29-May-09 PRELIMINARY RESULTS Change (% Under the

advertisement

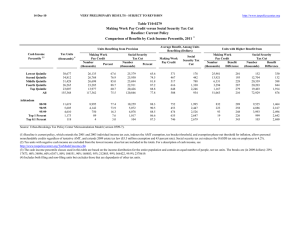

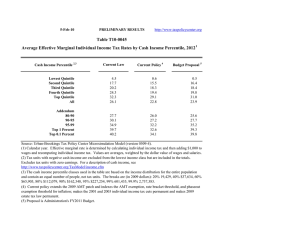

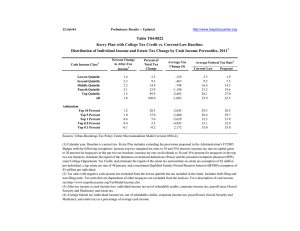

29-May-09 PRELIMINARY RESULTS http://www.taxpolicycenter.org Click on PDF or Excel link above for additional tables containing more detail and breakdowns by filing status and demographic groups. Table T09-0293 Administration's Fiscal Year 2010 Budget Proposals Major Individual Income Tax Provisions Baseline: Administration Baseline Distribution of Federal Tax Change by Cash Income Percentile, 2017 Summary Table Cash Income 2,3 Percentile Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Percent of Tax Units 4 With Tax Cut With Tax Increase Percent Change in After-Tax Income 5 Share of Total Federal Tax Change Average Federal Tax Change ($) 1 Average Federal Tax Rate6 Change (% Points) Under the Proposal 65.9 72.2 84.4 83.4 55.6 71.7 0.1 0.3 0.1 0.1 15.8 2.4 3.6 1.9 1.3 0.8 -1.3 0.0 2,362.8 2,674.1 2,778.5 2,450.0 -10,206.0 100.0 -459 -560 -648 -681 3,268 -5 -3.4 -1.7 -1.1 -0.6 1.0 0.0 1.4 8.6 15.6 19.1 25.7 20.8 75.4 57.5 15.6 6.9 1.8 0.3 1.9 53.6 87.4 96.5 0.6 0.2 -0.9 -4.1 -4.6 1,217.6 250.7 -1,636.3 -10,037.9 -5,032.4 -774 -327 2,626 63,110 310,106 -0.5 -0.1 0.6 3.0 3.3 21.8 23.1 25.4 30.1 32.4 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-1). Number of AMT Taxpayers (millions). Baseline: 6.8 Proposal: 5.5 (1) Calendar year. Administration baseline extends the 2009 AMT patch and indexes the AMT exemption, rate bracket threshold, and phaseout exemption threshold for inflation; makes the 2001 and 2003 individual income tax cuts permanent and makes 2009 estate tax law permanent. Proposal would: (a) extend the Making Work Pay Credit, reduce the phase-out rate to 1.6 percent, and index the phase-out thesholds for inflation after 2010; (b) extend the higher EITC credit value for families with 3 children and higher phase-out threshold for married couples; (c) modify the saver's credit making it equal to 50% of the first $500 of retirement savings ($1,000 for couples) and fully refundable; (d) create automatic 401(k)s and IRAs; (e) extend the American Opportunity Tax Credit; (f) extend the $3,000 child tax credit refundability threshold; (g) reinstate the 39.6 percent bracket; (h) change the threshold for the 36-percent tax bracket to $250,000 less the standard deduction and two personal exemptions for married couples filing jointly and $200,000 less the standard deduction and one personal exemption for single filers, indexed for inflation after 2009; (i) set the thresholds for the personal exemption phase-out and limitation on itemized deductions to $250,000 of AGI (married) and $200,000 (single), indexed for inflation after 2009; (j) impose a 20 percent rate on capital gains and qualified dividends for taxpayers in the top two tax brackets and repeal the 8 percent and 18 percent rates for assets held for more than 5 years; (k) limit value of itemized deduction to 28 percent; (l) maintain the estate tax at its 2009 parameters. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The breaks are (in 2009 dollars): 20% $20,846, 40% $39,988, 60% $71,590, 80% $124,539, 90% $180,564, 95% $252,295, 99% $660,987, 99.9% $3,049,618. (4) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (5) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 29-May-09 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T09-0293 Administration's Fiscal Year 2010 Budget Proposals Major Individual Income Tax Provisions Baseline: Administration Baseline 1 Distribution of Federal Tax Change by Cash Income Percentile, 2017 Detail Table Percent of Tax Units4 Cash Income Percentile2,3 With Tax Cut Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Increase Percent Change in After-Tax Income5 Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Under the Proposal Average Federal Tax Rate6 Change (% Points) Under the Proposal 65.9 72.2 84.4 83.4 55.6 71.7 0.1 0.3 0.1 0.1 15.8 2.4 3.6 1.9 1.3 0.8 -1.3 0.0 2,362.8 2,674.1 2,778.5 2,450.0 -10,206.0 100.0 -459 -560 -648 -681 3,268 -5 -70.3 -16.5 -6.4 -3.3 4.0 0.0 -0.6 -0.7 -0.7 -0.6 2.6 0.0 0.3 3.4 10.3 18.5 67.5 100.0 -3.4 -1.7 -1.1 -0.6 1.0 0.0 1.4 8.6 15.6 19.1 25.7 20.8 75.4 57.5 15.6 6.9 1.8 0.3 1.9 53.6 87.4 96.5 0.6 0.2 -0.9 -4.1 -4.6 1,217.6 250.7 -1,636.3 -10,037.9 -5,032.4 -774 -327 2,626 63,110 310,106 -2.1 -0.6 2.6 10.9 11.2 -0.3 -0.1 0.4 2.6 1.3 14.4 10.6 16.5 26.0 12.6 -0.5 -0.1 0.6 3.0 3.3 21.8 23.1 25.4 30.1 32.4 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Cash Income Percentile, 2017 1 Tax Units4 Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Number (thousands) Percent of Total Average Income (Dollars) Average Federal Tax Burden (Dollars) Average AfterTax Income5 (Dollars) Average Federal Tax Rate6 Share of PreTax Income Percent of Total Share of PostTax Income Percent of Total Share of Federal Taxes Percent of Total 40,705 37,758 33,915 28,437 24,688 168,027 24.2 22.5 20.2 16.9 14.7 100.0 13,512 33,137 60,464 105,717 332,349 89,404 652 3,392 10,066 20,910 81,969 18,557 12,860 29,745 50,397 84,807 250,379 70,847 4.8 10.2 16.7 19.8 24.7 20.8 3.7 8.3 13.7 20.0 54.6 100.0 4.4 9.4 14.4 20.3 51.9 100.0 0.9 4.1 11.0 19.1 64.9 100.0 12,437 6,069 4,926 1,257 128 7.4 3.6 2.9 0.8 0.1 165,657 235,719 410,513 2,141,178 9,468,938 36,890 54,659 101,811 581,907 2,761,703 128,767 181,060 308,702 1,559,271 6,707,235 22.3 23.2 24.8 27.2 29.2 13.7 9.5 13.5 17.9 8.1 13.5 9.2 12.8 16.5 7.2 14.7 10.6 16.1 23.5 11.4 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-1). Number of AMT Taxpayers (millions). Baseline: 6.8 Proposal: 5.5 (1) Calendar year. Administration baseline extends the 2009 AMT patch and indexes the AMT exemption, rate bracket threshold, and phaseout exemption threshold for inflation; makes the 2001 and 2003 individual income tax cuts permanent and makes 2009 estate tax law permanent. Proposal would: (a) extend the Making Work Pay Credit, reduce the phase-out rate to 1.6 percent, and index the phase-out thesholds for inflation after 2010; (b) extend the higher EITC credit value for families with 3 children and higher phase-out threshold for married couples; (c) modify the saver's credit making it equal to 50% of the first $500 of retirement savings ($1,000 for couples) and fully refundable; (d) create automatic 401(k)s and IRAs; (e) extend the American Opportunity Tax Credit; (f) extend the $3,000 child tax credit refundability threshold; (g) reinstate the 39.6 percent bracket; (h) change the threshold for the 36-percent tax bracket to $250,000 less the standard deduction and two personal exemptions for married couples filing jointly and $200,000 less the standard deduction and one personal exemption for single filers, indexed for inflation after 2009; (i) set the thresholds for the personal exemption phase-out and limitation on itemized deductions to $250,000 of AGI (married) and $200,000 (single), indexed for inflation after 2009; (j) impose a 20 percent rate on capital gains and qualified dividends for taxpayers in the top two tax brackets and repeal the 8 percent and 18 percent rates for assets held for more than 5 years; (k) limit value of itemized deduction to 28 percent; (l) maintain the estate tax at its 2009 parameters. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The breaks are (in 2009 dollars): 20% $20,846, 40% $39,988, 60% $71,590, 80% $124,539, 90% $180,564, 95% $252,295, 99% $660,987, 99.9% $3,049,618. (4) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (5) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 29-May-09 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T09-0293 Administration's Fiscal Year 2010 Budget Proposals Major Individual Income Tax Provisions Baseline: Administration Baseline 1 Distribution of Federal Tax Change by Cash Income Percentile Adjusted for Family Size, 2017 Detail Table Percent of Tax Units4 Cash Income Percentile2,3 With Tax Cut Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Increase Percent Change in After-Tax Income5 Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Under the Proposal Average Federal Tax Rate6 Change (% Points) Under the Proposal 72.4 67.9 78.9 87.6 56.4 71.7 