Document 14089804

advertisement

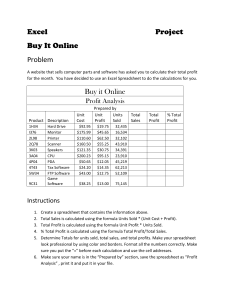

Participating in one or more of the Society’s 60 statewide committees is one of the most effective ways for you to practice and perfect your skills and knowledge while contributing to your profession. Committee service allows you to: Build leadership skills Network with peers and use your affiliation as an invaluable referral source Gain recognition for you and your organization Stay up to date on current issues Enhance your technical proficiency and career potential Serve your profession and community at large It’s simple to join a committee. Apply online at www.nysscpa.org and click on “Find Committees” on the homepage. Or contact Nereida Gomez, Senior Manager, Committee Services, at 212-719-8358 or ngomez@nysscpa.org. NYSSCPA new york state society of Publisher LOUIS GRUMET Editor-in-Chief MARY-JO KRANACHER, MBA, CPA, CFE Associate Publisher JOANNE S. BARRY Managing Editor CAROLYN MORRISROE Art Director LARRY MATTHEWS Associate Editor ANTHONY H. SARMIENTO Senior Designer ERNESTO LARA Editorial Assistant DIANA CARBONELL Copyeditors/Proofreaders GENE CIOFFI KEITH PLANIT Subscriptions (800) 877-4522 or (212) 719-8312 Advertising Account Executives EXECUTIVE PUBLISHING (410) 893-8003 Fax: (410) 893-8004 General Information (212) 719-8300 MOLLY DEISE mdeise@executivepublishing.com http://www.cpaj.com E-mail: cpaj@nysscpa.org KATIE GRIBBIN katieg@executivepublishing.com The CPA Journal welcomes the submission of articles on a wide variety of topics of interest to CPAs in public practice, industry, education, and government. Articles are evaluated on the basis of the clarity of ideas and writing, contribution to the profession, relevance, benefit to practitioners, and soundness of point of view. Manuscripts deemed to have potential for publication are reviewed by two referees prior to acceptance for publication. See www.cpaj.com/guidelines. htm for more detailed information. Classified Advertising SALES DESK (410) 893-8003 mdeise@executivepublishing.com katieg@executivepublishing.com THE CPA JOURNAL EDITORIAL BOARD Susan B. Anders Neal B. Hitzig Vincent J. Love C. Richard Baker Ronald J. Huefner Nicholas J. Mastracchio, Jr. Edwin B. Morris William Bregman Peter A. Karl III Thomas Buckhoff Laurence Keiser Bruce Nearon Douglas R. Carmichael Stuart Kessler Raymond M. Nowicki Rona L. Cherno Jerome Landau Paul A. Pacter Robert A. Dyson Joel Lanz Lawrence A. Pollack Arthur Siegel Andrew Fair Mark H. Levin Julie Lynn Floch Michele Mark Levine Lynn Turner Dan L. Goldwasser Martin Lieberman Elizabeth K. Venuti Kenneth J. Gralak David A. Lifson George I. Victor Neville Grusd Steve Lilien Paul D. Warner Elliot L. Hendler Steve Loeb Robert N. Waxman certified public accountants THE CPA JOURNAL (ISSN 0732-8435, USPS 049-970) is published monthly by The New York State Society of Certified Public Accountants, 3 Park Avenue, New York, NY 10016-5991. Copyright 2010 by The New York State Society of Certified Public Accountants. Subscription rates: NYSSCPA Members (Basic Rate): $15.00. Non-members, United States possessions, Canada, one year $42.00; Students (Undergraduate and Graduate) $21.00; Foreign $54.00; Single copy $5.00. All subscriptions and remittances may be sent in United States funds to The CPA Journal, P. O. Box 34701, Newark, NJ 07189-4701. • Periodicals postage paid at New York, NY and additional mailing offices. The matters contained in this publication, unless otherwise stated, are the statements and opinions of their authors and are not promulgations by the Society. Publishers Copy Protection Clause: Advertisers and advertising agencies assume liability for all content (including text, representation, and illustrations) herefrom made against the publisher. POSTMASTER: Please send address changes to: The CPA Journal, 3 Park Avenue, New York, NY 10016-5991, Attn: Subscription Department. The CPA Journal is a registered trademark of The New York State Society of CPAs. T E C H N O L O G Y electronic reporting Using XBRL to Analyze Financial Statements A Step-by-Step Spreadsheet Guide By Thomas Tribunella and Heidi Tribunella A ccounting and financial data has long been contained in paper documents, but it is now possible to identify, transfer, and store financial information electronically. XML (Extensible Markup Language) and XBRL (Extensible Business Reporting Language) can give us the ability to tag specific pieces (elements) of financial information so they can be used and reused in a variety of reports. XBRL is a text and data markup language similar to HTML (Hyper Text Markup Language), created in the metalanguage of XML. XBRL allows content such as financial statement elements to be electronically labeled with conceptual tags. The discussion below will demonstrate how to use XBRL data with a spreadsheet for financial analysis. It will show how XBRL data can be easily updated in the spreadsheet as new financial data becomes available. Both Microsoft Office versions 2003 and 2007 are XML compliant, as are most databases, accounting systems, and enterprise systems. This means that these systems can automatically