Document 12824813

advertisement

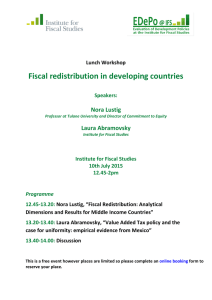

Fiscal Redistribu/on: Analy/cal Dimensions and Results for Middle Income Countries Nora Lus/g Tulane University, CGD, IAD Fiscal Redistribu/on in Developing Countries Ins/tute for Fiscal Studies London, UK July 10, 2015 OUTLINE • Brief descrip9on of CEQ project • Methodological highlights • Results – Middle-­‐income countries – Ethiopia Nora Lus9g 2 What is CEQ? Nora Lus9g What is CEQ: Descrip/on of Project § The CEQ project is an ini9a9ve of: • The Center for Inter-­‐American Policy and Research (CIPR) and the Department of Economics, Tulane University, Center for Global Development and the Inter-­‐American Dialogue § CEQ’s goals are to: • Foster evidence-­‐based policy discussion on fiscal redistribu9on • Assist governments, mul9lateral ins9tu9ons, and nongovernmental organiza9ons in their efforts to build more equitable socie9es Nora Lus9g 4 What is CEQ: Core Team § Director: Nora Lus9g § Technical Coordinator: Sean Higgins § Project Coordinator: Samantha Greenspun § Team: Rodrigo Aranda, Ali Enami, and Yang Wang § Advisory Board: list on CEQ homepage § Consultants: Jim Alm, Francois Bourguignon, Jean-­‐Yves Duclos, Peter Lambert, Anthony Shorrocks and Stephen Younger § Country teams: listed at the end of presenta9on Nora Lus9g 5 What is CEQ: Funding § Tulane University (2008 -­‐) • Center for Inter-­‐American Policy and Research • School of Liberal Arts • Stone Center for La9n American Studies § Bill & Melinda Gates Founda9on • CEQ Handbook (text, master workbook and ado files) • CEQ Assessments in Ghana and Tanzania § Canadian Interna9onal Development Agency (CIDA), the Norwegian Ministry of Foreign Affairs, and the General Electric Founda9on Nora Lus9g 6 What is CEQ: Partnerships and Collabora/ons § World Bank: 11 countries, background papers, joint papers, policy briefs and LEL (Equity Lab) § IDB: 10 countries in LAC, by ethnicity and race, overview papers for LA § ICEFI: 4 countries in Central America, rural-­‐urban § IFAD: 4 countries, rural-­‐urban § § UNDP: Ecuador (top incomes) and Venezuela Economic Research Forum: Egypt and Iran § AfDB: Tunisia § CADEP: Paraguay § CBGA: India § FUSADES: El Salvador § REPOA: Tanzania § University of Ghana: Ghana § OECD: chapter for flagship publica9on and project on redistribu9on and the middle-­‐class § IMF: chapter for edited volume § CAF: background paper § ADB: box for flagship publica9on § CEPAL: box for flagship publica9on Nora Lus9g 7 What is CEQ: Country Coverage § 33 countries at different stages of comple9on § Asia…………………… 4 § ECA…………………….3 § LAC……………………17 § MENA…………………4 § SSA……………………. 4 § United States § 17 CEQ Assessments have been completed Nora Lus9g 8 www.commitmentoequity.org Nora Lus9g 9 CEQ Assessment: Tools § Handbook: Lus9g and Higgins, current version Sept 2013; includes sample Stata code => available on CEQ website § Master Workbook: Excel Spreadsheet to present background informa9on, assump9ons and results. Lus9g and Higgins, version Feb 2015 (available with permission) § Diagnos/c Ques/onnaire: = > available on website § Ado Stata Files: (available with permission) § CEQ Handbook 2016 (forthcoming) Lus9g and Higgins, editors. Commitment to Equity Handbook: Es4ma4ng the Redistribu4ve Impact of Fiscal Policy Nora Lus9g 10 NEW! CEQ Ins/tute • Research-­‐based policy tools • CEQ database and informa9onal resources • Advisory and training services • Bridges to policy Nora Lus9g 11 Methodological Highlights: The Net Fiscal System, Inequality and Poverty Based on: Duclos & Araar (2006) Higgins & Lus9g (2015) Lambert (2001) Lus9g, Enami & Aranda (forthcoming) Lus9g & Higgins (2013) Nora Lus9g Fiscal Policy, Inequality and Poverty Main Ques/ons § Does the net fiscal system decrease inequality? § Is a par9cular fiscal interven9on equalizing or unequalizing? § Does the net fiscal system decrease poverty? § Does the net fiscal system make some of the poor poorer? Nora Lus9g What is the “net fiscal system”? In literature: § From market to disposable income: direct taxes and direct transfers § From market to consumable income: direct and indirect taxes, direct transfers and indirect subsidies § From market to extended disposable income: direct taxes and direct transfers plus valua9on of in-­‐kind services § From market to final income: direct and indirect taxes, direct transfers and indirect subsidies plus valua9on of in-­‐kind services Nora Lus9g 14 CEQ Assessment: Income Concepts MARKET INCOME PLUS DIRECT TRANSFERS MINUS DIRECT TAXES Net Fiscal System I DISPOSABLE INCOME PLUS INDIRECT SUBSIDIES MINUS INDIRECT TAXES Net Fiscal System II POST-­‐FISCAL or CONSUMABLE INCOME PLUS MONETIZED VALUE OF PUBLIC SERVICES: EDUCATION & HEALTH Net Fiscal System III FINAL INCOME Nora Lus9g 15 Main messages 1. Analyzing the tax without the spending side, or vice versa, is not really useful Ø Taxes can be unequalizing but spending so equalizing that the unequalizing effect of taxes is more than compensated Ø Taxes can be unequalizing by themselves but when combined with transfers make the system more equalizing than without the regressive taxes Nora Lus9g 16 Main messages 2. Analyzing the progressivity or regressivity of individual interven9ons can lead to the wrong conclusions about their contribu9on Ø Regressive taxes can exert an equalizing influence, under certain condi9ons which involve the size and progressivity of ALL fiscal interven/ons simultaneously ALSO Ø Progressive transfers in a system with progressive taxes can exert an unequalizing influence, under certain condi9ons which involve the size and progressivity of ALL fiscal interven/ons simultaneously Ø Regressive transfers in a system with regressive taxes can exert an equalizing influence, under certain condi9ons which involve the size and progressivity of ALL fiscal interven/ons simultaneously Nora Lus9g 17 Main messages 3. Analyzing the impact on inequality only can be misleading Ø Fiscal systems can be equalizing but poverty increasing Nora Lus9g 18 Main messages 4. Analyzing the impact on tradi9onal poverty indicators can be misleading Ø Fiscal systems can show a reduc9on in poverty for all possible poverty lines and yet a substan9al share of the poor could have been impoverished by the combined effect of taxes and transfers Nora Lus9g 19 Methodological Highlights: The Analy/cs of Fiscal Income Redistribu/on Based on Duclos & Araar (2006) Lambert (2001) Lus9g, Enami and Aranda (forthcoming) Nora Lus9g Main messages 1. Analyzing the tax without the spending side, or vice versa, is not really useful Ø Taxes can be unequalizing but spending so equalizing that the unequalizing effect of taxes is more than compensated Ø Taxes can be unequalizing by themselves but when combined with transfers make the system more equalizing than without the regressive taxes Nora Lus9g 21 Main messages 2. Analyzing the progressivity or regressivity of individual interven9ons can lead to the wrong conclusions about their contribu9on Ø Regressive taxes can exert an equalizing influence, under certain condi9ons which involve the size and progressivity of ALL fiscal interven/ons simultaneously Ø Progressive transfers in a system with progressive taxes can exert an unequalizing influence, under certain condi9ons which involve the size and progressivity of ALL fiscal interven/ons simultaneously Ø Regressive transfers in a system with regressive taxes can exert an equalizing influence, under