0.0 0.4 0.2 0.1 12.3 2.4 4.8 1.9 1.3 0.9 -1.2 0.0 2,519.2 2,350.7 2,558.7 2,767.5 -10,136.6 100.0 -595 -530 -599 -693 2,530 -5 -237.8 -19.6 -7.6 -3.9 3.7 0.0 -0.6 -0.6 -0.7 -0.7 2.6 0.0 -0.4 2.4 7.9 17.6 72.4 100.0 -4.7 -1.8 -1.1 -0.8 0.9 0.0 -2.7 7.2 13.7 18.8 25.5 20.8 80.5 48.8 16.5 8.1 1.6 0.0 1.7 39.3 84.0 95.8 0.6 0.2 -0.8 -3.8 -4.5 1,218.1 294.2 -1,618.0 -10,030.9 -5,168.0 -605 -292 2,034 52,157 270,061 -1.9 -0.6 2.4 10.4 11.1 -0.3 -0.1 0.4 2.6 1.3 15.7 11.9 17.8 27.0 13.2 -0.4 -0.2 0.6 2.8 3.2 21.9 23.3 25.2 29.7 32.3 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Cash Income Percentile Adjusted for Family Size, 2017 1 Tax Units4 Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Number (thousands) Percent of Total Average Income (Dollars) Average Federal Tax Burden (Dollars) Average AfterTax Income5 (Dollars) Average Federal Tax Rate6 Share of PreTax Income Percent of Total Share of PostTax Income Percent of Total Share of Federal Taxes Percent of Total 33,450 35,074 33,747 31,556 31,677 168,027 19.9 20.9 20.1 18.8 18.9 100.0 12,732 30,173 53,321 92,353 279,871 89,404 250 2,699 7,881 18,026 68,711 18,557 12,482 27,475 45,440 74,328 211,161 70,847 2.0 8.9 14.8 19.5 24.6 20.8 2.8 7.0 12.0 19.4 59.0 100.0 3.5 8.1 12.9 19.7 56.2 100.0 0.3 3.0 8.5 18.2 69.8 100.0 15,914 7,953 6,289 1,520 151 9.5 4.7 3.7 0.9 0.1 140,958 200,752 349,936 1,857,869 8,388,125 31,426 47,059 86,069 500,412 2,439,842 109,532 153,694 263,867 1,357,456 5,948,283 22.3 23.4 24.6 26.9 29.1 14.9 10.6 14.7 18.8 8.5 14.6 10.3 13.9 17.3 7.6 16.0 12.0 17.4 24.4 11.8 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-1). Number of AMT Taxpayers (millions). Baseline: 6.8 Proposal: 5.5 (1) Calendar year. Administration baseline extends the 2009 AMT patch and indexes the AMT exemption, rate bracket threshold, and phaseout exemption threshold for inflation; makes the 2001 and 2003 individual income tax cuts permanent and makes 2009 estate tax law permanent. Proposal would: (a) extend the Making Work Pay Credit, reduce the phase-out rate to 1.6 percent, and index the phase-out thesholds for inflation after 2010; (b) extend the higher EITC credit value for families with 3 children and higher phase-out threshold for married couples; (c) modify the saver's credit making it equal to 50% of the first $500 of retirement savings ($1,000 for couples) and fully refundable; (d) create automatic 401(k)s and IRAs; (e) extend the American Opportunity Tax Credit; (f) extend the $3,000 child tax credit refundability threshold; (g) reinstate the 39.6 percent bracket; (h) change the threshold for the 36-percent tax bracket to $250,000 less the standard deduction and two personal exemptions for married couples filing jointly and $200,000 less the standard deduction and one personal exemption for single filers, indexed for inflation after 2009; (i) set the thresholds for the personal exemption phase-out and limitation on itemized deductions to $250,000 of AGI (married) and $200,000 (single), indexed for inflation after 2009; (j) impose a 20 percent rate on capital gains and qualified dividends for taxpayers in the top two tax brackets and repeal the 8 percent and 18 percent rates for assets held for more than 5 years; (k) limit value of itemized deduction to 28 percent; (l) maintain the estate tax at its 2009 parameters. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2009 dollars): 20% $14,392, 40% $26,987, 60% $45,911, 80% $76,270, 90% $109,860, 95% $155,381, 99% $400,442, 99.9% $1,863,666. (4) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (5) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 29-May-09 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T09-0293 Administration's Fiscal Year 2010 Budget Proposals Major Individual Income Tax Provisions Baseline: Administration Baseline 1 Distribution of Federal Tax Change by Cash Income Percentile Adjusted for Family Size, 2017 Detail Table - Single Tax Units Percent of Tax Units4 Cash Income Percentile2,3 With Tax Cut Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Increase Percent Change in After-Tax Income5 Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Under the Proposal Average Federal Tax Rate6 Change (% Points) Under the Proposal 66.8 54.4 72.6 84.8 47.4 64.2 0.0 0.3 0.0 0.0 6.5 1.0 3.7 1.4 1.2 0.9 -0.7 0.5 41.6 36.9 43.9 39.6 -62.9 100.0 -335 -301 -402 -463 888 -191 -46.5 -13.4 -6.4 -3.3 1.9 -1.8 -0.7 -0.6 -0.6 -0.3 2.3 0.0 0.9 4.4 11.8 21.7 61.1 100.0 -3.4 -1.3 -1.0 -0.7 0.5 -0.4 3.9 8.4 14.7 20.7 25.7 20.1 74.9 20.5 12.7 6.4 0.5 0.0 0.0 18.7 79.7 94.7 0.4 0.1 -0.2 -3.1 -4.4 12.8 1.8 -3.8 -73.7 -42.2 -339 -105 288 27,640 180,725 -1.4 -0.3 0.5 7.7 9.3 0.1 0.2 0.3 1.7 0.9 16.4 11.3 14.4 19.0 9.2 -0.3 -0.1 0.1 2.2 3.0 23.3 24.3 24.3 30.9 35.2 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Cash Income Percentile Adjusted for Family Size, 2017 1 Tax Units4 Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Average Income (Dollars) Average Federal Tax Burden (Dollars) Average AfterTax Income5 (Dollars) Number (thousands) Percent of Total 17,946 17,740 15,791 12,368 10,255 75,772 23.7 23.4 20.8 16.3 13.5 100.0 9,849 23,350 39,855 66,353 181,320 51,323 721 2,256 6,250 14,217 45,760 10,527 9,128 21,094 33,605 52,136 135,560 40,797 5,447 2,527 1,895 386 34 7.2 3.3 2.5 0.5 0.0 101,176 143,504 245,016 1,246,622 6,069,456 23,957 34,984 59,284 357,437 1,952,452 77,219 108,520 185,732 889,186 4,117,004 Share of PreTax Income Percent of Total Share of PostTax Income Percent of Total Share of Federal Taxes Percent of Total 7.3 9.7 15.7 21.4 25.2 20.5 4.5 10.7 16.2 21.1 47.8 100.0 5.3 12.1 17.2 20.9 45.0 100.0 1.6 5.0 12.4 22.0 58.8 100.0 23.7 24.4 24.2 28.7 32.2 14.2 9.3 11.9 12.4 5.3 13.6 8.9 11.4 11.1 4.5 16.4 11.1 14.1 17.3 8.3 Average Federal Tax Rate6 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-1). (1) Calendar year. Administration baseline extends the 2009 AMT patch and indexes the AMT exemption, rate bracket threshold, and phaseout exemption threshold for inflation; makes the 2001 and 2003 individual income tax cuts permanent and makes 2009 estate tax law permanent. Proposal would: (a) extend the Making Work Pay Credit, reduce the phase-out rate to 1.6 percent, and index the phase-out thesholds for inflation after 2010; (b) extend the higher EITC credit value for families with 3 children and higher phase-out threshold for married couples; (c) modify the saver's credit making it equal to 50% of the first $500 of retirement savings ($1,000 for couples) and fully refundable; (d) create automatic 401(k)s and IRAs; (e) extend the American Opportunity Tax Credit; (f) extend the $3,000 child tax credit refundability threshold; (g) reinstate the 39.6 percent bracket; (h) change the threshold for the 36-percent tax bracket to $250,000 less the standard deduction and two personal exemptions for married couples filing jointly and $200,000 less the standard deduction and one personal exemption for single filers, indexed for inflation after 2009; (i) set the thresholds for the personal exemption phase-out and limitation on itemized deductions to $250,000 of AGI (married) and $200,000 (single), indexed for inflation after 2009; (j) impose a 20 percent rate on capital gains and qualified dividends for taxpayers in the top two tax brackets and repeal the 8 percent and 18 percent rates for assets held for more than 5 years; (k) limit value of itemized deduction to 28 percent; (l) maintain the estate tax at its 2009 parameters. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2009 dollars): 20% $14,392, 40% $26,987, 60% $45,911, 80% $76,270, 90% $109,860, 95% $155,381, 99% $400,442, 99.9% $1,863,666. (4) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (5) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 29-May-09 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T09-0293 Administration's Fiscal Year 2010 Budget Proposals Major Individual Income Tax Provisions Baseline: Administration Baseline 1 Distribution of Federal Tax Change by Cash Income Percentile Adjusted for Family Size, 2017 Detail Table - Married Tax Units Filing Jointly Percent of Tax Units4 Cash Income Percentile2,3 With Tax Cut Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Increase