21-Jul-10 PRELIMINARY RESULTS With Tax With Tax Cut

advertisement

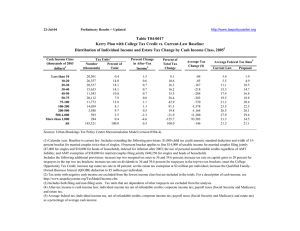

21-Jul-10 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T10-0172 Incremental Effects of Allowing the 2001 and 2003 Tax Cuts to Sunset Eliminate AMT Patch 1 Distribution of Federal Tax Change by Cash Income Level, 2012 Summary Table Cash Income Level (thousands of 2009 dollars) 2 Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All Percent of Tax Units 3 With Tax Cut 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 With Tax Increase 0.0 0.0 0.0 1.1 4.5 12.5 29.6 38.5 60.3 22.1 14.5 12.5 Percent Change in After-Tax Income 4 0.0 0.0 0.0 0.0 -0.1 -0.2 -0.6 -0.7 -0.9 -0.1 0.0 -0.4 Share of Total Federal Tax Change Average Federal Tax Change ($) 0.0 0.0 0.0 0.2 1.2 7.4 16.6 40.7 32.1 1.4 0.3 100.0 0 0 0 5 35 123 433 741 2,035 498 235 239 Average Federal Tax Rate5 Change (% Points) 0.0 0.0 0.0 0.0 0.1 0.2 0.5 0.5 0.7 0.1 0.0 0.3 Under the Proposal 5.4 5.3 10.8 15.0 17.5 19.6 21.7 24.6 27.3 28.5 33.8 23.5 Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-5). Number of AMT Taxpayers (millions). Baseline: 1.2 Proposal: 19.7 ** This table is part of a series of tables showing the distributional effects of moving incrementally from current policy to current law. For definitions and further information, see “Related Tables: Moving Incrementally from Current Policy to Current Law” at http://taxpolicycenter.org/numbers/displayatab.cfm?template=simulation&SimID=367 (1) Calendar year. Baseline is current policy (extension of the 2001-2003 tax cuts and patching AMT using 2009 parameters indexed for inflation) plus estate tax at current law level— a 55 percent top tax rate and a $1 million exemption, not indexed); top two tax brackets raised to 36 and 39.6 percent; restoration of the personal exemption phaseout (PEP) and the limitation on itemized deductions (Pease); increased tax rates on long-term capital gains (10 percent for tax units in 15 percent bracket, 20 percent for rest) and reduced rates for gains on assets held 5 years or longer; taxation of all dividends as ordinary income; removal of low- and middleincome tax cuts (eliminate the 10 percent bracket and increase the 25 and 28 percent tax rates to 28 and 31 percent; restore marriage penalties by setting the standard deduction and 10 and 15 percent tax brackets for couples filing jointly to 1.67 times those for singles and making the EITC phaseout threshold for couples filing jointly the same as that for singles; and repeal expansions of the student loan interest deduction, the Earned Income Tax Credit (EITC), the Child and Dependent Care Tax Credit (CDCTC), and the Child Tax Credit (CTC)). Policy is elimination of the AMT patch. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (4) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (5) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 21-Jul-10 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T10-0172 Incremental Effects of Allowing the 2001 and 2003 Tax Cuts to Sunset Eliminate AMT Patch Distribution of Federal Tax Change by Cash Income Level, 2012 1 Detail Table Cash Income Level (thousands of 2009 dollars) 2 Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All Percent of Tax Units With Tax Cut 3 With Tax Increase 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 1.1 4.5 12.5 29.6 38.5 60.3 22.1 14.5 12.5 Percent Change in After-Tax Income 4 Share of Total Federal Tax Change 0.0 0.0 0.0 0.0 -0.1 -0.2 -0.6 -0.7 -0.9 -0.1 0.0 -0.4 0.0 0.0 0.0 0.2 1.2 7.4 16.6 40.7 32.1 1.4 0.3 100.0 Average Federal Tax Change Dollars 0 0 0 5 35 123 433 