Problem Set 2

advertisement

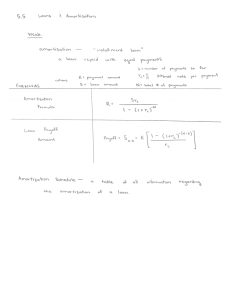

Problem Sets FINA 3770-004 Fall 2004 Problem Set 2 1. Suppose you have received a promise that you will get a series of payments of $500, $400, $600, $700, and $300, spaced a month apart, and starting one month from today. Discounting at 12% APR compounded monthly, calculate the present value of this stream of cash flows. 2. Calculate the future value of the stream of cash flows in problem 1, assuming you invested them at 12% APR compounded monthly (calculate this value as of month 5). 3. Calculate the present value of the series of payments in problem 1, assuming that these are real cash flows, the inflation rate is 3% per year with monthly compounding (0.25% per month) and the nominal rate of return is 12% APR with monthly compounding. (Note: You could either inflate the cash flows, or discount at the real rate, and you would get exactly the same answer either way.) 4. Suppose you paid $400 in exchange for a promise that you will get a series of payments of $110, $121, $133.10, and $146.41, spaced a year apart, and starting one year from today. Calculate the annually compounded rate of return implied by this stream of cash flows. 5. What is the present value of $1,000 to be received annually for 10 years, if interest of 10% can be earned? 6. If you invest $1,000 per year at 10%, how much will you have after 10 years? 7. If you invest $100 per month at 12% interest compounded monthly, how much will you have after 5 years? 8. Suppose you want to withdraw $1,000 per year for 4 years from a bank account, so that there will be nothing left at the end. How much must you deposit, at 6% compounded annually? 9. You want to buy a $90,000 house and have $20,000 for the down payment. If you can get a mortgage at 12% (compounded monthly) for 30 years, what will your monthly payments be? 10. Suppose you have $25,000 for a down payment and can afford $900 per month for house payments. What price can you afford to pay for a house if you can get a mortgage at 12% (compounded monthly) for 30 years? 11. Adam Smith took out a 30 year mortgage and after paying the various fees actually received $95,000. The payments will be $1,126 per month. What rate of interest is implied, stated as an APR with monthly compounding? 12. Your insurance company has offered you the convenience of making monthly premium installments, instead of paying your premium annually in advance. Your next annual premium is due September 28th. You could pay $200 then and be done with it for another year, or make the first monthly installment of $19. The remaining 11 installments would be due monthly on the 28th. If you choose the monthly payments, you will in effect be borrowing money from the insurance company. What interest rate would you be paying, stated as an APR with monthly compounding? 13. Your insurance company has offered you the convenience of making monthly premium installments, instead of paying your premium annually in advance. Your next annual premium is due September 28th. You could pay $200 then and be done with it for another year, or choose monthly installment of $19. The first payment would be due October 28th, and the remaining 11 installments would be due monthly on the 28th. If you choose the monthly payments, you will in effect be borrowing money from the insurance company. What interest rate would you be paying, stated as an APR with monthly compounding? 14. Suppose you saved $1000 each year for 5 years and invested it at 8% compounded annually, starting October 1, 1999. How much would you have on October 1, 2004? 15. Suppose you invested $1000 on today’s date in 1999 and repeated the investment annually for a total of five such installments. How much would you have on today’s date in 2004, if you earned 12% APR with annual compounding? 16. Suppose you invested $1000 on today’s date in the year 2000 and repeated the investment annually for a total of five such installments. How much would you have on today’s date in 2004, if you earned 12% APR with annual compounding? page 1 Problem Sets FINA 3770-004 Fall 2004 17. Robert Anderson wants to retire right away, and would like to set aside enough from the advance on his latest book to give himself an income of $3,000 per month for 25 years. He also would like to be able to give himself monthly cost of living increases to keep up with inflation. He expects inflation to average 6% compounded monthly (0.5% per month), and he can earn a nominal rate of return of 12% with monthly compounding. How much will his retirement annuity cost? 18. A car costs $9,863.69 and will last 5 years with no salvage value. If you could earn 8% compounded monthly by investing the money, what is the opportunity cost per month of the car's life? Opportunity cost refers to the value of the next best alternative use of the money, which in this case you can assume is to provide a monthly annuity for 5 years. 