Percent Change in After-Tax Income5 Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Under the Proposal Average Federal Tax Rate6 Change (% Points) Under the Proposal 70.1 71.5 79.1 89.5 63.1 74.0 0.0 0.2 0.4 0.2 15.3 4.9 5.3 2.5 1.4 1.0 -1.3 -0.4 -19.5 -26.3 -34.4 -48.6 229.4 100.0 -872 -872 -854 -916 3,394 463 -247.2 -25.9 -9.1 -4.4 4.2 1.4 -0.3 -0.4 -0.6 -0.9 2.1 0.0 -0.2 1.0 4.7 14.8 79.5 100.0 -5.2 -2.2 -1.2 -0.8 1.0 0.3 -3.1 6.4 12.3 17.6 25.3 21.9 87.9 64.8 18.6 9.2 2.0 0.1 2.2 47.8 85.0 96.1 0.6 0.2 -0.9 -4.0 -4.6 -26.0 -7.0 40.3 222.2 110.3 -808 -402 2,834 60,334 294,112 -2.3 -0.8 2.9 11.0 11.5 -0.6 -0.3 0.3 2.7 1.3 15.7 12.8 20.1 31.0 14.9 -0.5 -0.2 0.7 2.9 3.3 21.2 22.9 25.5 29.5 31.7 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Cash Income Percentile Adjusted for Family Size, 2017 1 Tax Units4 Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Average Income (Dollars) Average Federal Tax Burden (Dollars) Average AfterTax Income5 (Dollars) Number (thousands) Percent of Total 6,484 8,750 11,696 15,376 19,603 62,623 10.4 14.0 18.7 24.6 31.3 100.0 16,852 38,883 69,198 114,228 335,346 152,719 353 3,364 9,335 21,047 81,593 33,000 16,499 35,520 59,864 93,180 253,753 119,718 9,331 5,082 4,122 1,068 109 14.9 8.1 6.6 1.7 0.2 165,784 230,762 400,541 2,063,034 9,022,743 35,975 53,335 99,088 547,143 2,567,620 129,809 177,427 301,453 1,515,891 6,455,122 Share of PreTax Income Percent of Total Share of PostTax Income Percent of Total Share of Federal Taxes Percent of Total 2.1 8.7 13.5 18.4 24.3 21.6 1.1 3.6 8.5 18.4 68.7 100.0 1.4 4.2 9.3 19.1 66.4 100.0 0.1 1.4 5.3 15.7 77.4 100.0 21.7 23.1 24.7 26.5 28.5 16.2 12.3 17.3 23.0 10.3 16.2 12.0 16.6 21.6 9.4 16.2 13.1 19.8 28.3 13.5 Average Federal Tax Rate6 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-1). (1) Calendar year. Administration baseline extends the 2009 AMT patch and indexes the AMT exemption, rate bracket threshold, and phaseout exemption threshold for inflation; makes the 2001 and 2003 individual income tax cuts permanent and makes 2009 estate tax law permanent. Proposal would: (a) extend the Making Work Pay Credit, reduce the phase-out rate to 1.6 percent, and index the phase-out thesholds for inflation after 2010; (b) extend the higher EITC credit value for families with 3 children and higher phase-out threshold for married couples; (c) modify the saver's credit making it equal to 50% of the first $500 of retirement savings ($1,000 for couples) and fully refundable; (d) create automatic 401(k)s and IRAs; (e) extend the American Opportunity Tax Credit; (f) extend the $3,000 child tax credit refundability threshold; (g) reinstate the 39.6 percent bracket; (h) change the threshold for the 36-percent tax bracket to $250,000 less the standard deduction and two personal exemptions for married couples filing jointly and $200,000 less the standard deduction and one personal exemption for single filers, indexed for inflation after 2009; (i) set the thresholds for the personal exemption phase-out and limitation on itemized deductions to $250,000 of AGI (married) and $200,000 (single), indexed for inflation after 2009; (j) impose a 20 percent rate on capital gains and qualified dividends for taxpayers in the top two tax brackets and repeal the 8 percent and 18 percent rates for assets held for more than 5 years; (k) limit value of itemized deduction to 28 percent; (l) maintain the estate tax at its 2009 parameters. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2009 dollars): 20% $14,392, 40% $26,987, 60% $45,911, 80% $76,270, 90% $109,860, 95% $155,381, 99% $400,442, 99.9% $1,863,666. (4) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (5) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 29-May-09 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T09-0293 Administration's Fiscal Year 2010 Budget Proposals Major Individual Income Tax Provisions Baseline: Administration Baseline 1 Distribution of Federal Tax Change by Cash Income Percentile Adjusted for Family Size, 2017 Detail Table - Head of Household Tax Units Percent of Tax Units4 Cash Income