741 2,035 498 235 239 Percent 0.0 0.0 0.0 0.1 0.4 1.0 2.3 2.2 2.6 0.3 0.0 1.4 Share of Federal Taxes Change (% Points) 0.0 0.0 0.0 0.0 0.0 0.0 0.1 0.2 0.2 -0.1 -0.3 0.0 Under the Proposal 0.2 0.7 2.1 3.1 3.7 10.2 10.1 25.5 17.0 7.5 19.9 100.0 Average Federal Tax Rate 5 Change (% Points) 0.0 0.0 0.0 0.0 0.1 0.2 0.5 0.5 0.7 0.1 0.0 0.3 Under the Proposal 5.4 5.3 10.8 15.0 17.5 19.6 21.7 24.6 27.3 28.5 33.8 23.5 Baseline Distribution of Income and Federal Taxes 1 by Cash Income Level, 2012 Cash Income Level (thousands of 2009 dollars) 2 Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All Tax Units 3 Number (thousands) 16,958 24,305 21,133 16,074 12,909 22,702 14,431 20,606 5,930 1,048 531 157,348 Percent of Total 10.8 15.5 13.4 10.2 8.2 14.4 9.2 13.1 3.8 0.7 0.3 100.0 Average Income (Dollars) 5,723 15,533 25,808 36,190 46,615 64,099 90,195 141,257 296,062 704,969 3,114,004 76,169 Average Federal Tax Burden (Dollars) 309 827 2,781 5,415 8,116 12,461 19,163 34,059 78,845 200,326 1,053,615 17,653 Average AfterTax Income 4 (Dollars) 5,414 14,706 23,026 30,774 38,499 51,639 71,032 107,198 217,218 504,643 2,060,389 58,516 Average Federal Tax Rate 5 5.4 5.3 10.8 15.0 17.4 19.4 21.3 24.1 26.6 28.4 33.8 23.2 Share of PreTax Income Percent of Total Share of PostTax Income Percent of Total Share of Federal Taxes Percent of Total 0.8 3.2 4.6 4.9 5.0 12.1 10.9 24.3 14.7 6.2 13.8 100.0 1.0 3.9 5.3 5.4 5.4 12.7 11.1 24.0 14.0 5.7 11.9 100.0 0.2 0.7 2.1 3.1 3.8 10.2 10.0 25.3 16.8 7.6 20.1 100.0 Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-5). Number of AMT Taxpayers (millions). Baseline: 1.2 Proposal: 19.7 (1) Calendar year. Baseline is current policy (extension of the 2001-2003 tax cuts and patching AMT using 2009 parameters indexed for inflation) plus estate tax at current law level— a 55 percent top tax rate and a $1 million exemption, not indexed); top two tax brackets raised to 36 and 39.6 percent; restoration of the personal exemption phaseout (PEP) and the limitation on itemized deductions (Pease); increased tax rates on long-term capital gains (10 percent for tax units in 15 percent bracket, 20 percent for rest) and reduced rates for gains on assets held 5 years or longer; taxation of all dividends as ordinary income; removal of low- and middle-income tax cuts (eliminate the 10 percent bracket and increase the 25 and 28 percent tax rates to 28 and 31 percent; restore marriage penalties by setting the standard deduction and 10 and 15 percent tax brackets for couples filing jointly to 1.67 times those for singles and making the EITC phaseout threshold for couples filing jointly the same as that for singles; and repeal expansions of the student loan interest deduction, the Earned Income Tax Credit (EITC), the Child and Dependent Care Tax Credit (CDCTC), and the Child Tax Credit (CTC)). Policy is elimination of the AMT patch. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (4) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (5) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 21-Jul-10 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T10-0172 Incremental Effects of Allowing the 2001 and 2003 Tax Cuts to Sunset Eliminate AMT Patch Distribution of Federal Tax Change by Cash Income Level, 2012 1 Detail Table - Single Tax Units Cash Income Level (thousands of 2009 dollars) 2 Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All Percent of Tax Units 3 With Tax Increase With Tax Cut 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.1 0.5 2.1 4.1 9.6 30.3 17.6 13.9 1.4 Percent Change in After-Tax Income 4 0.0 0.0 0.0 0.0 0.0 -0.1 -0.1 -0.2 -0.3 0.0 0.0 -0.1 Share