19. If the car cost $11,206.11 and was expected to have a salvage value of $2,000 at the end of a five-year life, what would the opportunity cost be (if money earns 8% compounded monthly)? 20. Suppose your company is considering buying a machine that costs $2,000,000 and is expected to have a $200,000 salvage value at the end of a 7-year life. The opportunity cost of capital is 12% APR (with monthly compounding). How much per month must be saved, at minimum, in order to justify the expenditure? 21. A business term loan has annual payments of $100,000 for 5 years at 10% APR. Assuming it is an ordinary annuity, calculate the present value (the principal) of the loan, and then construct an amortization table showing a breakdown of the payments into principal and interest, as well as the remaining balance after each payment. 22. For the loan in the previous problem, calculate the annual payments after tax. For this calculation assume that the interest payments are immediately deductible as soon as they are made, and that the corporate income tax rate is 34%. When you are finished with the after-tax payment schedule, use the cash flow mode to calculate the after-tax interest rate paid on this loan. 23. Samantha and Peter Braumeister bought a new house recently. They took out a mortgage with $100,000 principal, 30 years of monthly payments, and a fixed rate of 10.2% APR with monthly compounding. They made the first payment on July 1, and it is now time to figure their income tax for the year. How much interest would they pay on their home mortgage for the payments made from July through December? 24. Suppose you have received a promise that you will get a series of payments of $400, $400, $500, $500, $600, $600, and $600, spaced a month apart, and starting one month from today. Discounting at 12% compounded monthly, calculate the present value of this stream of cash flows. 25. Suppose you have inherited some money and want to establish a fund for educating your young child. You think you will need to be able to withdraw $10,000 per year for 4 years, starting in 17 years (withdrawals in years 17, 18, 19, and 20). How much must you put in the fund now, if you can earn 10% compounded annually? 26. An investment opportunity offers a stream of payments amounting to $100,000 per year for five years. The payments will be spread continuously over the life of the investment, rather than arriving at discrete intervals. Discounting at 10% compounded continuously, calculate the present value. 27. An investment opportunity offers a stream of payments amounting to $10,000 per year for ten years. The payments will be spread continuously over the life of the investment, rather than arriving at discrete intervals. Discounting at 8% compounded continuously, calculate the present value. 28. Arthur Anderson wants to retire in 15 years, and would like to put aside enough to give himself an income of $25,000 per year for 25 years after retirement. If he can earn 10% compounded annually over the whole timespan and saves an equal amount each year, how much must he set aside annually from now until retirement? Assume all cash flows fall at the end of the year. page 2 FINA 3770-004 SOLUTIONS: PROBLEM SET 2 Fall 2004 1. Use Cash Flow Mode. Data inputs: Initial Cash 9. Flow is 0, CF1 is 500, CF2 is 400, CF3 is 600, CF4 is 700, CF5 is 300. Frequencies are all 1. %I is 1 (because payments are monthly, so you must use the monthly rate). Compute NPV. Result is $2,427.65 You need to borrow $70,000, so the data input proceeds as follows: PV is 70000, I/YR is 12, P/YR is 12, N is 360, Mode is END. Compute PMT. Result is $720.03. If it is not crystal clear whether the payments are at the end of the period, by default we treat it as an ordinary annuity. 2. HP-17 and HP-19 have an “NFV” key you can use 10. for this. If your calculator doesn’t have this feature, then enter the answer from the previous problem as PV, N is 5, I/YR is 12, P/YR is 12, PMT is 0. Calculate FV. The result is $2,551.48 3. Repeat the calculation in problem 1, but use the real rate per month. The real rate is (1%0.25%)/1.0025. Calculate this and enter it directly into interest without rounding. The answer is $2,445.57 The first step is to find out how much you can borrow, so the data input proceeds as follows: FV is 0, PMT is –900 I/YR is 12, P/YR is 12, N is 360, Mode is END. Compute PV. Intermediate result is $87,496.50. Next, be sure the sign in the display is positive, then add the $25,000 down payment. The final result is that you can afford to pay $112,496.50. Normally, mortgage loans have the payments at the end of the period, so we treat them as ordinary annuities. 4. 5. 