Peaks, Valleys, and Points of View

advertisement

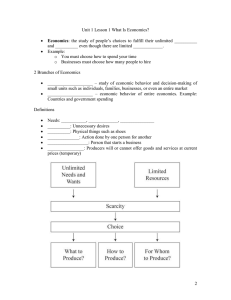

Peaks, Valleys, and Points of View But once the frog and fly populations start doing their stuff to each other, once the fitness landscape of each begins to deform as the other population moves on its own landscape, all bets are off. Neither population may ever come to rest on fitness peaks, for those peaks themselves may keep moving, and the adapting population may keep chasing peaks that forever elude them. Coevolving systems, thus, do not have a potential function. Mathematicians recognize such coevolving systems as general, complex, dynamical systems. Stuart Kauffman. At Home in the Universe. The Oxford University Press 1995, p. 222) So what if our dialogs reflect coevolving systems? And our peaks and valleys are flipped? …by the invisible hand? … about every 10 years. A painting of economic history • Visit: • http://www.google.com/imgres?q=mark+tansey+ec+101&um =1&hl=en&sa=N&biw=1366&bih=673&tbm=isch&tbnid=sgxlG xcH5sl0M:&imgrefurl=http://anticap.wordpress.com/2010/04 /18/ec-101/&docid=7Z2CorjWFhKVM&imgurl=http://anticap.files.wordpress.com/2 010/04/5534431.jpg&w=382&h=480&ei=d75PT7zlDdKqsAKL2 _S1Dg&zoom=1&iact=hc&vpx=180&vpy=130&dur=2555&hov h=252&hovw=200&tx=123&ty=180&sig=10112665443348838 3279&page=1&tbnh=158&tbnw=124&start=0&ndsp=19&ved =1t:429,r:0,s:0 Same sizex larger), 89KB •More sizes •Search by image •Similar images Images may be subject to copyright. •482 × 298 ( Same sizex larger), 89KB •More sizes •Search by image •Similar images Images may be subject to copyright. •482 × 298 ( FLIPPABLE ECONOMICS Economic “Science” is completely flippable on the basis of the latest Experience. The painting starts with the believers in laissez-faire right side up, but 2008 turns the economy, the painting, and the laissez-faire economists upside down. In fact the painting captures the precise moment when the head of the Fed (Greenspan) and the President of the United State (Bush) find their laissez-faire policy achieving the greatest intervention by the government (partial nationalization of GM, Chrysler, AIG, and the major banks) of all time. So upside down, they are almost totally right side up. Presto! Flippable chief executives who, when you hear what they do- not what they say-are pro-government interventionists. They are flipped by the cascading economy represented by the avalanche off of the mountain, K-10. Flipped, they now have to ascend the greater heights. The diminishing returns guaranteeing the stability of their equilibrium in the laissez-faire has become the increasing returns of creatively destroyed equilibrium faced by the interventionists. With the flip of a picture the convexity of the avalanche becomes concavity, and concavity becomes convexity. The painting has a flippable timedimension shown vertically above. 1. The Laissez-Faire economists are shown from earliest (top) to latest (center) 2. while the Interventionists are shown earliest (bottom) to latest (center). When the painting is flipped vertically, the only thing that has changed is who is on top; time still passes as we move visually to the center of the painting. Physiocrats Classical Economics: Austrian Economics NeoClassical Economics 1. Laissez-Faire ideologues: Chicago School Microecon omics Macroecon omics 3rd generation: Great Society: New Deal: KEYNES Industrial Organization Institutionalism 2. Socialism Malthus Colbert Communism Macroeconomics (left) vs. Microeconomics (right): Macroeconomics looks at Classical Economics: the overall economy from the point of view of a planner. Microeconomics looks at an individual household or firm from the point of the individual who NeoClassical runs that unit. The Laissezfaire economists are almost Economics invisible on the macroeconomic side because they don’t like Chicago School planning for the economy, and after the crash of 2008, the credibility of laissez-faire to achieve stable equilibrium is gone (as suggested by the avalanche in the painting) Physiocrats Austrian Economics Laissez-Faire ideologues: Microecon omics Macroecon omics 3rd generation: Great Society: New Deal: KEYNES Industrial Organization Institutionalism Malthus Colbert Communism Macroeconomics and microeconomics are flippable. When the painting is upside down, Upside down the painting is about actual government intervention. the communists- the ultimate micro-managers- become the ultimate planners of the Socialism macro economy. And the New Deal-Great Society-3rd generation Keynesians become the micro managers of the safety net for dependents. Those in the center of the painting dance either way. Meanwhile the Laissez-faire theoreticians, having nothing to say theoretically about planning at the macroeconomic level, have nothing to provide dependents at the microeconomic level when the economy fails. 