of Total Federal Tax Change 0.0 0.0 0.1 0.0 0.7 13.3 14.3 36.6 32.8 1.7 0.6 100.0 Average Federal Tax Change Dollars 0 0 0 0 2 24 64 174 669 203 123 23 Percent 0.0 0.0 0.0 0.0 0.0 0.2 0.3 0.5 0.8 0.1 0.0 0.2 Share of Federal Taxes Change (% Points) 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.1 0.0 0.0 0.0 Under the Proposal 0.9 3.0 6.0 7.3 8.3 18.4 11.9 18.1 9.9 4.4 11.7 100.0 5 Average Federal Tax Rate Change (% Points) 0.0 0.0 0.0 0.0 0.0 0.0 0.1 0.1 0.2 0.0 0.0 0.1 Under the Proposal 8.5 9.1 14.6 18.6 20.7 23.1 25.7 27.0 29.0 31.7 36.7 23.0 Baseline Distribution of Income and Federal Taxes by Cash Income Level, 2012 1 Cash Income Level (thousands of 2009 dollars) 2 Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All Tax Units 3 Number (thousands) Percent of Total 12,161 14,889 11,204 7,555 6,018 8,766 3,599 3,384 787 138 75 68,932 17.6 21.6 16.3 11.0 8.7 12.7 5.2 4.9 1.1 0.2 0.1 100.0 Average Income (Dollars) 5,710 15,384 25,667 36,120 46,555 63,234 89,193 137,406 300,163 697,814 2,972,435 43,878 Average Federal Tax Burden (Dollars) 484 1,400 3,748 6,727 9,623 14,596 22,897 36,982 86,447 220,775 1,090,704 10,064 Average AfterTax Income 4 (Dollars) 5,227 13,984 21,919 29,392 36,932 48,638 66,296 100,424 213,716 477,039 1,881,731 33,814 Average Federal Tax Rate 5 8.5 9.1 14.6 18.6 20.7 23.1 25.7 26.9 28.8 31.6 36.7 22.9 Share of PreTax Income Percent of Total Share of PostTax Income Percent of Total Share of Federal Taxes Percent of Total 2.3 7.6 9.5 9.0 9.3 18.3 10.6 15.4 7.8 3.2 7.3 100.0 2.7 8.9 10.5 9.5 9.5 18.3 10.2 14.6 7.2 2.8 6.0 100.0 0.9 3.0 6.1 7.3 8.4 18.4 11.9 18.0 9.8 4.4 11.8 100.0 Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-5). (1) Calendar year. Baseline is current policy (extension of the 2001-2003 tax cuts and patching AMT using 2009 parameters indexed for inflation) plus estate tax at current law level— a 55 percent top tax rate and a $1 million exemption, not indexed); top two tax brackets raised to 36 and 39.6 percent; restoration of the personal exemption phaseout (PEP) and the limitation on itemized deductions (Pease); increased tax rates on long-term capital gains (10 percent for tax units in 15 percent bracket, 20 percent for rest) and reduced rates for gains on assets held 5 years or longer; taxation of all dividends as ordinary income; removal of low- and middle-income tax cuts (eliminate the 10 percent bracket and increase the 25 and 28 percent tax rates to 28 and 31 percent; restore marriage penalties by setting the standard deduction and 10 and 15 percent tax brackets for couples filing jointly to 1.67 times those for singles and making the EITC phaseout threshold for couples filing jointly the same as that for singles; and repeal expansions of the student loan interest deduction, the Earned Income Tax Credit (EITC), the Child and Dependent Care Tax Credit (CDCTC), and the Child Tax Credit (CTC)). Policy is elimination of the AMT patch. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (4) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (5) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 21-Jul-10 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T10-0172 Incremental Effects of Allowing the 2001 and 2003 Tax Cuts to Sunset Eliminate AMT Patch Distribution of Federal Tax Change by Cash Income Level, 2012 1 Detail Table - Married Tax Units Filing Jointly Cash Income Level (thousands of 2009 dollars) 2 Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All Percent of Tax Units 3 With Tax Increase With Tax Cut 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.1 1.6 9.3 33.6 43.0 64.7 23.0 14.7 23.6 