HOW CAN I BE A BETTER HEALTHCARE CONSUMER? MOTT COMMUNITY COLLEGE Chadd Hodkinson

advertisement

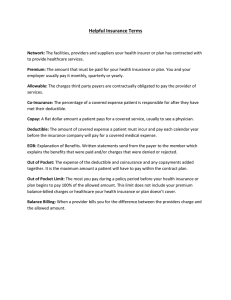

HOW CAN I BE A BETTER HEALTHCARE CONSUMER? MOTT COMMUNITY COLLEGE Chadd Hodkinson SET SEG Employee Benefit Services Senior Benefit Consultant The content in this presentation is informational. Each employee should review the benefit summary and network information specific to their plan and discuss specific circumstances and questions with their carrier. TOPICS OF DISCUSSION • What makes a wise healthcare consumer? • Why should I become a wise healthcare consumer? • How can I become a wise healthcare consumer? • What resources are available to me? WHAT MAKES A WISE HEALTHCARE CONSUMER? Wise Healthcare Consumers: • Know how to choose a healthcare plan to fit their family • Choose their care providers carefully • Ask questions about procedures • Practice preventative care • Understand their prescriptions • Review bills and EOBs WHY SHOULD I BE A WISE HEALTHCARE CONSUMER? • Control your healthcare costs • When members… o engage in conversations with their doctors o access in-network doctors/facilities o ask questions before partaking in expensive medical procedures …they can save money HOW CAN I BECOME A WISE HEALTHCARE CONSUMER? • Educate Yourself o Make more conscientious healthcare decisions • Put in Effort o Become more engaged with your healthcare IN-NETWORK DOCTORS AND FACILITIES • In-network providers have agreed to see patients at lower, negotiated rates of service, saving you money • Out of pocket costs (deductible, coinsurance, copayments) are lower when visiting an in-network doctor or facility MAKING THE MOST OUT OF DOCTOR VISITS • According to a study by UCLA, patients usually have questions, but ask them less than 10% of the time • Before you see a provider, prepare a list of questions about: o o o o o Symptoms Diagnosis Treatments Medications Testing MAKING THE MOST OUT OF DOCTOR VISITS Be able to describe your symptoms. • Describe your problem • Are you in pain? • When did the problem start? Has it changed since then? • What makes it go away? • Have you felt like this before? If so, when? • Have you had any other symptoms (e.g., fever, shortness of breath, insomnia, nausea) MAKING THE MOST OUT OF DOCTOR VISITS Ask questions about your diagnosis. • How certain are you about this diagnosis? Are there additional symptoms to look for? • Will this diagnosis increase my risk for other conditions? If so, are they preventable? • Is my condition chronic or acute? • Is my condition contagious? MAKING THE MOST OUT OF DOCTOR VISITS Ask questions about your treatment. • Why would this treatment be good for me? What are the chances it will work? • How much will this treatment cost? • Will this treatment cause any side effects? • Are there other treatment options? MAKING THE MOST OUT OF DOCTOR VISITS Ask questions about your prescription medication. • What will this medicine do? • When, how often, and for how long should I take it? • Could there be side effects? What should I do if they occur? • Is this medicine OK to take with other medications? • Is there anything I shouldn't do while taking the medicine? • Is there a less-expensive, generic equivalent? MAKING THE MOST OUT OF DOCTOR VISITS Ask questions about your test. • How will this test tell what is wrong? • How accurate is the test? • Is the test invasive or non-invasive? • Where will I go for the test? • How and when will I get the test results? • Will more tests be needed? • Is this test necessary? If so, why? MAKING THE MOST OUT OF DOCTOR VISITS Provide as much background information as possible. • Medical history and your family's medical history • Allergies • Medications you’re taking • Daily habits (e.g., how much you sleep, whether or not you smoke) • Occupation • Pressures/stress HIGH DEDUCTIBLE HEALTH PLANS (HDHP) • Have a deductible of at least $1,300 for a single person and $2,600 for a couple or family • Employee pays 100% (except for preventive care) of medical and prescription drug costs (less any carrier discounts) until deductible is met • Copays do not apply until deductible is met HIGH DEDUCTIBLE HEALTH PLANS (HDHP) • HDHPs encourage member engagement and awareness of costs • Employees generally look for ways to decrease their own healthcare spending • HDHPs can help generate discussion between members and health care providers HIGH DEDUCTIBLE HEALTH PLANS (HDHP) • Monthly premiums are typically far less than a traditional plan • Premium savings can be contributed tax free to a health savings account (HSA) • In years when less healthcare is needed, savings stay with the member • In years when more healthcare is needed, overall spending (premium cost share and deductible/copays) is generally less than with a traditional plan HEALTH SAVINGS ACCOUNT (HSA) • The account and its contents belong to you (not your employer) • Rolls over year after year (no “use it or lose it”) • Fully portable should you decide to leave the high deductible plan or the college • Accessible in retirement HEALTH SAVINGS ACCOUNT (HSA) • Money goes in tax free, can grow tax free and comes out tax free (if spent on approved medical expenses) • Can save 25% or more on medical expenses if HSA contributions are made through payroll deductions (Use on dental or vision expenses to increase overall savings) • Cannot contribute to an HSA if enrolled in a nonqualified health plan (including Medicare) EMERGENCY ROOM, URGENT CARE OR PRIMARY CARE? • Know when to seek medical care at the ER, Urgent Care