2.Beginning with Colbert, who experiments with government taxation and regulation, a dialog is set up between those (Colbert, Socialism, Communism, Institutionalism, Industrial Organization, Heterodox) who believe in government intervention and those who belief in laissez-faire (Physiocrats, Calssical Economics, Neoclassical, Chicago School, Austrian, Laissez Faire) . Austrian Economics NeoClassical Economics 2. Chicago School Macroecon omics 3rd generation: Great Society: New Deal: KEYNES Physiocrats Classical Economics: Laissez-Faire ideologues: Microecon omics 1. Industrial Organization Communism Institutionalism Socialism Malthus Colbert 3.The Physiocrats are highly critical of Colbert’s interventionist policies and create a political counter to those policies Physiocrats Classical Economics: Austrian Economics NeoClassical Economics 2. Chicago School Laissez-Faire ideologues: 3. Macroecon omics 3rd generation: Great Society: New Deal: KEYNES Microecon omics 1. Industrial Organization Communism Institutionalism Socialism Malthus Colbert 4.Adam Smith visits France and picks up many ideas from the Physiocrats Physiocrats Classical Economics: 4. Austrian Economics NeoClassical Economics 2. Chicago School Laissez-Faire ideologues: 3. Macroecon omics 3rd generation: Great Society: New Deal: KEYNES Microecon omics 1. Industrial Organization Communism Institutionalism Socialism Malthus Colbert 5.The NeoClassical economists synthesize and mathematicize the ideas of the Classical Economists to produce the supply and demand tools still used today. But they add concepts of equilbrium, marginalism, and factor shares which raise normative questions. Physiocrats Classical Economics: 4. 5. Austrian Economics NeoClassical Economics 2. Chicago School Laissez-Faire ideologues: 3. Macroecon omics 3rd generation: Great Society: New Deal: KEYNES Microecon omics 1. Industrial Organization Communism Institutionalism Socialism Malthus Colbert 6.Meanwhile, the French Revolution wipes out the monarchy and hatches the first socialist experiments with community decision-making. There is deep suspicion of markets because the ill effects of competition and industrialization have made themselves felt. Labor feels it is being cheated of the surplus from its labor by the capitalists. Physiocrats Classical Economics: 4. 5. Austrian Economics NeoClassical Economics 2. Chicago School Laissez-Faire ideologues: 3. Macroecon omics 3rd generation: Great Society: New Deal: KEYNES Microecon omics 1. Industrial Organization Communism Institutionalism Socialism 6. Malthus Colbert 7.The Communists wish to take socialism to the extreme of allowing no private property. The state owns everything and the capitalists are weeded out. The state plans everything. Physiocrats Classical Economics: 4. 5. Austrian Economics NeoClassical Economics 2. Chicago School Laissez-Faire ideologues: 3. Macroecon omics 3rd generation: Great Society: New Deal: KEYNES Microecon omics 1. Industrial Organization Communism Institutionalism Socialism 6. Malthus Colbert 7. 8a-d. Clark and his son make the transition from German socialism to Neoclassical economics to Institutionalism to Heterodox Economics. Clark rejects the redistribution of property by the socialists. While making important contributions to the Neoclassical schools, he realizes the problems of monopoly and writes a report which provides the foundation for setting up one of the key U.S. antitrust agencies, the FTC. Macroecon omics 3rd generation: Great Society: New Deal: KEYNES Physiocrats Classical Economics: 4. 5. Austrian Economics NeoClassical Economics 2. Chicago School Laissez-Faire ideologues: 8a. 3. 8b. Microecon omics 1. Industrial Organization 8c. Institutionalism Socialism 6. Malthus Colbert Communism 7. His son goes beyond the Institutionalist school by criticizing the excesses of the orthodox neoclassical conception of markets. Others will travel between schools, although not quite as dramatically as the Clarks. Repelled by the Socilaists (9a) and the Communists (9b), the Austrian School develops theories of economic rationality, human action, and acquisition of information to counter the economic thinking of the interventionists. While they support the laissez-faire conclusions of Neoclassical economics, they are also quite critical of the mathematicization and the model of economic rationality used by the Neoclassical economists (9c). Macroecon omics 3rd generation: Great Society: New Deal: KEYNES Physiocrats Classical Economics: 4. 