Percent Change in After-Tax Income 4 0.0 0.0 0.0 0.0 0.0 -0.1 -0.7 -0.8 -1.0 -0.1 0.0 -0.5 Share of Total Federal Tax Change 0.0 0.0 0.0 0.0 0.1 2.4 15.1 44.2 36.3 1.6 0.4 100.0 Average Federal Tax Change Dollars 0 0 0 0 5 75 506 836 2,253 557 256 500 Percent 0.0 0.0 0.0 0.0 0.1 0.7 2.9 2.5 2.9 0.3 0.0 1.6 Share of Federal Taxes Change (% Points) 0.0 0.0 0.0 0.0 0.0 -0.1 0.1 0.2 0.3 -0.1 -0.4 0.0 Under the Proposal 0.0 0.1 0.5 0.9 1.3 5.6 8.7 29.3 20.8 9.1 23.5 100.0 5 Average Federal Tax Rate Change (% Points) 0.0 0.0 0.0 0.0 0.0 0.1 0.6 0.6 0.8 0.1 0.0 0.4 Under the Proposal 5.3 3.4 7.0 10.3 12.9 16.4 19.9 24.1 27.1 28.0 33.3 24.5 Baseline Distribution of Income and Federal Taxes by Cash Income Level, 2012 1 Cash Income Level (thousands of 2009 dollars) 2 Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All Tax Units 3 Number (thousands) Percent of Total 2,172 4,097 4,842 4,391 4,095 9,883 9,149 16,193 4,941 876 435 61,357 3.5 6.7 7.9 7.2 6.7 16.1 14.9 26.4 8.1 1.4 0.7 100.0 Average Income (Dollars) 4,766 16,031 25,959 36,302 46,760 65,241 90,792 142,545 295,420 706,519 3,075,014 126,020 Average Federal Tax Burden (Dollars) 251 551 1,817 3,720 6,015 10,600 17,560 33,529 77,696 197,349 1,025,038 30,417 Average AfterTax Income 4 (Dollars) 4,516 15,480 24,142 32,583 40,745 54,641 73,232 109,016 217,724 509,170 2,049,976 95,603 Average Federal Tax Rate 5 5.3 3.4 7.0 10.3 12.9 16.3 19.3 23.5 26.3 27.9 33.3 24.1 Share of PreTax Income Percent of Total Share of PostTax Income Percent of Total Share of Federal Taxes Percent of Total 0.1 0.9 1.6 2.1 2.5 8.3 10.7 29.9 18.9 8.0 17.3 100.0 0.2 1.1 2.0 2.4 2.8 9.2 11.4 30.1 18.3 7.6 15.2 100.0 0.0 0.1 0.5 0.9 1.3 5.6 8.6 29.1 20.6 9.3 23.9 100.0 Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-5). (1) Calendar year. Baseline is current policy (extension of the 2001-2003 tax cuts and patching AMT using 2009 parameters indexed for inflation) plus estate tax at current law level— a 55 percent top tax rate and a $1 million exemption, not indexed); top two tax brackets raised to 36 and 39.6 percent; restoration of the personal exemption phaseout (PEP) and the limitation on itemized deductions (Pease); increased tax rates on long-term capital gains (10 percent for tax units in 15 percent bracket, 20 percent for rest) and reduced rates for gains on assets held 5 years or longer; taxation of all dividends as ordinary income; removal of low- and middle-income tax cuts (eliminate the 10 percent bracket and increase the 25 and 28 percent tax rates to 28 and 31 percent; restore marriage penalties by setting the standard deduction and 10 and 15 percent tax brackets for couples filing jointly to 1.67 times those for singles and making the EITC phaseout threshold for couples filing jointly the same as that for singles; and repeal expansions of the student loan interest deduction, the Earned Income Tax Credit (EITC), the Child and Dependent Care Tax Credit (CDCTC), and the Child Tax Credit (CTC)). Policy is elimination of the AMT patch. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (4) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (5) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 21-Jul-10 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T10-0172 Incremental Effects of Allowing the 2001 and 2003 Tax Cuts to Sunset Eliminate AMT Patch Distribution of Federal Tax Change by Cash Income Level, 2012 1 Detail Table - Head of Household Tax Units Cash Income Level (thousands of 2009 dollars) 2 Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All Percent of Tax Units 3 With Tax Increase With Tax Cut 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 