11. Use cash flow mode. Then the initial cash flow is –400. Cash flows 1 through 4 are 110, 121, 133.10, and 146.41, each with frequency of 1. Next, calculate IRR. Result is 10% 12. Data input: PMT is 1000, N is 10, P/YR is 1, I/YR is 10, FV is 0, Mode is END. Compute PV. Result is $6,144.57. If it is not crystal clear whether the payments are at the end of the period, by default we treat it as an ordinary annuity. The 13. neegative sign in the PV display is due to the sign convention. 6. Data input: PMT is –1000, N is 10, P/YR is 1, 14. I/YR is 10, PV is 0, Mode is END. Compute FV. Result is $15,937.42. If it is not crystal clear whether the payments are at the end of the period, by default we treat it as an ordinary annuity. 7. Data input: PMT is –100, N is 60, P/YR is 12, I/YR is 12, PV is 0, Mode is END. Compute FV. 15. Result is $8,166.97. If it is not crystal clear whether the payments are at the end of the period, by default we treat it as an ordinary annuity. 8. Data input: PMT is 1000, N is 4, P/YR is 1, I/YR is 6, FV is 0, Mode is END. Compute PV. Result is $3,465.11. If it is not crystal clear whether the 16. payments are at the end of the period, by default we treat it as an ordinary annuity. The neegative sign in the PV display indicates that an outflow would occur in the present. Data input: PV is 95000, PMT is –1126, N is 360, P/YR is 12, FV is 0, Mode is END. Compute I/YR. Result is 14%. Data input: PV is 200, PMT is –19, N is 12, P/YR is 12, FV is 0, Mode is BEG. Compute I/YR. Result is 29.73% (Note: This is an annuity due, because payments are clearly at the beginning of the period.) This is the same as the previous problem in every way except that it is an ordinary annuity Mode is END. The APR is 24.91% Data input: PMT is –1000, N is 5, P/YR is 1, I/YR is 8, PV is 0, Mode is BEG. Compute FV. Result is $6,335.93. Since the payments are at the begining of the period, it is an annuity due (the last payment comes into account one period before the future value). Data input: PMT is –1000, N is 5, P/YR is 1, I/YR is 12, PV is 0, Mode is BEG. Compute FV. Result is $7,115.19. Since the payments are at the begining of the period, it is an annuity due (the last payment comes into account one period before the future value) This is the same as the previous problem in every way except that it is an ordinary annuity. Mode is END. Calculate FV. Result is $6,352.85 Page 1 of 2 FINA 3770-004 17. 18. 19. SOLUTIONS: PROBLEM SET 2 Fall 2004 The key to an efficient calculation is the annual 24. real rate. So first find r = (12% – 6%) / 1.005 and input it directly as I/YR (the result is approximately 5.97%). Alternatively, one could calculate the real rate per month and then multiply times twelve. Other data inputs: PMT is 3000, N is 300, P/YR is 12, FV is 0. Mode is END. Compute PV. Result is $466,942.12. If it is not 25. crystal clear whether the payments are at the end of the period, by default we treat it as an ordinary annuity. The negative sign in the PV display indicates that an outflow would occur in the present. 26. PV is 9863.69, FV is 0, P/YR is 12, N is 60, mode is END, calculate PMT. The result shows that the opportunity cost of the car is $200 per month Use Cash Flow Mode. Data inputs: Initial Cash Flow is 0, CF1 is 400 with frequency 2, CF2 is 500 with frequency 2, CF3 is 600 with frequency 3. %I is 1 (because payments are monthly, so you must use the monthly rate). Compute NPV. Result is $3,449.68 PV is 11206.11, FV is 2000, P/YR is 12, N is 60, mode is end, calculate PMT. The result shows that the opportunity cost of the car is $200 per month È 1- e - (.08¥1 0) ˘ PV = ($10, 000 ¥ 10 )Í Î .08 ¥ 10 ˙˚ PV = $68,833.88 20. PV is –20,000,000, FV is 200,000, N is 84, interest per year is 12, calculate PMT. Answer is $33,774.92 21. PV = $379,078.68 Amortization Table n Interest Principal Balance 1 37,907.87 62,092.13 316,986.55 2 31,698.66 68,301.34 248,685.21 3 24,868.52 75,131.48 173,553.73 4 17,355.37 82,644.63 90,909.10 5 9,090.91 90,909.09 0 22. After-Tax Amortization Table After-tax n Interest Principal 1 25,019.19 62,092.13 2 20,291.12 68,301.34 3 16,413.22 75,131.48 4 11,454.54 82,644.63 5 6,000.00 90,909.09 27. 28. Use Cash Flow Mode. Data inputs: Initial Cash Flow is 0, CF1 is 0 with frequency 16, CF2 is 10000 with frequency 4, %I is 10, compute NPV. Result is $6,898.55 È 1 - e -( .1¥5 ) ˘ PV = ($100, 000 ¥ 5)Í Î .1 ¥ 5 ˙˚ PV = $393,469.34 First, find the present value of Arthur’s desired retirement annuity at the time of his retirement (this is the goal of the savings plan). For this step PMT is 25000, FV is 0, P/YR is 1, I/YR is 10, mode is end, calculate PV (the result is $226,926). Now with this result in the calculator display, make sure the sign is positive. Then input it as FV for the next step. Then PV is 0, N is 15,and all other settings remain the same. Calculate PMT. The result shows that Arthur must save $7,142.22 per year in order to meet the goal. After-tax Payment 87,111.32 89,222.46 91,544.70 94,099.17 96,909.09 After-tax interest rate = 6.60% 23. Interest for the first six payments totals $5,094.54. Page 2 of 2