5. Austrian Economics 9c. NeoClassical Economics 2. Chicago School Laissez-Faire ideologues: 3. 8a. 9a. 9b. 8b. Microecon omics 1. Industrial Organization 8c. Communism Institutionalism Socialism 6. Malthus Colbert 7. 10.Laissez-faire economists often pay little attention to the theoretic economic root of the arguments for depending on markets, and make the desirability of markets simply a given- a religion. The fervent belief in markets provides an ideological counterweight to the Soviet Union during the Cold War, but leads to massive defense expenditures which leads to even more massive government. Practicing laissezfaire capitalism becomes an rd oxymoron 3 generation: Macroecon omics Great Society: New Deal: KEYNES Physiocrats Classical Economics: 4. 5. Austrian Economics 9c. NeoClassical Economics 2. Chicago School 8a. Laissez-Faire ideologues: 10. 3. 9a. 9b. 8b. Microecon omics 1. Industrial Organization 8c. Communism Institutionalism Socialism 6. Malthus Colbert 7. Physiocrats Classical Economics: 4. 5. 2. Chicago School 8a. Macroecon omics 3rd generation: Great Society: New Deal: KEYNES Austrian Economics 9c. NeoClassical Economics Laissez-Faire ideologues: 10. 3. 9a. 9b. 8b. Microecon omics 1. Industrial Organization 8c. Communism Institutionalism Socialism 6. Malthus Colbert 7. Painting Placement Economics grows out of key face-offs among economists. Some of these face-offs occur among economists on the same side- and so they are shown proximate to each other (with two way arrows). Some of these face-offs occur between teacher and pupil- and these are shown proximate to each other with the teacher vertically further back in time (and the arrow points to the student). But some are across the interventionist-laissez faire divide with vertical placement (and two way arrows). Generally, the faceoff is over specific issues. There are also some contrasts and parallels where no face-off occurred, but wouldn’t it be great if they had?! Molina Contrasts and Parallels Classical Economics: NeoClassical Economics Yunnus Laffer Hume Law Physiocrats Adam Smith Bentham Say Mill Ricardo Marshall Walras Clark Kaldor Chicago School Bohm Bawerk Austrian von Mises Economics Hayek Friedman Shultz Reagan Bush Cheney generation: Reich Stiglitz Rivlin Tyson Great Society: Solow Okun New Deal: Berle KEYNES Ayn Rand Buchanan Tullock Kornai Greenspan Laissez-Faire ideologues: Macroecon omics 3rd Heterodox Industrial Organization Mueller Galbraith Bain Institutionalism Commons Veblen Ward Socialism Malthus Turgot Vaubon Quesnay Condorcet Colbert Microecon omics Bowles Arrow Habermas Schumpeter Kondratiev Communism Mao Tse-Tung Stalin Lenin Marx Fourier Owen Proudhon St. Simon Rousseau Major Face-offs The face-offs occur over specific issues. The issues examined here are: •Will Capitalism work? •Does the market automatically eliminate shortages and surpluses (gluts)? •Is government intervention needed? •Is there a “public good”? •How does money affect income? Even though Economists want to be scientists many of them are still playing childhood games of good-guys and bad-guys; before science is ever applied, their results are predictable. Some of the bad guys make fun reading. Will capitalism work? Classical Economists: Capitalism produces the technological change that saves the economy from the dismal predictions of Malthus. Socialists: Abolish the excesses of Capitalism. Come up with creative experiments to use markets to socialist ends. Eliminate the capitalists’ ill-gotten gains; that’s the reason for the government or a community to takeover the decisions and returns from owning capital. Marx: There are clear historical stages of progress from a mediaeval to a capitalist to a communist economic system. His progression has an Hegelian inevitability to it. Applied Communism (Mao, Stalin, Lenin): We can jump from the agricultural stage to Communism, by suppressing Capitalism and never let it raise its ugly head (but degrees of private ownership creep into their experiments: Russia experiences one of the great privatizations of all time). Kondratiev: Capitalism faces a 150 year cycle, marked initially by fast growth, but inevitably a slow down and collapse. Keynes: Capitalism can work if government can bail it out when necessary. Schumpeter: Capitalism is saved by its ability continually to creatively destroy itself. It is always tearing down its own institutions through its inventions, innovations, and diffusion of technological change. On the other hand the technocrats