3.5 17.1 43.1 68.5 64.1 74.1 18.2 16.3 15.1 Percent Change in After-Tax Income 4 0.0 0.0 0.0 0.0 -0.3 -0.9 -1.3 -1.1 -1.0 0.0 0.0 -0.5 Share of Total Federal Tax Change 0.0 0.0 0.0 1.0 7.0 35.0 28.2 21.6 7.0 0.1 0.0 100.0 Average Federal Tax Change Dollars 0 0 0 13 132 450 929 1,127 2,132 167 184 186 Percent 0.0 0.0 0.0 0.3 1.7 3.7 4.8 3.5 2.9 0.1 0.0 2.8 Share of Federal Taxes Change (% Points) 0.0 0.1 -0.1 -0.3 -0.1 0.2 0.3 0.1 0.0 -0.1 -0.2 0.0 Under the Proposal -0.8 -2.2 3.8 10.4 11.5 26.7 17.0 17.5 6.9 2.6 6.6 100.0 5 Average Federal Tax Rate Change (% Points) 0.0 0.0 0.0 0.0 0.3 0.7 1.0 0.9 0.7 0.0 0.0 0.5 Under the Proposal -7.7 -4.8 5.1 12.7 16.7 19.8 22.8 25.0 25.9 26.7 34.2 16.2 Baseline Distribution of Income and Federal Taxes by Cash Income Level, 2012 1 Cash Income Level (thousands of 2009 dollars) 2 Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All Tax Units 3 Number (thousands) Percent of Total 2,483 5,029 4,757 3,767 2,449 3,559 1,389 877 150 24 11 24,547 10.1 20.5 19.4 15.4 10.0 14.5 5.7 3.6 0.6 0.1 0.0 100.0 Average Income (Dollars) 6,647 15,579 25,971 36,157 46,569 63,082 89,214 132,993 294,130 686,382 2,985,055 41,760 Average Federal Tax Burden (Dollars) -514 -740 1,333 4,563 7,662 12,035 19,393 32,097 74,049 183,209 1,020,067 6,594 Average AfterTax Income 4 (Dollars) 7,161 16,319 24,639 31,594 38,908 51,047 69,820 100,896 220,081 503,173 1,964,988 35,166 Average Federal Tax Rate 5 -7.7 -4.8 5.1 12.6 16.5 19.1 21.7 24.1 25.2 26.7 34.2 15.8 Share of PreTax Income Percent of Total Share of PostTax Income Percent of Total Share of Federal Taxes Percent of Total 1.6 7.6 12.1 13.3 11.1 21.9 12.1 11.4 4.3 1.6 3.2 100.0 2.1 9.5 13.6 13.8 11.0 21.1 11.2 10.3 3.8 1.4 2.5 100.0 -0.8 -2.3 3.9 10.6 11.6 26.5 16.6 17.4 6.9 2.7 6.8 100.0 Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-5). (1) Calendar year. Baseline is current policy (extension of the 2001-2003 tax cuts and patching AMT using 2009 parameters indexed for inflation) plus estate tax at current law level— a 55 percent top tax rate and a $1 million exemption, not indexed); top two tax brackets raised to 36 and 39.6 percent; restoration of the personal exemption phaseout (PEP) and the limitation on itemized deductions (Pease); increased tax rates on long-term capital gains (10 percent for tax units in 15 percent bracket, 20 percent for rest) and reduced rates for gains on assets held 5 years or longer; taxation of all dividends as ordinary income; removal of low- and middle-income tax cuts (eliminate the 10 percent bracket and increase the 25 and 28 percent tax rates to 28 and 31 percent; restore marriage penalties by setting the standard deduction and 10 and 15 percent tax brackets for couples filing jointly to 1.67 times those for singles and making the EITC phaseout threshold for couples filing jointly the same as that for singles; and repeal expansions of the student loan interest deduction, the Earned Income Tax Credit (EITC), the Child and Dependent Care Tax Credit (CDCTC), and the Child Tax Credit (CTC)). Policy is elimination of the AMT patch. