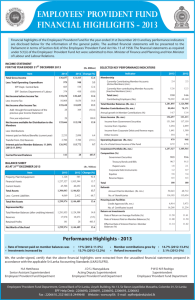

HANDBOOK OF EMPLOYEES` PROVIDENT FUND

advertisement