tag and export data and information in XML format. Accordingly, this information can be imported into another application, such as a spreadsheet, for analysis. In addition, XML-compliant documents can be posted directly to the Internet for display, as most web browsers can read XML documents. Step 1: Prepare the Spreadsheet The steps outlined below use Microsoft Excel 2007. Before starting the procedures outlined in this article, make sure that you have the developer tab displayed. If it is not displayed, simply click on the Microsoft Office Button in the top left corner and then choose “Excel Options” from MARCH 2010 / THE CPA JOURNAL the drop down menu. In the dialog box, under “Top options for working with Excel,” check the third box, “Show Developer tab in the Ribbon,” and then click “OK.” Step 2: Identify the Company and Report This example uses the financial statements from Adobe Systems Inc., specifically its Form 10-Q for the quarter ended August 29, 2008. To download the financial statements as a PDF for use as a reference while devel- oping the sample spreadsheet, go to www.sec.gov. Click on “Search” in the upper right corner. In the “Search Company Filings” pane on the left, enter Adobe into the “Company name” field and click on “Find Companies.” As the example uses Adobe Systems Inc., click on CIK number 0000796343 to see the filings. Scroll down to the 10-Q filing dated 2008-10-02 and click on the “Documents” button. From the resulting list, click on the file “form10qunofficial_ pdf.pdf.” 69 Pages 1 to 5 of the 10-Q of the PDF can be used as a reference. top or other desired location. Refer to Exhibit 1. Step 3: Download the XBRL Report Step 4: Open the XML Source within an Excel Spreadsheet To download the XBRL-compliant report from the SEC for 10-Q, follow the steps above. Then, look down the list of documents, below the PDF, and right-click the XBRL Instance Document file named “adbe-20080916.xml.” Choose “Save Target As …” and save the file to the desk- The next step is to integrate the tagged data source into the spreadsheet. To access the tagged data, complete the following procedures: ■ From within Microsoft Excel, open the XML file downloaded in step 3. EXHIBIT 1 File Download ■ Excel will recognize the file as an XML file, and an “Open XML” dialog box will appear. Select “Use the XML Source task pane” and click “OK.” A dialog box that states: “The specified XML source does not refer to a schema. Excel will create a schema based on the XML source data” will then appear. The user should click “OK.” The tagged data will be shown in a sidebar of the Excel spreadsheet. Excel has created a taxonomy of tags from the structured XML-compliant document. Step 5: Determine the Output Information and Identify the Input Data With the data in hand, a user can determine whatever information is needed, such as financial ratios, horizontal analysis, and vertical analysis. Four ratios will suffice to demonstrate the process. Exhibit 2 shows the input data and the related XBRL tags and cell locations. After the data needs are determined, a user can work on importing the input data to produce the output information. Input data should only be entered once. Step 6: Map the XBRL Tags into the Input Section EXHIBIT 2 Input Data Excel Input Cell XBRL Tag Name Value in Thousands B3 ns3:CashAndCashEquivalentsAtCarryingValue 1,134,263 B9 ns3:ShortTermInvestments 866,641 B13 ns3:AccountsReceivableNetCurrent 327,970 B17 ns3:AssetsCurrent 2,517,120 B21 ns3:LiabilitiesCurrent 661,663 E3 ns3:Revenues 887,257 E9 ns3:GrossProfit 776,406 E15 ns3:NetIncomeLoss 191,608 70 Once all of the XBRL tags are shown in the source task pane, it is a simple process to map the data elements to the cells in the input data section of the spreadsheet. Two methods can be used to map the data: 1) click on the data element <value> and drag it to the target cell or 2) select the target cell on the spreadsheet and double-click on the data item <value> shown in the source task pane. Data elements can only be mapped to one cell; the same element cannot be mapped to two different cells. If the data is needed in more than one cell, simply add a formula (e.g., +A2) to put the data in a second cell. It may be helpful to show the actual numerical data in the XML Source task pane while mapping. To do so, simply click the “Options” menu on the bottom of the XML Source task pane and select “Preview Data in Source Pane.” Once mapped, the cell has a blue background, and in the source task pane, the data element is bolded to indicate it has already been mapped. When bringing the tags into the spreadsheet, the name of the tag is automatically placed above the MARCH 2010 / THE CPA JOURNAL data. To remove the tag names and use custom names, simply uncheck the “Header Row” box within the “Table Style Options” on the Design Tab. The input data required to calculate the desired output information in this example are: current assets, current liabilities, cash, short-term investments, accounts receivable, net income, sales, and gross profit. The following steps will include this data in the input section and program the cells in the output