21-Mar-06

Preliminary Results

http://www.taxpolicycenter.org

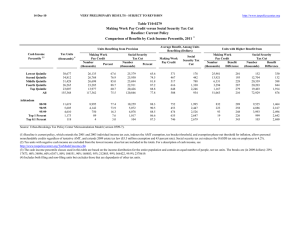

Table T06-0065

Impose $10,000 Limit on Individual Income Tax Cuts in

EGTRRA, JGTRRA, and WFTRA With Extension of 2005 AMT Relief, Indexed for Inflation

Distribution of Federal Tax Change by Cash Income Percentile, 2011 1

Cash Income

Percentile2

Percent of Tax Units 3

With Tax

Cut

With Tax

Increase

Percent

Change in

After-Tax

Income4

Share of

Total Federal

Tax Change

Average Federal Tax Change

Dollars

Percent

Share of Federal Taxes

Change (%

Points)

Under the

Proposal

Average Federal Tax Rate 5

Change (%

Points)

Under the

Proposal

Lowest Quintile

Second Quintile

Middle Quintile

Fourth Quintile

Top Quintile

All

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

5.2

1.0

0.0

0.0

0.0

0.0

-1.2

-0.7

0.0

0.0

0.0

0.0

100.0

100.0

0

0

0

0

2,082

416

0.0

0.0

0.0

0.0

3.7

2.6

0.0

-0.1

-0.2

-0.5

0.7

0.0

0.5

2.6

8.0

17.6

71.1

100.0

0.0

0.0

0.0

0.0

0.9

0.5

3.8

8.7

15.2

19.3

25.4

21.5

Addendum

Top 10 Percent

Top 5 Percent

Top 1 Percent

Top 0.5 Percent

Top 0.1 Percent

0.0

0.0

0.0

0.0

0.0

10.4

20.6

72.8

85.5

94.6

-1.6

-2.2

-4.0

-4.8

-5.6

100.0

100.0

97.6

90.0

59.3

4,164

8,325

40,659

74,975

247,017

4.8

6.1

10.5

12.1

13.3

1.1

1.5

1.9

1.8

1.2

55.6

43.6

26.0

21.1

12.8

1.2

1.6

2.9

3.4

3.9

26.9

28.1

30.7

31.7

33.5

Baseline Distribution of Income and Federal Taxes

by Cash Income Percentile, 2011 1

Cash Income

Percentile2

Tax Units3

Number

(thousands)

Percent of

Total

Average

Income

(Dollars)

Average

Federal Tax

Burden

(Dollars)

Average

After-Tax

Income4

(Dollars)

Average

Federal Tax

Rate5

Share of PreTax Income

Percent of

Total

Share of PostTax Income

Percent of

Total

Share of

Federal Taxes

Percent of

Total

Lowest Quintile

Second Quintile

Middle Quintile

Fourth Quintile

Top Quintile

All

30,620

31,187

31,196

31,195

31,197

155,984

19.6

20.0

20.0

20.0

20.0

100.0

9,918

24,924

43,588

75,268

230,709

76,577

378

2,157

6,639

14,552

56,559

16,078

9,540

22,767

36,949

60,716

174,150

60,499

3.8

8.7

15.2

19.3

24.5

21.0

2.5

6.5

11.4

19.7

60.3

100.0

3.1

7.5

12.2

20.1

57.6

100.0

0.5

2.7

8.3

18.1

70.4

100.0

Addendum

Top 10 Percent

Top 5 Percent

Top 1 Percent

Top 0.5 Percent

Top 0.1 Percent

15,599

7,799

1,560

780

156

10.0

5.0

1.0

0.5

0.1

341,597

511,855

1,399,560

2,196,271

6,282,917

87,592

135,566

388,886

622,031

1,858,156

254,005

376,289

1,010,674

1,574,240

4,424,761

25.6

26.5

27.8

28.3

29.6

44.6

33.4

18.3

14.3

8.2

38.0

28.1

15.1

11.8

6.6

54.5

42.2

24.2

19.3

11.6

Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0305-3A).

(1) Calendar year. Baseline is extended law with the extension of the 2005 AMT exemption levels ($58,000 for married couples and $40,250 for singles and heads of household), indexed for inflation

after 2005; allowance of personal non-refundable credits regardless of tentative AMT; and extending the non-refundable credit for elective deferrals and IRA contributions (the "saver's credit"). Proposal

includes extending but limiting the individual income tax cuts due to the following provisions in EGTRRA, JGTRRA, and WFTRA to $10,000 (indexed for inflation after 2007): marginal tax rates; the

10-percent bracket; the child tax credit; the child and dependent care credit; the standard deduction, 15-percent bracket, and EITC for married couples; tax rates on long-term capital gains and dividends;

pension and IRA provisions; expansion of student loan interest deduction (excludes other education provisions). The effect of these provisions is measured against a current-law baseline with the

extension of the 2000 AMT exemption levels ($45,000 for married couples and $33,750 for singles and heads of household), indexed for inflation after 2000; and allowance of personal non-refundable

credits regardless of tentative AMT.

(2) Tax units with negative cash income are excluded from the lowest quintile but are included in the totals. For a description of cash income, see

http://www.taxpolicycenter.org/TaxModel/income.cfm

(3) Includes both filing and non-filing units. Tax units that are dependents of other taxpayers are excluded from the analysis.

(4) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax.

(5) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income.

0

0