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (4) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (5) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 21-Jul-10 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T10-0172 Incremental Effects of Allowing the 2001 and 2003 Tax Cuts to Sunset Eliminate AMT Patch Distribution of Federal Tax Change by Cash Income Level, 2012 1 Detail Table - Tax Units with Children Cash Income Level (thousands of 2009 dollars) 2 Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All Percent of Tax Units With Tax Cut 3 With Tax Increase 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.1 3.4 13.8 32.0 64.3 71.2 78.2 19.8 10.8 32.0 Percent Change in After-Tax Income 4 0.0 0.0 0.0 0.0 -0.3 -0.6 -1.3 -1.3 -1.4 -0.1 0.0 -0.8 Share of Total Federal Tax Change 0.0 0.0 0.0 0.2 1.4 7.9 19.0 43.8 26.9 0.7 0.1 100.0 Average Federal Tax Change Dollars 0 0 0 14 107 316 962 1,391 2,902 459 123 603 Percent 0.0 0.0 0.0 0.3 1.5 2.7 5.2 4.1 3.7 0.2 0.0 2.7 Share of Federal Taxes Change (% Points) 0.0 0.0 0.0 0.0 0.0 0.0 0.2 0.4 0.2 -0.2 -0.5 0.0 Under the Proposal -0.2 -0.7 0.4 1.8 2.6 8.1 10.2 29.3 20.1 8.3 19.9 100.0 Average Federal Tax Rate 5 Change (% Points) 0.0 0.0 0.0 0.0 0.2 0.5 1.1 1.0 1.0 0.1 0.0 0.6 Under the Proposal -11.3 -8.2 3.3 11.6 16.0 18.8 21.4 24.6 27.7 29.7 34.7 23.8 Baseline Distribution of Income and Federal Taxes 1 by Cash Income Level, 2012 Cash Income Level (thousands of 2009 dollars) 2 Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All Tax Units 3 Number (thousands) Percent of Total 2,968 5,639 5,683 4,891 3,849 7,425 5,841 9,319 2,750 441 206 49,155 6.0 11.5 11.6 10.0 7.8 15.1 11.9 19.0 5.6 0.9 0.4 100.0 Average Income (Dollars) 6,252 15,769 25,918 36,161 46,701 64,368 90,740 142,137 293,742 705,334 3,105,769 95,419 Average Federal Tax Burden (Dollars) -706 -1,288 847 4,187 7,354 11,770 18,473 33,633 78,458 209,179 1,077,910 22,061 Average AfterTax Income 4 (Dollars) 6,958 17,057 25,071 31,974 39,346 52,598 72,267 108,505 215,284 496,155 2,027,859 73,359 Average Federal Tax Rate 5 Share of PreTax Income Percent of Total Share of PostTax Income Percent of Total Share of Federal Taxes Percent of Total -11.3 -8.2 3.3 11.6 15.8 18.3 20.4 23.7 26.7 29.7 34.7 23.1 0.4 1.9 3.1 3.8 3.8 10.2 11.3 28.2 17.2 6.6 13.7 100.0 0.6 2.7 4.0 4.3 4.2 10.8 11.7 28.0 16.4 6.1 11.6 100.0 -0.2 -0.7 0.4 1.9 2.6 8.1 10.0 28.9 19.9 8.5 20.5 100.0 Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-5). Note: Tax units with children are those claiming an exemption for children at home or away from home. (1) Calendar year. Baseline is current policy (extension of the 2001-2003 tax cuts and patching AMT using 2009 parameters indexed for inflation) plus estate tax at current law level— a 55 percent top tax rate and a $1 million exemption, not indexed); top two tax brackets raised to 36 and 39.6 percent; restoration of the personal exemption phaseout (PEP) and the limitation on itemized deductions (Pease); increased tax rates on long-term capital gains (10 percent for tax units in 15 percent bracket, 20 percent for rest) and reduced rates for gains on assets held 5 years or longer; taxation of all dividends as ordinary income; removal of low- and middle-income tax cuts (eliminate the 10 percent bracket and increase the 25 and 28 percent tax rates to 28 and 31 percent; restore marriage penalties by setting the standard deduction and 10 and 15 percent tax brackets for couples filing jointly to 1.67 times those for singles and making the EITC phaseout threshold for couples filing jointly the same as that for singles; and repeal expansions of the student loan interest deduction, the Earned Income Tax Credit (EITC), the Child and Dependent Care Tax Credit (CDCTC), and the Child Tax Credit (CTC)). Policy is elimination of the AMT patch. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (4) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (5) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 21-Jul-10 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T10-0172 Incremental Effects of Allowing the 2001 and 2003 Tax Cuts to Sunset Eliminate AMT Patch Distribution of Federal Tax Change by Cash Income Level, 2012 1 Detail Table - Elderly Tax Units Cash Income Level (thousands of 2009 dollars) 2 Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All Percent of Tax Units With Tax Cut 3 With Tax Increase 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.1 0.2 1.3 4.4 9.4 41.7 31.3 21.0 3.4 Percent Change in After-Tax Income 4 0.0 0.0 0.0 0.0 0.0 0.0 -0.1 -0.2 -0.5 -0.2 0.0 -0.1 Share of Total Federal Tax Change 0.0 0.0 0.0 0.1 0.1 2.1 5.4 22.3 60.1 8.1 2.0 100.0 Average Federal Tax Change Dollars 0 0 0 0 1 11 50 171 1,224 754 339 75 Percent 0.0 0.0 0.0 0.0 0.0 0.1 0.4 0.6 1.6 0.4 0.0 0.5 Share of Federal Taxes Change (% Points) 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.2 0.0 -0.1 0.0 Under the Proposal 0.1 0.6 1.4 1.6 1.9 7.3 7.6 19.3 19.4 10.5 30.2 100.0 Average Federal Tax Rate 5 Change (% Points) 0.0 0.0 0.0 0.0 0.0 0.0 0.1 0.1 0.4 0.1 0.0 0.1 Under the Proposal 3.2 2.8 5.1 6.8 8.3 12.0 15.7 21.2 26.3 27.9 34.3 20.1 Baseline Distribution of Income and Federal Taxes 1 by Cash Income Level, 2012 Cash Income Level (thousands of 2009 dollars) 2 Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All Tax Units 3 Number (thousands) Percent of Total 2,305 6,471 5,084 2,999 2,259 4,405 2,504 2,986 1,128 245 132 30,543 7.6 21.2 16.7 9.8 7.4 14.4 8.2 9.8 3.7 0.8 0.4 100.0 Average Income (Dollars) 6,366 15,655 25,560 36,054 46,537 64,489 89,136 141,589 304,121 709,954 3,095,895 75,737 Average Federal Tax Burden (Dollars) 201 432 1,313 2,440 3,880 7,699 13,944 29,909 78,835 197,391 1,062,418 15,130 Average AfterTax Income 4 (Dollars) 6,166 15,222 24,247 33,614 42,657 56,791 75,191 111,681 225,286 512,563 2,033,477 60,607 Average Federal Tax Rate 5 3.2 2.8 5.1 6.8 8.3 11.9 15.6 21.1 25.9 27.8 34.3 20.0 Share of PreTax Income Percent of Total Share of PostTax Income Percent of Total Share of Federal Taxes Percent of Total 0.6 4.4 5.6 4.7 4.5 12.3 9.7 18.3 14.8 7.5 17.7 100.0 0.8 5.3 6.7 5.5 5.2 13.5 10.2 18.0 13.7 6.8 14.5 100.0 0.1 0.6 1.4 1.6 1.9 7.3 7.6 19.3 19.2 10.5 30.4 100.0 Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-5). Note: Elderly tax units are those with either head or spouse (if filing jointly) age 65 or older. (1) Calendar year. Baseline is current policy (extension of the 2001-2003 tax cuts and patching AMT using 2009 parameters indexed for inflation) plus estate tax at current law level— a 55 percent top tax rate and a $1 million exemption, not indexed); top two tax brackets raised to 36 and 39.6 percent; restoration of the personal exemption phaseout (PEP) and the limitation on itemized deductions (Pease); increased tax rates on long-term capital gains (10 percent for tax units in 15 percent bracket, 20 percent for rest) and reduced rates for gains on assets held 5 years or longer; taxation of all dividends as ordinary income; removal of low- and middle-income tax cuts (eliminate the 10 percent bracket and increase the 25 and 28 percent tax rates to 28 and 31 percent; restore marriage penalties by setting the standard deduction and 10 and 15 percent tax brackets for couples filing jointly to 1.67 times those for singles and making the EITC phaseout threshold for couples filing jointly the same as that for singles; and repeal expansions of the student loan interest deduction, the Earned Income Tax Credit (EITC), the Child and Dependent Care Tax Credit (CDCTC), and the Child Tax Credit (CTC)). Policy is elimination of the AMT patch. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (4) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (5) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income.