 N S 2 ) C (m1 , C2 ) 1 U (C ,1 N S 2 ) m (m1 , C2 )(1 R1 ) L 2 (1 ) R1 • (3.23) The lambda, , in (3.23) denotes the marginal utility of wealth. In order to optimise consumption, the agent equates to the net marginal utility of consumption (UC(.)) in the first and second lines of (3.23) minus the disutility arising from additional shopping costs that must be incurred (the UL(.)C(.) term). The third line in (3.23) indicates that marginal utility of money balances (UL(.) m(.)) should be equal to the opportunity costs of holding money. 16 Money as a Store of Value • So far, we have shown that both bonds and money could be used to transfer wealth from one period of time to the other. However, economic agents often prefer to use bonds as store of value because it yields higher returns. • In modelling money as store of value, a model similar to that of Bewley (1980) can be adopted. It is assumed that the agent holds only money stock in which case B0 = B1 = B2 = 0. Thus, the budget constraint can be re-written as: Y1 m0 m1 C1 m1 , Y2 C2 , 1 0 1 1 m1 0 (3.24) where t Pt+1/Pt-1 is the inflation rate. Note that the budget constraint will become a consolidated one similar to (3.8) if m1 is strictly positive. • The agent maximises its utility by choosing the path of C1, C2, and m1. The Lagrange associated with this optimisation problem is: m0 1 U (C 2 ) 1 Y1 L U (C1 ) C1 m1 1 0 1 m1 2 Y2 C2 1 1 (3.25) 17 • • where 1 and 2 are the lagrangean multipliers associated with the two budget constraints. The F.O.C. for the optimisation process yields: L U ' (C1 ) 1 0 C1 (3.26) L 1 U ' (C 2 ) 2 0 C 2 1 (3.27 ) L L 1 2 0, m1 0, m1 0 m1 1 1 m1 (3.28) Combining equations (3.26) – (3.28) gives (1 )U ' (C1 ) L U ' (C 2 ) 1 0 m1 1 1 1 U ' (C 2 ) m1 0, • m1 (3.29) L 0 m1 Equation (3.29) indicates that the agent’s desire to hold stock of money now depends on the inflation and discount rates. 18 • The relationship between the agent’s consumption substitution and the budget line can be represented graphically as follow C2 A EY0 EC EY1 C B Figure 4.1: Money as store of value • C1 On the graph, the agent’s consolidated budget constraint is represented by the AB line and has a slope dC2/dC1 = -1/(1+1). The indifference curve, V0 represents the combination of money stock holdings that maximises utility, and it has aslope of dC2/dC1 = -(1+)U’(C1)/U’(C2), and it is tangential with the budget line at EC. 19 • Point EC represents privately optimal consumption if the non-negativity constraint on money holding is ignored. • If the income endowment point lies north-west of point EC, say at E0Y, money is of no use as a store of value to the agent. In economic terms, the agent would like to be a net supplier of money in order to attain the consumption point EC but this is impossible. • There are two possible solutions (outcomes) from the above, first, since E0Y (the dashed curve) is steeper than the budget line, the choice set is only AE0YC, and the best the agent can do is to consume his endowments in the two periods. Consequently, L/m1 < 0 (lifetime utilities rises by supplying money) and complementary slackness results in m1 =0. • Alternatively, if the income endowment point lies south-east of the consumption point (say at E1Y) the agent saves in the first period by holding money and the first expression in (3.29) holds with equality so that the Euler equation becomes: U ' (C 2 ) (1 )(1 1 ) U ' (C1 ) (3.30) 20 Inflation, Money Growth & Interest Rate Inflation is an increase in the average price of goods and services in terms of money. Recall that from the financial market equilibrium condition real money balances is decreasing in nominal interest rate, i, and increasing in income, Y. That is, M L(i, Y ), P Li 0, LY 0 (3.31) where M is stock of money (money supply) and P is price level. This condition implies that P can be defined as: P M L (i, Y ) (3.32) This shows that an increase in P will occur if there is increase in M and i, a decrease in Y, and a decrease in money demand at a given i and Y. 21 Note that increases (decreases) in i and Y are only short-run phenomena, just as decreases in money demand for a given level of i and Y cannot be sustained over a long period of time. The above situation suggests that sustained increases (changes) in P can only be associated with increases in M. This is established through the quantity theory of money. The relation between growth rate of money and inflation in Nigeria is depicted below 45 40 35 30 25 GRM2 20 Inflation 15 10 5 2003:1 2003:7 2004:1 2004:7 2005:1 2005:7 2006:1 2006:7 2007:1 2007:7 2008:1 2008:7 2009:1 2009:7 2010:1 2010:7 2011:1 2011:7 2012:1 2012:7 2013:1 2013:7 0 Figure 4.2: Growth Rate of Money and Inflation in Nigeria, 2003:1 – 2013:12 22 Money Growth and Interest Rate We begin our analysis of money and interest rate by assuming a long-run situation in which prices are flexible. Also, recall that the neutrality of money in which case money does not affect real economic variables, such real income and real interest rate. This implies that both real interest and income can be held