may gain enough control to stifle this creative force, erect a welfare state which leads to the atrophy and destruction of an economy. Ayn Rand: Capitalism is the only thing that works, but it doesn’t work if government interferes. Industrial Organization: Capitalism can work with regulation, taxation/subsidy, antitrust, and formal industrial policy. Kornai: Totalitarian government doesn’t work. Capitalism is the default. Habermas: Late Capitalism destroys the Enlightenment’s dream of a rational human being through institutions which illuminate discourse. Molina Hume Classical Economics: Shortages & Surpluses? Malthus sets the stage NeoClassical Economics Yunnus Laffer Law Physiocrats Adam Smith Bentham Say Mill Ricardo Marshall Walras Clark Kaldor Chicago School Bohm Bawerk Austrian von Mises Economics Hayek Friedman Shultz Reagan Bush Cheney Laissez-Faire ideologues: Ayn Rand Buchanan Tullock Kornai Greenspan Microecon omics Macroecon omics 3rd generation: Reich Stiglitz Rivlin Tyson Great Society: Solow Okun New Deal: Berle KEYNES Turgot Vaubon Quesnay Condorcet Heterodox Industrial Organization Mueller Galbraith Bain Institutionalism Commons Veblen Ward Socialism Malthus Colbert Bowles Arrow Habermas Schumpeter Kondratiev Communism Mao Tse-Tung Stalin Lenin Marx Fourier Owen Proudhon St. Simon Rousseau Molina Shortages & Surpluses? Say’s Law Classical Economics: NeoClassical Economics Yunnus Laffer Hume Law Physiocrats Adam Smith Bentham Say Mill Ricardo Marshall Walras Clark Kaldor Chicago School Bohm Bawerk Austrian von Mises Economics Hayek Friedman Shultz Reagan Bush Cheney Laissez-Faire ideologues: Ayn Rand Buchanan Tullock Kornai Greenspan Microecon omics Macroecon omics 3rd generation: Reich Stiglitz Rivlin Tyson Great Society: Solow Okun New Deal: Berle KEYNES Turgot Vaubon Quesnay Condorcet Heterodox Industrial Organization Mueller Galbraith Bain Institutionalism Commons Veblen Ward Socialism Malthus Colbert Bowles Arrow Habermas Schumpeter Kondratiev Communism Mao Tse-Tung Stalin Lenin Marx Fourier Owen Proudhon St. Simon Rousseau Molina Shortages & Surpluses? Classical Economics: NeoClassical Economics Yunnus Laffer Hume Law Physiocrats Adam Smith Bentham Say Mill Ricardo Marshall Walras Clark Kaldor Chicago School Bohm Bawerk Austrian von Mises Economics Hayek Friedman Shultz Reagan Bush Cheney generation: Reich Stiglitz Rivlin Tyson Great Society: Solow Okun New Deal: Berle KEYNES Ayn Rand Buchanan Tullock Kornai Greenspan Laissez-Faire ideologues: Macroecon omics 3rd Heterodox Industrial Organization Mueller Galbraith Bain Institutionalism Commons Veblen Ward Socialism Malthus Turgot Vaubon Quesnay Condorcet Colbert Microecon omics Bowles Arrow Habermas Schumpeter Kondratiev Communism Mao Tse-Tung Stalin Lenin Marx Fourier Owen Proudhon St. Simon Rousseau IS GOVERNMENT INTERVENTION NEEDED? 1.Colbert (the government intervention solution): Forced to finance the Napoleonic Wars, Colbert creatively finds ways to stimulate French manufacturing industries through subsidies and to impose protectionism against foreign imports. He also finds ways to tax more efficiently. 2.Law (the private sector solution): Saddled with enormous debt Louis XIV employs a Scot to set up foreign projects, allow private stock to be sold in those projects on the basis of their expected future income, allow the exchange of that stock for government debt, and … voila… debt paid! But the economy comes crashing down when people no longer expect the foreign projects to generate income. Problem! 3.And a problem that resurfaces about every ten years thereafter right up to 2008, forcing the government to intervene even more or to face revolution (Louis XVI). Like Law, Alan Greenspan wants to take the laissez-faire approach, but finds the market to crash beneath him. 4a.Like Louis XIV, President Bush finds that he needs to intervene with more government when the market crashes so that he becomes the ironic victim of the laissez-faire approach. 4b.Like Louis XVI, President Bush is beheaded with his whole party. 5.The Physiocrats. In reaction against Colbert, the Physiocrats argue that the government intervention actually makes the economy more inefficient. They fight the protectionist, regulatory, and taxation schemes with the cry “laissez faire.” 6a.Suppose communities (women, indians, martians) are not powerful enough to protect themselves, does human nature protect such communities? Plato raises the question in the Myth of Gyges- Gyges who does evil once he has a cloak of invisibility. Is there anything in the market that protects such communities? 