or through your primary care physician • Seeing a primary care physician is substantially cheaper than visiting an Urgent Care or ER • If you think it might be an emergency, go to the emergency room! PRIMARY CARE URGENT CARE PRIMARY CARE, URGENT CARE & EMERGENCY CARE?Typical business Hours Typical business hours: 9 a.m. – 5 p.m. Accessibility Typically by appointment Uses hours, but also weeknights and weekends Walk-In or by appointment Acute illness Checkups, physicals, illnesses that can wait (rapid onset and short duration; regulated with for an appointment OTC prescriptions) EMERGENCY 24/7 Walk-In Threat to life or limb SAMPLE COSTS: Urgent Care Emergency Room Acute bronchitis: $127 Acute Bronchitis: $595 Earache: $110 Earache: $400 Sore throat: $94 Sore throat: $525 Sinusitis: $112 Sinusitis: $617 Upper respiratory infection: $111 Upper respiratory infection: $486 PREVENTIVE SERVICES • Approved services are covered at 100% for plan enrollees with no deductible or copay liability (no enrollee out of pocket cost) • Services must be received in-network o Ex: annual physicals, well baby check-ups, some immunizations, etc. • Confirm with carrier that scheduled services are preventive MANAGE CHRONIC CONDITIONS • Although it’s not considered preventive, it is often less costly to manage a condition rather than to treat an unmanaged condition • Learning to control your condition can help you: o o o o Improve your quality of life Save money Avoid disability Prevent untimely death PRESCRIPTION MEDICATION MANAGEMENT • Talking to your doctor about generic alternatives can save large amounts of money • If it is determined by your doctor that the name brand will work best for your condition, prior authorization may be required PRESCRIPTION MEDICATION MANAGEMENT • • • • Always ask for a generic medicine Remind pharmacy to use prescription card Ask pharmacy if the claim went through Blue Cross Ask doctor for a 90 day prescription for maintenance drugs • The majority of Tier 3 drugs have a less expensive alternative or equivalent in Tier 1 & Tier 2 PROVIDER BILLS AND EXPLANATION OF BENEFITS (EOBs) • Medical billing is complicated and mistakes happen • Review your bills as they come in from providers to make sure services you were charged for were rendered • Contact the provider if you believe there is an error • Compare the charges and member responsibility on your bill to the amounts listed on your EOBs PROVIDER BILLS AND EXPLANATION OF BENEFITS (EOBs) • Your EOB is a window into your medical billing history • Review EOBs carefully to make sure: o you received the service you’re being billed for o the amount your doctor received and your share are correct o your diagnosis and procedure are correctly listed and coded HOW TO READ A PROVIDER BILL • Ensure your insurance is on file/was applied • Ensure services you were charged for were services you received • Find your patient responsibility total • Find out where you can pay • Locate a customer service number if you have questions or find an error Ensure insurance is on file/was applied Find your patient responsibility total Find out where to pay provider Ensure services you were charged for were services you received Contact customer service if you have a question or there is an error HOW TO READ AN EXPLANATION OF BENEFITS (EOB) • Ensure your personal information is correct to avoid processing errors • Compare charges on an individual basis • Make sure charges match bill provider has sent (date of service, services rendered and approved charges) • If you find an error, contact provider and/or Blue Cross EOB SAMPLE: EOB SAMPLE: EOB SAMPLE: EOB SAMPLE: EOB SAMPLE: EOB SAMPLE: WHAT RESOURCES ARE AVAILABLE? WWW.BCBSM.COM • • • • Online health assessment Informational resource library, calculators and quizzes Smoking cessation tools Blue Cross Blue Shield’s website also offers ratings and other information about providers and facilities Find out if Provider accepts your plan Compare ratings of Providers BLUE CROSS BLUE SHIELD OF MICHIGAN TRANSPARENCY TOOL WHAT RESOURCES ARE AVAILABLE? www.webmd.com • WebMD provides information on various conditions • Knowledge empowers you to ask your doctors questions about generic prescriptions, alternative therapies and recommended procedures after a diagnosis as been received Tools and Resources can aide in education General Overview for education WHAT RESOURCES ARE AVAILABLE? www.guroo.com • GuRoo allows members to price shop medical procedures • Provides national average pricing • Powered by the Health Care Cost Institute • Described as an independent, nonprofit organization oriented to provide honest, clear insight into health care costs WHAT RESOURCES ARE AVAILABLE? www.healthcarebluebook.com • Healthcare Blue Book also provides a tool for pricing surgeries, testing, medication and more • Provides local pricing • Partners with organizations and providers who strive to be transparent • Prices are based on information gathered from these partners Local prices of procedures Alternative options Healthcare Blue book offers a variety of services to price shop WHAT RESOURCES ARE AVAILABLE? www.ahrq.gov The Agency for Healthcare Research and Quality • educational videos • Question Builder for doctor visits • Health Priorities self-assessment and free printed materials http://www.healthylife.com/ The American Institute of Preventative Medicine • An authority on the development and implementation of health promotion, wellness, medical self-care, and disease management programs and publications QUESTIONS?