section to calculate the desired ratios: current ratio, quick ratio, profit margin, and gross profit margin. The data will appear in the spreadsheet cells once the import function is complete. When the data is imported, the financial statements are comparative, so the data will take up two rows for the balance sheet: one for the current year, listed first, and one for the prior year. The data will take up four rows on the income statement, as four columns appear on the Adobe income statement. Refer to Exhibit 3 for a view of the completed spreadsheet prior to importing the XML data. EXHIBIT 3 Spreadsheet View Prior to Import of Data Step 7: Populate the Spreadsheet by Importing the Data Once the spreadsheet is mapped and labeled, it is time to import the data. The authors have found that it is easier to enter the formulas for the output section after the data has been imported. To do so, simply place the cursor in any cell. Click on the “Developer Tab” and then click “Import.” An XML Import dialog box will appear. Select the file with the XML data in it and click “Import.” The data will be pulled into the spreadsheet cells. See Exhibit 4 for a screenshot of an Excel spreadsheet with the imported XMLcompliant data. One can now format the data with commas and decimals, as well as place lines and borders as appropriate. Compare the data imported to the printout of the 10-Q to note that the imported data is comparative financial information. EXHIBIT 4 XML Data Imported Step 8: Create the Formulas At this point, the cell formulas can be entered into the output section of the spreadsheet. The Excel formulas and their related addresses are shown in Exhibit 5. The spreadsheet is organized with input and output sections so that changes MARCH 2010 / THE CPA JOURNAL 71 in the input data have no effect on the output information. As a result, the data can be updated quickly without re-creating the cell formulas. Exhibit 6 presents the completed spreadsheet, which includes the formatted data as well as formulas for the financial statement analysis. Step 9: Change the Input Section The real power of this technique comes from the ability to update the spread- sheet with additional data. To show this, download the next quarter’s 10-Q for Adobe Systems, the quarter ending February 28, 2009. It is under the filing date 2009-04-03 and has the file name of adbe-20090227.xml (see Step 2). Follow the instructions to import the data (Step 7). The data from this file can now be incorporated into the spreadsheet, and the financial statement ratios are automatically recalculated. EXHIBIT 5 Spreadsheet Formulas for Output Section Ratio Calculation Cell Excel Formula Current Ratio Current Assets Current Liabilities B27 =B18/B22 Quick Ratio (Acid Test) Cash + S.T. Investments + A.R. Current Liabilities B28 =(B4+B10+B14)/B22 Gross Profit Percentage (Gross Margin Ratio) Gross Profit Sales or Revenue B29 =E10/E4 Profit Margin Percentage (Return on Sales) Net Income Sales or Revenue B30 =E16/E4 EXHIBIT 6 Completed Spreadsheet Possibilities of Electronic Data SEC Chair Mary Schapiro recently announced that the EDGAR (Electronic Data Gathering and Retrieval) system will be replaced by a new system. EDGAR was developed in the 1980s to store public company filings, such as 10-Ks and 10-Qs. The EDGAR system is a textbased document system, which makes it difficult to retrieve individual pieces of data from the stored financial information. The SEC’s new IDEA (Interactive Data Electronic Applications) system will be data-based, allowing users to search and retrieve data items, such as revenue or retained earnings. The new IDEA system will place electronic XBRL tags around data items so that they can be efficiently searched and retrieved for financial analysis. Because XBRL and XML are open source systems, they are free of license fees. In addition, XBRL is extensible so companies can modify the basic taxonomy (with XML) to fit their needs. The uses of such technologies are numerous. Auditors can use these skills to quickly look at benchmarking data and use during analytical procedures within an engagement. This can also be helpful when analyzing companies as potential investment and acquisition targets. The advantages of XBRL are manifold. For example, automatic tagging of data and information is now available with accounting software, database, and enterprise systems. With XBRL, analysts can drill down to the transaction level from the financial reports. Another advantage is quicker and more periodic reporting capabilities, as well as real-time reporting and auditing. With the recent SEC mandate for the 500 largest publicly held companies to use XBRL, the data is there. Accordingly, CPAs must learn how to work with, and profit ❑ from, this new form of information. Thomas Tribunella, PhD, CPA, is an associate professor of accounting and information systems in the school of business, State University of New York at Oswego, Oswego, N.Y. Heidi Tribunella, MS, CPA, is a senior lecturer in accounting at the Simon Graduate School of Business Administration, University of Rochester, Rochester, N.Y. 72 MARCH 2010 / THE CPA JOURNAL