PowerPoint Chapter 14

advertisement

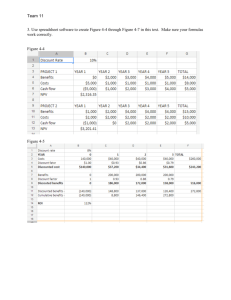

Management Accounting: A Road of Discovery Management Accounting: A Road of Discovery James T. Mackey Michael F. Thomas Presentations by: Roderick S. Barclay Texas A&M University - Commerce James T. Mackey California State University - Sacramento © 2000 South-Western College Publishing Chapter 14 How can we control the change process? Capital budgeting and the balanced scorecard Key Learning Objectives • Define present value, and compute the present value of a lump sum and an annuity. • Calculate an investment’s net present value and relate NPV to the investment’s time-adjusted ROI. • Discuss how the timing of cashflows and risk affect capital budgeting decisions, and determine the payback period. • Explain the need for multiple capital budgeting methods, and calculate the accounting rate of return. • Describe four perspectives for long-run value and create a balanced scorecard. • [Appendix A] Incorporate taxes into NPV and time-adjusted ROI calculations. Capital Budgeting Capital Budgeting influences cashflows for many years. Capital projects usually involve large cash outflows early and smaller cash inflows over many years later in the project. A thorough knowledge of the process and the measurements involved is necessary to avoid bad decisions. Part I The Time Value of Money Compound Interest and The Time Value of Money Deposit $100 today In 1 year Savings account $100 beginning balance + interest earned Beginning balance x 10% Savings account ending balance In 2 years $100 $110 Beginning + 10 balance x 10% + 11 $110 $121 ‘FUTURE Value’ includes compounded returns — earning interest on interest — the actual dollars received in the future. Comparing Future Values and Present Values Present value $100 x (1 + compound interest rate) = x 1.21 = Future value $122 Future value $121 (1 + compound interest rate) = 1.21 = Present value $100 x (1 / 1.21) = $100 x Present value (PV) factor x 0.82644 = Present value $100 or $121 Or Future value $121 The ‘Present Value’ of future cashflows is the value of future cashflows in current dollars today. Comparing Present Value Factors for Lump Sums and Annuities PV factor for a lump sum at 10% Year Cashflow Present Value 1 $200,000 x 0.9091 = $181,820 2 $200,000 x 0.8264 = 165,280 3 $200,000 x 0l,7518 = 150,260 4 $200,000 x 0.6830 = 136,600 5 $200,000 x 0.6209 = 124,180 6 $200,000 x 0.5645 = 112,900 7 $200,000 x 0.5132 = 102,640 $200,000 x 4.8684 = $973,680 10% PV factor for an annuity = the sum of the PV factors for a lump sum Because money today is more valuable than money in the future, future money must be ‘discounted’ to today’s value. Using ROI and NPV in Capital Budgeting Review Exhibit 14-7, p. 514 and remember the following constraints. The ‘discount or interest’ rate is the opportunity cost of investing in assets, like machines, rather than the next best investment. In practice discount rates could be the company’s cost of capita, required Return On Investment, or a ‘risk adjusted’ Return On Investment. Remember, to increase value we must only accept projects that have more value than our existing uses of cash. Therefore, we only accept projects with positive NPV. The idea is that the NPV is the value increase we can expect if we make the investment. Cashflow Issues Review and analyze Exhibit 14-8, p. 515, ‘Cashflow Timing Effects on NPV and ROI’. Review and analyze Exhibit 14-9, p. 516, ‘Comparing Present Value Factors for Different Discount Rates’. The value of future cashflows depends upon the company’s current opportunities or some version of their ROI. Change ‘the time it takes to receive money’, or ‘company’s ROI’, and the present value will change. The Cashflow ‘Teeter-Totter’ and Risk Review Exhibit 14-10, p. 517, ‘Future Cashflows are Less Valuable with Higher Discount Rates. Remember: More RISK means future cashflows are more uncertain. More RISK requires higher expected returns to compensate for the chances of NOT receiving future cashflows. More Risk Issues Hence, some companies use a ‘RISK-Adjusted Rate of Return’ for riskier investments. Because the future is never certain, most companies use multiple measures to evaluate capital investments. THE TIME ADJUSTED RETURN ON INVESTMENT is the discount rate that makes the value of the cash investment exactly equal to the cash returned. That