6b.AdamSmith: The invisible hand works through competition to achieve desirable outcomes for markets He popularizes the Physiocrat’s point of view. Nevertheless he justifies government regulation of monopoly. 7.Ricardo. Free trade allows everyone to gain by specializing in what they have a comparative advantage in producing and therefore the trade protectionism should be eliminated. Government taxation and intervention should be kept to a minimum. 8.Socialism. Government planning and ownership can provide a means for achieving the best market outcomes while still achieving valuable public outcomes that a flawed market can never achieve. 9.Communism.Markets always fail and sacrifice the worker. The government should own the means of production. People should be able to work according to their ability and consume according to their needs. 10. Hayek. The market efficiently allows the exchange of information necessary to determine the prices necessary for the market to achieve efficient outcomes. Inserting a 3rd party between every communication only serves to make communication impossible. The volume of information needed is beyond the possibility of any central authority ever to process the information needed for the efficient exchange of goods and services. 11.Kornai. Totalitarian government results in a chronic shortage economy. IS GOVERNMENT INTERVENTION NEEDED? (CONTINUED) 12.Ayn Rand and the Laissez-Faire clan. Government cannot be trusted and should not be used. Only individual enterprise can be relied upon to be productive. Government intervention limits the creativity and abilities of free enterprise. Survival of the fittest means the weak should be allowed to fail. If the weak are preserved our strong are weakened. 13.The wrecking crew: Dismantle government agencies. If that can’t be done, subcontract the work to the private sector. If that can’t be done, underfund them through prioritization at the Office of Management and Budget. If that can’t be done, don’t allow them to employ anyone. If that can’t be done, detail deadwood from other agencies. If that can’t be done, don’t appoint an agency head. If that can’t be done, appoint a dependable anti-government head of the agency. In any event don’t let an agency write its own history, control its public relations, or keep documentation sitting around. And if you can’t cut it back, feed the beast until it blows itself up. It’s guerilla warfare to keep down big government, even if you have to increase big government to do it. 14.Keynes,. When there isn’t enough demand and prices don’t eliminate the surplus, government may have to intervene with greater demand to stabilize the economy. 15a. Laffer. Government stifles growth. Rather than stabilizing the economy through demand side policies, supply side policies should enhance the availability of resources. 15b. The wrecking Crew 2: Yes, whenever we get into office, let’s loot the government of any stockpiled commodities it owns, dump them on the economy, and curb inflation (and by the way, use the proceeds to balance the budget!). 16. The rest of the conservative macroeconomists- gone due to the 2008 avalanche pictured. 17. The New Deal, the Great Society, and the 3rd generation. Keynes reaffirmed. Infrastructure investment becomes the optimal public investment. The government must take over when the private sector fails. 16. Institutionalism. When the market fails to take care of the weak, government must provide a safety net. Government also takes the responsibility for regulating the private sector. 17. Industrial Organization. Isn’t it time that someone measured whether or not markets work, whether there is something called market power, and what the impact of government policy is? By the way, watch out that government isn’t taken over by the private sector! The government should plan with a systematic industrial policy, rather than defaulting to capture of government by powerful private interests. 18.Friedman. Government should not be in the business of choosing winners or losers. It should be limited in its powers so that it cannot be taken over by private interests. Exit (in other words, bankruptcy and liquidation) is the way markets preserve the most efficient firms. Without exit there are barriers to entry to efficient firms gaining enough of the market to survive. We should have let Chrysler fail in 1978, rather than bailing it out, because in 2008, we have to bail it out again! Molina Hume Classical Economics: NeoClassical Economics Yunnus Laffer Law Physiocrats Adam Smith Bentham Say Mill Ricardo Marshall Walras Clark Kaldor Chicago School Turgot Vaubon Quesnay Condorcet Bohm