certain condi9ons which involve the size and progressivity of ALL fiscal interven/ons simultaneously 22 Nora Lus9g Fiscal Policy and Inequality Four Key Ques/ons § Does the net fiscal system decrease inequality? § Is a par9cular tax or transfer equalizing or unequalizing? § What is the contribu9on of a par9cular tax or transfer (or any combina9on of them) to the change in inequality? § What is the inequality impact if one increases the size of a tax (transfer) or its progressivity? Nora Lus9g In a world with a single interven/on, the impact on inequality depends on… § Progressivity of a tax (transfer) § Size of the tax (transfer), where size equals the total tax (transfer) divided by total pre-­‐tax (pre-­‐transfer) income Ø A large regressive tax can be more equalizing than a small progressive one Nora Lus9g 24 Kakwani Index Ø Progressive Tax: Kt = CCt-­‐ Gx > 0 Ø Propor9onal Tax: Kt = CCt-­‐ Gx = 0 Ø Regressive Tax: Kt = CCt-­‐ Gx < 0 Nora Lus9g 25 Ø In a world with more than one interven9on, the one-­‐to-­‐one mapping from the combina9on of size and progressivity to the induced change in inequality breaks down Ø Will illustrate for the one-­‐tax-­‐one-­‐transfer case but results apply to m taxes and n transfers (Lus9g, Enami and Aranda, forthcoming) 26 Does the net fiscal system decrease inequality? Let’s&define&the&Redistributive&Effect&of&the&net&fiscal& system&as& ! !!"!! = !! − !! ! & Where&!! !!"#!!! !are&the&pre:tax:pre:transfer&Gini& coefficient&post:tax:post:transfer&Gini,&respectively& Nora Lus9g 27 Does the net fiscal system decrease inequality? From%Lambert%(2001),%we%know%that%!"!! !is%equal%to%the% weighted%sum%of%the%redistributive%effect%of%taxes%and% transfers% % ! − ! !"! + (! + !)!"! !"!! = ! !−!+! % Where%% • !"! !and%!"! %are% the% Redistributive% Effect% of% the% tax% and%the%transfer,%respectively%% • g%and%b:%size%of%tax%and%transfer,%respectively.%% That%is,%total%taxes%and%total%transfers%divided%by%total% preItax%and%preItransfer%income,%respectively% Nora Lus9g 28 Does the net fiscal system decrease inequality? Nora Lus9g 29 Does the net fiscal system decrease inequality? Tax Regressive 𝑲𝑻 < 0 Neutral 𝑲𝑻 = 𝟎 Progressive 𝑲𝑻 > 0 Nora Lus9g Regressive 𝑲𝑩 < 0 Transfer Neutral 𝑲𝑩 = 𝟎 Always Unequalizing Always Unequalizing Always Unequalizing No Change in Equality Always Equalizing Equalizing only if Condition 1 holds Always Equalizing Always Equalizing Progressive 𝑲𝑩 > 0 Equalizing only if Condition 1 holds 30 • The above result is well-­‐known in the literature: Ø A fiscal system with a regressive tax can be equalizing as long as transfers are progressive and the condi9on above is fulfilled Ø A fiscal system with a regressive tax that collects more revenues than a less regressive one may be more equalizing • However, Lambert’s equa9on has more fundamental implica9ons Nora Lus9g 31 Fiscal Policy and Inequality Four Key Ques/ons § Does the net fiscal system decrease inequality? § Is a par9cular tax or transfer equalizing or unequalizing? § What is the contribu9on of a par9cular tax or transfer (or any combina9on of them) to the change in inequality? § What is the inequality impact if one increases the size of a tax (transfer) or its progressivity? Nora Lus9g Is a par/cular tax or transfer equalizing? § If there is a single interven9on in the system, any of the progressivity measures discussed earlier will give an unambiguous answer § If there is a tax and a transfer (or more than one tax or one transfer), then this is no longer the case Ø A regressive tax can be equalizing in the sense that the reduc9on in inequality can be larger with the tax than without it Nora Lus9g 33 Lambert’s Conundrum 1 2 3 4 Total Original Income x 10 20 30 40 100 Tax t 6 9 12 15 