is, the net present value is zero. Usually this calculation requires a computer. The time adjusted ROI is the breakeven return for the project. If the time adjusted ROI is greater than the company’s current ROI, then the project will increase the company’s value — Accept. Concept Review Revisit Exhibit 14-6, p. 513, and 14-7, p. 514. Apply the understanding of those exhibits with the knowledge you have gained from the succeeding exhibits and you should have a thorough understanding of the concepts underlying NPV and the Time Value of Money. Part II Payback Period — Another Way to Look at the Project Payback Questions How long will our investment be at risk? When do we get our original cash investment back? Let’s review some alternatives. Payback Period for a Constant Annuity Year Investment Now $1,000,000 Annuity received Net cashflow ($1,000,000) 1 $400,000 ( 600,000) 2 $400,000 ( 200,000) 3 $400,000 200,000 4 $400,000 600,000 $200,000 Payback period = 2 years + $400,000 Payback period = 2.5 years Payback Period for a Variable Annuity Year Investment Now $1,000,000 Annuity received Net cashflow ($1,000,000) 1 $100,000 ( 900,000) 2 $200,000 ( 700,000) 3 $400,000 ( 300,000) 4 $700,000 400,000 $300,000 Payback period = 3 years + $700,000 Payback period = 3.5 years Part III Accounting Rate of Return on Investment Accounting Rate of Return (ARR) Investment’s average annual profit ARR = Investment’s average book value $ 30,000 ARR = $100,000 2 ARR = 60% Annual ARR calculations follow on the next two slides Depreciation and Book Value Table Year Beginning book value Less depreciation Ending book value Average book value 1 $100,000 ($20,000) $80,000 $90,000 2 80,000 ($20,000) 60,000 70,000 3 60,000 ($20,000) 40,000 50,000 4 40,000 ($20,000) 20,000 30,000 5 20,000 ($20,000) 0 10,000 Annual ARR calculations Year Profit Average book value = ARR 1 $30,000 $90,000 = 33% 2 $30,000 70,000 = 43% 3 $30,000 50,000 = 60% 4 $30,000 30,000 = 100% 5 $30,000 10,000 = 300% Management Considerations in Using Capital Budgeting Methods Capital budgeting method Net present value (NPV) Time adjusted ROI (IRR) Payback period Accounting rate of return (ARR) Differentiating features Reinvests cashflows at the discount rate. Reinvests cashflows at the project’s ROI. Measures the length of time our investment is at risk, but does not consider the time value of money (the interest we can earn from the returns). How the outside world sees us. How investments affect our financial statements (again without considering the time value of money). Using Multiple Capital Budgeting Methods is an International Phenomenon Visit Exhibit 14-14, p. 522. Notice that all companies do not use the same methods for evaluating capital budgeting. Note also that not all companies use the same accounting standards. Part IV Nonfinancial Decision Criteria — The Balance Scorecard Stakeholders Stakeholders can significantly influence the value of an organization. Therefore, we need to measure factors important to stakeholder value. Stakeholder Value Stakeholders Source of Value Measurement Objective Investors & creditors Financial value Financial returns of the company compared to other companies. Customers Value of the company’s goods or services Characteristics of goods or services that influence their value for customers. Workers & management Efficiency of processes that produce goods & services Relative value added by internal processes. Workers & Management Learning and Innovation The value of continuous improvement Four Perspectives for a Balanced Scorecard The Glass Box Internal processes focus — Which process reflect how our processes create value? Innovation and Learning focus — Which measures reflect continuous improvement? The Black Box Financial focus — Which measures covey our value to stockholders and lenders? Customer focus — Which measures reflect our value to customers? Reasons for a Balanced Scorecard The cost of a product doesn’t determine the value of a product. Value only exists in the eyes of the customer. We believe financial measures alone are NOT sufficient to measure long-term value. We believe financial measures alone do NOT always direct management to make valueadding decisions. Examples of Financial Focus Goals and Measures Company Goals Measures Underwater engineering and construction Investor value Liquidity Project success ROI Cashflow Project profitability