Bawerk Austrian von Mises Economics Hayek Laissez-Faire: Friedman Shultz Reagan Bush Cheney Ayn Rand Buchanan Tullock Kornai Greenspan Microecon omics Macroecon omics 3rd generation: Reich Stiglitz Rivlin Tyson Great Society: Solow Okun New Deal: Berle KEYNES Industrial Organization Mueller Galbraith Bain Institutionalism Commons Veblen Ward Socialism Malthus Colbert Heterodox Bowles Arrow Habermas Communism Mao Tse-Tung Stalin Lenin Marx Fourier Owen Proudhon St. Simon Rousseau IS THERE A PUBLIC GOOD? 1.Molina: Get God out of it. While God may know everything, man has free will. God’s knowledge is a secondary knowledge that has nothing to do with Human Beings taking responsibility for their actions. Let the enlightenment guide policy toward humans! 2.Hume: Consequences matter, not intent (virtuous or otherwise) 3.Adam Smith: The invisible hand works regardless of the intent of the participants. People are motivated by their sympathy for others 4.Bentham:The greatest happiness for all is the goal of society 5.Mill: maximization of individual utility is the goal of individuals. The maximization of utility for individuals will achieve the the public good. 6.Kaldor: Amend the “Pareto” criterion which was that a choice for society is economically efficient if no other choice can make someone better off without making someone else worse off. Choices can still be efficient if those who are made worse off will accept compensation in being made worse off. 7.Ayn Rand: Don’t trust social objectives, and particularly don’t trust governments that pretend to be achieving the public good. 8.Arrow: With the Impossibility Theorem, unless we accept dictatorship, it is not possible to define what the “public good” is. It is not possible to add or compare the utility of one person with that of another. Arrow’s work on the conditions under which markets generate efficient outcomes provides the basis for other economists to define the “market failures” which prevent the market from generating efficient outcomes. “Public good” takes on a completely different meaning to indicate those goods from which people cannot be excluded from the benefits. This turns Kaldor on his head; the problem is not the compensation of the losers, but forcing the winners to pay up. 9.Stiglitz: Just look at 2008! It’s all about market failures; read my book “FreeFall” 10. Buchanan (B) and Tullock (T). If we can’t determine what the public good is, what the h… is government doing? And let’s take a look at how government decides to do it. B&T create the “Public Choice” discipline to study how government decides. Specifically, the new field finds there is no voting system that is economically efficient in representing what people really want, decisive (being able to choose among alternatives), and equitable. Now what… 11.The totalitarians (Mao, Stalin, Lenin) historically have something to say about how to make people decide to achieve the public good, as defined by them. 12.Socialists. There are ways, short of Communism, to organize communities to take advantage of markets and to decide what is in the communities’ interest. Molina Hume Classical Economics: NeoClassical Economics Yunnus Laffer Law Physiocrats Adam Smith Bentham Say Mill Ricardo Marshall Walras Clark Kaldor Chicago School Turgot Vaubon Quesnay Condorcet Bohm Bawerk Austrian von Mises Economics Hayek Laissez-Faire: Friedman Shultz Reagan Bush Cheney Ayn Rand Buchanan Tullock Kornai Greenspan Microecon omics Macroecon omics 3rd generation: Reich Stiglitz Rivlin Tyson Great Society: Solow Okun New Deal: Berle KEYNES Industrial Organization Mueller Galbraith Bain Institutionalism Commons Veblen Ward Socialism Malthus Colbert Heterodox Bowles Arrow Habermas Communism Mao Tse-Tung Stalin Lenin Marx Fourier Owen Proudhon St. Simon Rousseau HOW DOES MONEY AFFECT INCOME? Law is highly innovative in creating a central bank that issues money which is redeemable for interest bearing debt and/or high return stock in speculative colonial enterprises. Keynes believes money has a crucial impact on the economy through interest rates. Higher interest rates choke off investment, lower aggregate expenditure, and, through a multiplying effect, lower income of the economy. Hayek opposes Keynes and views manipulation of interest rates to stimulate the economy as a source of false signals about what sectors to subsidize. The overstimulated sectors produce surpluses of capital that will only be wasted; the overhang of housing after 2008 is a pretty good illustration of his point. Friedman sees the policy on money as the root of the depression. To avoid shocks and