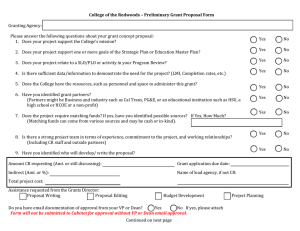

Document 14484084

advertisement