Percentile2,3 With Tax Cut Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Increase Percent Change in After-Tax Income5 Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Under the Proposal Average Federal Tax Rate6 Change (% Points) Under the Proposal 85.3 91.8 94.6 88.2 29.3 86.5 0.0 0.7 0.0 0.0 9.7 0.7 5.7 2.0 1.3 0.8 -0.9 1.5 47.7 31.8 21.2 10.5 -11.2 100.0 -930 -662 -642 -572 1,453 -629 113.8 -23.1 -6.9 -3.1 2.8 -8.7 -4.9 -1.9 0.5 1.8 4.4 0.0 -8.6 10.1 27.3 31.5 39.6 100.0 -5.9 -1.9 -1.1 -0.6 0.7 -1.3 -11.2 6.2 14.8 19.7 24.9 13.5 37.7 19.3 10.3 0.8 0.8 0.0 3.5 44.4 93.0 97.8 0.2 0.1 -0.8 -3.9 -4.6 1.1 0.2 -2.2 -10.3 -4.8 -212 -135 2,000 45,032 258,289 -0.7 -0.3 2.6 10.5 11.1 1.2 0.5 0.9 1.8 0.8 14.7 6.2 8.4 10.3 4.5 -0.2 -0.1 0.6 2.8 3.3 23.1 23.9 24.2 29.8 32.5 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Cash Income Percentile Adjusted for Family Size, 2017 1 Tax Units4 Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Average Income (Dollars) Average Federal Tax Burden (Dollars) Average AfterTax Income5 (Dollars) Number (thousands) Percent of Total 8,770 8,213 5,633 3,130 1,317 27,175 32.3 30.2 20.7 11.5 4.9 100.0 15,647 35,755 58,874 91,665 216,103 49,021 -817 2,865 9,334 18,618 52,379 7,225 16,464 32,890 49,540 73,046 163,724 41,797 845 247 187 39 3 3.1 0.9 0.7 0.1 0.0 135,186 188,332 332,770 1,587,850 7,937,589 31,447 45,045 78,368 428,331 2,320,534 103,739 143,287 254,403 1,159,520 5,617,056 Share of PreTax Income Percent of Total Share of PostTax Income Percent of Total Share of Federal Taxes Percent of Total -5.2 8.0 15.9 20.3 24.2 14.7 10.3 22.0 24.9 21.5 21.4 100.0 12.7 23.8 24.6 20.1 19.0 100.0 -3.7 12.0 26.8 29.7 35.1 100.0 23.3 23.9 23.6 27.0 29.2 8.6 3.5 4.7 4.6 1.9 7.7 3.1 4.2 4.0 1.6 13.5 5.7 7.5 8.5 3.7 Average Federal Tax Rate6 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-1). (1) Calendar year. Administration baseline extends the 2009 AMT patch and indexes the AMT exemption, rate bracket threshold, and phaseout exemption threshold for inflation; makes the 2001 and 2003 individual income tax cuts permanent and makes 2009 estate tax law permanent. Proposal would: (a) extend the Making Work Pay Credit, reduce the phase-out rate to 1.6 percent, and index the phase-out thesholds for inflation after 2010; (b) extend the higher EITC credit value for families with 3 children and higher phase-out threshold for married couples; (c) modify the saver's credit making it equal to 50% of the first $500 of retirement savings ($1,000 for couples) and fully refundable; (d) create automatic 401(k)s and IRAs; (e) extend the American Opportunity Tax Credit; (f) extend the $3,000 child tax credit refundability threshold; (g) reinstate the 39.6 percent bracket; (h) change the threshold for the 36-percent tax bracket to $250,000 less the standard deduction and two personal exemptions for married couples filing jointly and $200,000 less the standard deduction and one personal exemption for single filers, indexed for inflation after 2009; (i) set the thresholds for the personal exemption phase-out and limitation on itemized deductions to $250,000 of AGI (married) and $200,000 (single), indexed for inflation after 2009; (j) impose a 20 percent rate on capital gains and qualified dividends for taxpayers in the top two tax brackets and repeal the 8 percent and 18 percent rates for assets held for more than 5 years; (k) limit value of itemized deduction to 28 percent; (l) maintain the estate tax at its 2009 parameters. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2009 dollars): 20% $14,392, 40% $26,987, 60% $45,911, 80% $76,270, 90% $109,860, 95% $155,381, 99% $400,442, 99.9% $1,863,666. (4) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (5) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 29-May-09 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T09-0293 Administration's Fiscal Year 2010 Budget Proposals Major Individual Income Tax Provisions Baseline: Administration Baseline 1 Distribution of Federal Tax Change by Cash Income Percentile Adjusted for Family Size, 2017 Detail Table - Tax Units with Children Percent of Tax Units4 Cash Income Percentile2,3 With Tax Cut Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Increase Percent Change in After-Tax Income5 Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Under the Proposal Average Federal Tax Rate6 Change (% Points) Under the Proposal 93.8 97.8 98.6 96.8 55.9 89.5 0.0 0.4 0.2 0.2 19.1 3.4 6.6 2.6 1.5 1.0 -1.7 0.1 272.2 222.8 211.3 222.7 -831.5 100.0 -1,207 -975 -932 -987 4,478 -91 101.8 -29.3 -8.1 -4.0 4.8 -0.4 -1.1 -0.9 -0.8 -0.8 3.5 0.0 -2.1 2.1 9.3 20.7 69.9 100.0 -7.0 -2.4 -1.3 -0.8 1.2 -0.1 -13.9 5.8 14.7 19.4 26.9 20.9 83.5 40.4 10.5 3.8 0.5 0.1 5.8 71.7 94.1 98.7 0.6 0.1 -1.6 -5.0 -5.1 78.7 8.8 -198.7 -720.4 -315.1 -802 -199 5,712 86,462 399,875 -1.8 -0.3 4.6 12.6 12.1 -0.2 0.0 0.8 2.9 1.3 16.3 11.2 17.6 24.8 11.2 -0.4 -0.1 1.2 3.6 3.6 22.8 24.2 27.4 31.9 33.1 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Cash Income Percentile Adjusted for Family Size, 2017 1 Tax Units4 Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Average Income (Dollars) Average Federal Tax Burden (Dollars) Average AfterTax Income5 (Dollars) Number (thousands) Percent of Total 10,432 10,570 10,488 10,438 8,587 50,838 20.5 20.8 20.6 20.5 16.9 100.0 17,171 40,353 72,386 122,710 362,965 113,062 -1,185 3,327 11,570 24,742 93,249 23,692 18,356 37,026 60,816 97,968 269,716 89,369 4,538 2,056 1,608 385 36 8.9 4.0 3.2 0.8 0.1 189,201 270,179 478,067 2,423,697 11,187,796 43,944 65,613 125,401 687,065 3,299,759 145,257 204,566 352,665 1,736,632 7,888,037 Share of PreTax Income Percent of Total Share of PostTax Income Percent of Total Share of Federal Taxes Percent of Total -6.9 8.2 16.0 20.2 25.7 21.0 3.1 7.4 13.2 22.3 54.2 100.0 4.2 8.6 14.0 22.5 51.0 100.0 -1.0 2.9 10.1 21.4 66.5 100.0 23.2 24.3 26.2 28.4 29.5 14.9 9.7 13.4 16.3 7.1 14.5 9.3 12.5 14.7 6.3 16.6 11.2 16.8 22.0 10.0 Average Federal Tax Rate6 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-1). Note: Tax units with children are those claiming an exemption for children at home or away from home. (1) Calendar year. Administration baseline extends the 2009 AMT patch and indexes the AMT exemption, rate bracket threshold, and phaseout exemption threshold for inflation; makes the 2001 and 2003 individual income tax cuts permanent and makes 2009 estate tax law permanent. Proposal would: (a) extend the Making Work Pay Credit, reduce the phase-out rate to 1.6 percent, and index the phase-out thesholds for inflation after 2010; (b) extend the higher EITC credit value for families with 3 children and higher phase-out threshold for married couples; (c) modify the saver's credit making it equal to 50% of the first $500 of retirement savings ($1,000 for couples) and fully refundable; (d) create automatic 401(k)s and IRAs; (e) extend the American Opportunity Tax Credit; (f) extend the $3,000 child tax credit refundability threshold; (g) reinstate the 39.6 percent bracket; (h) change the threshold for the 36-percent tax bracket to $250,000 less the standard deduction and two personal exemptions for married couples filing jointly and $200,000 less the standard deduction and one personal exemption for single filers, indexed for inflation after 2009; (i) set the thresholds for the personal exemption phase-out and limitation on itemized deductions to $250,000 of AGI (married) and $200,000 (single), indexed for inflation after 2009; (j) impose a 20 percent rate on capital gains and qualified dividends for taxpayers in the top two tax brackets and repeal the 8 percent and 18 percent rates for assets held for more than 5 years; (k) limit value of itemized deduction to 28 percent; (l) maintain the estate tax at its 2009 parameters. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2009 dollars): 20% $14,392, 40% $26,987, 60% $45,911, 80% $76,270, 90% $109,860, 95% $155,381, 99% $400,442, 99.9% $1,863,666. (4) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (5) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 29-May-09 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T09-0293 Administration's Fiscal Year 2010 Budget Proposals Major Individual Income Tax Provisions Baseline: Administration Baseline 1 Distribution of Federal Tax Change by Cash Income Percentile Adjusted for Family Size, 2017 Detail Table - Elderly Tax Units Percent of Tax Units4 Cash Income Percentile2,3 With Tax Cut Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Increase Percent Change in After-Tax Income5 Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Under the Proposal Average Federal Tax Rate6 Change (% Points) Under the Proposal 16.1 16.9 26.1 43.9 31.4 25.5 0.0 0.0 0.0 0.1 12.3 2.3 0.7 0.4 0.3 0.4 -1.0 -0.5 -4.0 -7.6 -9.1 -13.0 133.8 100.0 -85 -89 -143 -283 2,419 334 -31.1 -10.8 -6.3 -3.0 3.7 2.3 -0.1 -0.2 -0.3 -0.5 1.1 0.0 0.2 1.4 3.1 9.7 85.5 100.0 -0.7 -0.3 -0.3 -0.3 0.8 0.4 1.5 2.8 4.6 10.9 22.7 16.7 43.5 32.1 14.6 7.3 1.0 0.0 0.2 29.0 78.9 95.7 0.3 0.1 -0.3 -2.8 -3.8 -6.7 -2.4 8.7 134.1 83.4 -269 -176 671 34,995 199,954 -1.3 -0.5 1.0 7.6 9.2 -0.4 -0.3 -0.3 2.1 1.4 11.4 10.4 20.1 43.5 22.7 -0.2 -0.1 0.2 2.0 2.7 15.6 18.3 21.3 28.6 32.0 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Cash Income Percentile Adjusted for Family Size, 2017 1 Tax Units4 Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Average Income (Dollars) Average Federal Tax Burden (Dollars) Average AfterTax Income5 (Dollars) Number (thousands) Percent of Total 5,486 9,944 7,536 5,425 6,505 35,193 15.6 28.3 21.4 15.4 18.5 100.0 12,851 26,105 46,194 84,549 297,285 87,173 275 831 2,284 9,460 65,057 14,262 12,576 25,274 43,910 75,088 232,228 72,912 2,933 1,593 1,528 451 49 8.3 4.5 4.3 1.3 0.1 127,727 183,292 318,053 1,732,517 7,447,999 20,187 33,686 67,019 461,102 2,179,691 107,540 149,607 251,035 1,271,415 5,268,308 Share of PreTax Income Percent of Total Share of PostTax Income Percent of Total Share of Federal Taxes Percent of Total 2.1 3.2 4.9 11.2 21.9 16.4 2.3 8.5 11.4 15.0 63.0 100.0 2.7 9.8 12.9 15.9 58.9 100.0 0.3 1.7 3.4 10.2 84.3 100.0 15.8 18.4 21.1 26.6 29.3 12.2 9.5 15.8 25.5 11.9 12.3 9.3 15.0 22.3 10.1 11.8 10.7 20.4 41.4 21.3 Average Federal Tax Rate6 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-1). Note: Elderly tax units are those with either head or spouse (if filing jointly) age 65 or older. (1) Calendar year. Administration baseline extends the 2009 AMT patch and indexes the AMT exemption, rate bracket threshold, and phaseout exemption threshold for inflation; makes the 2001 and 2003 individual income tax cuts permanent and makes 2009 estate tax law permanent. Proposal would: (a) extend the Making Work Pay Credit, reduce the phase-out rate to 1.6 percent, and index the phase-out thesholds for inflation after 2010; (b) extend the higher EITC credit value for families with 3 children and higher phase-out threshold for married couples; (c) modify the saver's credit making it equal to 50% of the first $500 of retirement savings ($1,000 for couples) and fully refundable; (d) create automatic 401(k)s and IRAs; (e) extend the American Opportunity Tax Credit; (f) extend the $3,000 child tax credit refundability threshold; (g) reinstate the 39.6 percent bracket; (h) change the threshold for the 36-percent tax bracket to $250,000 less the standard deduction and two personal exemptions for married couples filing jointly and $200,000 less the standard deduction and one personal exemption for single filers, indexed for inflation after 2009; (i) set the thresholds for the personal exemption phase-out and limitation on itemized deductions to $250,000 of AGI (married) and $200,000 (single), indexed for inflation after 2009; (j) impose a 20 percent rate on capital gains and qualified dividends for taxpayers in the top two tax brackets and repeal the 8 percent and 18 percent rates for assets held for more than 5 years; (k) limit value of itemized deduction to 28 percent; (l) maintain the estate tax at its 2009 parameters. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2009 dollars): 20% $14,392, 40% $26,987, 60% $45,911, 80% $76,270, 90% $109,860, 95% $155,381, 99% $400,442, 99.9% $1,863,666. (4) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (5) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income.