Electronics firm Sales growth Profitability Prosperity Annual change in sales and profits ROI Cashflow Aggressive global expansion Retain the preferred supplier Increasing share of market growth Food company Ratio of U.S. to international sales Volume and revenue trends by type of business Company growth versus industry growth More Examples of Financial Focus Goals and Measures Company Commercial bank Goals Efficiency Loan loss minimization Loan delinquencies Measures Biotechnology firm Growth Profitability Industry leadership Overhead expense ratios Number of problem loans, early detection Number of bad loans underwritten Revenue percentage increase ROI, Earnings per share Market share Examples of Customer Focus Goals and Measures Company Underwater engineering and construction Goals Value for the money Hassle free relationships Innovation Measures Electronics firm Customer support Delivery Quality Competitive price comparisons Customer satisfaction surveys Market share Response time On time delivery ratio Number of defects, number of visits to customers Examples of Customer Focus Goals and Measures Company Food company Goals Commercial bank Measures Customize products for local customers Lowest cost supplier Product expansion Personalized service Pricing Competitive products Cross-sell ratio Total cost comparison with competition Percentage of R&D products being test marketed by customers Number of complaints Competitive comparisons Number of products offered per year Examples of Customer Focus Goals and Measures Company Biotechnology firm Goals New products Accurate invoices Early payment Measures Percentage of sales from new products Percentage of error free invoices Percentage of customers paying early Examples of Internal Processes Focus Goals and Measures Company Underwater engineering and construction Goals Workplace safety Project success Project quality Measures Electronics firm Manufacturing efficiency Innovation New businesses Safety incident index Project performance index Rework Lead time Rate of new product introductions per quarter Number of new business starts per year Examples of Internal Processes Focus Goals and Measures Company Food company Goals Predictable production Lowest cost base Distribution efficiency Measures First pass success rate Comparison against lowest cost competitor Percent of perfect orders Commercial bank Incorporated in customer focus Incorporated in customer focus Biotechnology firm Low cost products Inventory reduction New products Per unit cost versus competition Inventory vs. percentage of sales Budget vs. actual number introduced Examples of Innovation and Learning Focus Goals and Measures Company Goals Measures Underwater engineering and construction Employee innovation Revenue generation Employee morale Number of suggestions per employee Revenue per employee Staff attitude survey Electronics firm Research and development Market leadership Technology leadership Number of patents Market share in all major markets Product performance compared to competition Examples of Innovation and Learning Focus Goals and Measures Company Food company Goals Commercial bank Measures Culture supports innovation Linking strategies to rewards Develop core competencies Enhanced job skills Participation in firm’s success Competitive wages and benefits Annual preparedness assessment Net income per dollar of payroll Percent competency deployment matrix filled Training, schooling Bonuses based on corporate and personal performances Annual market survey Examples of Innovation and Learning Focus Goals and Measures Company Biotechnology firm Goals New active ingredients Prprietary position Measures Number of new ingredients identified Number of new patents Criteria for Choosing Performance Measures The Communication focus Measures should reflect longterm value creation Communicate to external stakeholders that we are creating long-term value Communicate to internal stakeholders that they are creating long-term value The Behavioral focus Is this what we want our people to do? Does this measure correctly motivate them? Is this measure understanding and common sense to those being evaluated by it? Multree Homes Review Exhibit 14-21, p. 532 ‘Multree Homes Balanced Scorecard’. This will provide you an example of the Balanced Scorecard methodology applied to a company with which you are intimately familiar.