counterproductive anticipations of central bank actions to change the money supply, he advocates raising the money supply at a steady rate through time. Mundell recognizes the interest rate changes of the central bank in controlling the money supply may be counterproductive. While an autonomous economy might respond to higher interest rates with a lower money supply, foreign investment may actually cause a surge in money in response to higher interest rates. Solow says in response: "Everything reminds Milton Friedman of the money supply. Everything reminds me of sex, but I try to keep it out of my papers.” (http://en.wikipedia.org/wiki/Robert_Solow July 17, 2011) Shultz wants to get the U.S. off of the gold standard and is a key decision maker in the decision to end the Bretton Woods system on August 15, 1971. (Arthur Burns, Diary, 2010 University of Kansas Press). Greenspan masters the art of minimal information to prevent shocks from sudden changes in Fed policy on the money supply. He adheres to a laissez-faire approach in regulating the housing sector, the derivatives market, and the banking industry which sets him up for some of the blame for the crash of 2008. Molina Hume Classical Economics: NeoClassical Economics Yunnus Laffer Law Physiocrats Adam Smith Bentham Say Mill Ricardo Marshall Walras Clark Kaldor Chicago School Bohm Bawerk Austrian von Mises Economics Hayek Friedman Shultz Reagan Bush Cheney Laissez-Faire ideologues: Ayn Rand Buchanan Tullock Kornai Greenspan Microecon omics Macroecon omics 3rd generation: Reich Stiglitz Rivlin Tyson Great Society: Solow Okun New Deal: Berle KEYNES Turgot Vaubon Quesnay Condorcet Heterodox Industrial Organization Mueller Galbraith Bain Institutionalism Commons Veblen Ward Socialism Malthus Colbert Bowles Arrow Habermas Schumpeter Kondratiev Communism Mao Tse-Tung Stalin Lenin Marx Fourier Owen Proudhon St. Simon Rousseau WHO ARE THE BAD GUYS? Quesnay: Manufacturers are the bad guys. Quesnay views the French Aristocrats and the manufacturers that serve them as parasites on the agricultural sector. He develops his Tableau économique of the relationships among the sectors with this in mind. Proudhon: “What capital does to labour, and the State to liberty, the Church does to the spirit.” (http://en.wikipedia.org/wiki/Pierre-Joseph_Proudhon August 16, 2011) Trust no institution, particularly anyone who tries to govern. Proudhon is one of the first anarchists. Ironically similar to Ayn Rand with respect to government. Marx: The capitalists are the bad guys. All value can be traced to the labor in it. The surplus received by the capitalists has been stolen from the share owed to the workers. Socialism: The capitalists are the bad guys who have foisted industrialization on the workers and who are responsible for the inhuman conditions in which the workers find themselves. Industrial Organization: Those who have market power are the bad guys. They are the ones who curb production, charge exorbitant prices, inefficiently produce, excessively advertise, and fail to provide quality to the customer. At their doorstep can be laid the economy of waste, pollution, and dysfunctional public policy. The Santa Clara Supreme Court decision and Citizens United should be reversed! Hayek: The socialists and the communists are the bad guys because they make the economy inefficient by inhibiting discovery and exchange of information. Schumpeter: The self-interested technocrats cause stagnation by preventing creative destruction. They’re the bad guys. Ayn Rand and Laissez-Faire Economists: Government is the bad guy because it takes away the liberty people need to be the best that they can be. Kornai: Totalitarian government is bad because it leads to a shortage economy. Habermas: The corporate-capital-driven mass media is the evil that creates the bourgeois, consumption-driven public that kills communicative competence and rationality. Molina Hume Classical Economics: NeoClassical Economics Yunnus Laffer Law Physiocrats Adam Smith Bentham Say Mill Ricardo Marshall Walras Clark Kaldor Chicago School Bohm Bawerk Austrian von Mises Economics Hayek Friedman Shultz Reagan Bush Cheney Laissez-Faire ideologues: Ayn Rand Buchanan Tullock Kornai Greenspan Microecon omics Macroecon omics 3rd generation: Reich Stiglitz Rivlin Tyson Great Society: Solow Okun New Deal: Berle KEYNES Turgot Vaubon Quesnay Condorcet Heterodox Industrial Organization Mueller Galbraith Bain Institutionalism Commons Veblen Ward Socialism Malthus Colbert Bowles Arrow Habermas Schumpeter Kondratiev Communism Mao Tse-Tung Stalin Lenin Marx Fourier Owen Proudhon St. Simon Rousseau