Chapter 5

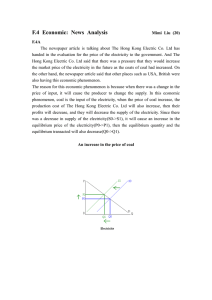

advertisement