constant, such that r and Y Since, real interest rate is defined as the difference between nominal interest and expected inflation, nominal interest rate can be expressed as: i r e (3.33) Equation (3.33) is know as the Fisher Identity. Given the constancy assumption about r and Y, then the price level, P can be re-written as 23 P M L(r e , Y ) (3.34) Equation (3.34) shows that since r and Y are assumed constant, if M (does not change discontinuously) and P grow at the same rate, such that M/P, then e will be equal to the growth of money. This shows two basic implications. First, the change in inflation resulting from the change in money growth is reflected one-for-one in the nominal interest rate. This hypothesis that inflation affects the nominal rate one-for-one is known as the Fisher effect; it follows from the Fisher identity and the assumption that inflation does not affect the real rate. Second, a higher growth rate of the nominal money stock reduces the real money stock. The rise in money growth increases expected inflation, thereby increasing the nominal interest rate. This increase in the opportunity cost of holding money reduces the quantity of real balances that individuals want to hold. Thus equilibrium requires that P rises more than M. 24 Seigniorage and Inflation • So far, it has been shown that with the introduction of money into the utility function, representative agent can cut through the complexities of the cash-in-advance constraint. • The introduction of money can also be used to examine the relationship between seigniorage, budget deficits, and inflation. • In many countries, the central planner (government) often uses printing or creation of money, or seignniorage, as a means of generating tax revenue. • The use of seigniorage often raises two important questions: 1) how much revenue can government raise from money creation? And 2) can the use of seigniorage to finance too large a budget deficit result in hyperinflation? • To answer these questions, we shall assume that the rate of changes in price level is faster than rate of changes in real variables. Thus, real variables are assumed given. • Further, we assume that two basic things that determine the relation between seigniorage and inflation are the demand for money and expectations about inflation by economic agents (See Cagan, 1956). • The demand for money function by economic agents is given as: m • • * M ce( a ) , P where m is real money balance, c is a constant term, a is elasticity of money demand, and * is expect rate of inflation. The higher the rate of expected inflation, the lower will be demand for real money balanced In equation (3.35) it is assumed that both output and real interest are constant, thus, they are included in c. Expectations about inflation are formed by economic agents through the process of adaptive expectations, in which case expectations of inflation are adjusted according to: d * b( * ) dt • (3.35) (3.36) where b is a coefficient that reflects the speed (rate) at which agents revise their expectations. Note that if current inflation exceeds expected inflation, then expected inflation will increase. This implies that expected inflation depends on past inflation. • Equation (3.36) can be integrated to yield t *t b s e[b ( s t )]ds • (3.37) The dynamics of growth of inflation in the economy is derived through the dynamics of money growth from equations (3.36) and (3.37). Stability of inflation • • Since inflation is generated through the dynamics of money growth, the question to ask is what happens to inflation if money grows at a constant rate? That is, suppose money growth is constant at rate , will inflation converge to or take off on its own toward hyperinflation? To answer the above question take the logarithm equation (3.36) and differentiate. This results in d * dt a • (3.38) If d*/dt is eliminated between equations (3.36) and (3.38), a relation between , *, and can be established as ab( * ) (3.39) • Equation (3.39) shows that whether there will be accelerating inflation depends on a, b in relations to d*/dt on the (, *) space and the effect on the equilibrium. Segniorage and Inflation • • Another question posed by Cagan is if equilibrium is stable, such that given the constant money growth and expectations of inflation, there is no accelerating inflation, how much revenue can be generated by government through seigniorage. In other words, what is the maximum deficit that the government can finance by creation of money? Seigniorage is defined as S • • dM / dt dM / dt M m P M P (3.40) Using equation (3.38) and the fact that in steady state (without growth)* = gives S ce ( a ) This indicates that steady state segniorage is maximized when = 1/a. • In other words, since the elasticity of money demand with respect to inflation is equal to –a, seigniorage is maximized when the elasticity of the tax base m with respect to the tax rate is equal to -1. Read • • • Dynamic inconsistency of low inflation monetary policy Rules vs discretion of monetary policy Stabilization theory and policy Romer chapter 11