42 Transfer B 21 14 7 0 42 Net Income N 25 25 25 25 100 Source: Lambert, 2001, Table 11.1, p. 278 Nora Lus9g 34 Lambert’s Conundrum § The Redistribu9ve Effect of the tax only in this example is equal to -­‐0.05, highligh9ng its regressivity § The Redistribu9ve Effect of the transfer is equal to 0.19 Ø Yet, the Redistribu9ve Effect of the net fiscal system is 0.25, higher than the effect without the taxes! Nora Lus9g 35 Lambert’s Conundrum 1 2 3 4 Total Original Income x 10 20 30 40 100 Transfer B 21 14 7 0 42 Post-­‐Transfer Income 31 34 37 40 142 Tax t 6 9 12 15 42 Net Income N 25 25 25 25 100 Source: Lambert, 2001, Table 11.1, p. 278 Nora Lus9g 36 Lambert’s Conundrum Path Dependency § If a tax is regressive vis-­‐à-­‐vis the original income but progressive with respect to the less unequally distributed post-­‐transfer income Ø Regressive taxes can exert an equalizing effect over an above the effect of progressive transfers Ø Note that ins9tu9onal path dependency is not the same as mathema9cal path dependency Nora Lus9g 37 When could a regressive tax exert an equalizing force? Nora Lus9g 38 Is a tax equalizing? Answer for a system with a tax and a transfer Regressive 𝑲𝑻 < 0 Adding Neutral a Tax 𝑲𝑻 = 𝟎 that is Progressive 𝑲𝑻 > 0 Nora Lus9g System with a Transfer that is Regressive Neutral Progressive 𝑲𝑩 < 0 𝑲𝑩 = 𝟎 𝑲𝑩 > 0 Always More Always More Equalizing Unequalizing Unequalizing only if Condition 2 Always More No Change in Always More Unequalizing Inequality Equalizing More Equalizing Always More Always Equalizing only if Condition 2 Equalizing 39 Equalizing Regressive Taxes Exist in Real Life § The US and the UK had regressive equalizing taxes in the past (O'Higgins & Ruggles, 1981 and Ruggles & O’Higgins, 1981) § Chile’s 1996 fiscal system had equalizing regressive taxes (Engel et al., 1999) • Redistribu9ve Effect of Net Fiscal System (taxes and transfers together = 0.0583 (decline in Gini points) • Redistribu9ve Effect of System with Taxes only = -­‐ 0.0076 • Redistribu9ve Effect of System with Transfers but without Taxes = 0.0574 Ø Note that 0.0583 > 0.0574 § CEQ Assessments for Chile 2009 and South Africa 2010 show that regressive consump9on taxes are equalizing Nora Lus9g 40 Fiscal Policy and Inequality Four Key Ques/ons § Does the net fiscal system decrease inequality? § Is a par9cular tax or transfer equalizing or unequalizing? § What is the contribu9on of a par9cular tax or transfer (or any combina9on of them) to the change in inequality? § What is the inequality impact if one increases the size of a tax (transfer) or its progressivity? Nora Lus9g What is the contribu/on of a par/cular tax or transfer to the change in inequality? § Sequen9al method • May give the wrong answer to the “without vs. with comparison” because it ignores path dependency Ø Marginal contribu/on method (same for poverty) • Gives correct answer to the “without vs. with comparison” but does not fulfill the principle of aggrega9on: i.e., the sum of the marginal contribu9ons will not equal the total change in inequality (except by coincidence) § Average Contribu9on with all possible paths considered (Shapley value) • Fulfills the principle of aggrega9on, takes care of path dependency but the sign may be different from the marginal contribu9on => problema9c? 42 Nora Lus9g Calcula/ng the Marginal Contribu/on of a Tax The$marginal$contribution$of$a$tax$is$defined$as$ ! !!"!! = !!!! − !!!!!! ! $ Where!!!!! ,$!!!!!! $and!!are$the$Gini$coefficient$of$ income$with$the$transfer$but$without$the$tax$and$the$Gini$ coefficient$with$the$transfer$and$with$the$tax,$respectively$ $ If$!"!! >!0,!remember,$the$tax$is$equalizing$ Nora Lus9g 43 Sequen/al vs. Marginal Contribu/on Why the sequen/al method can be misleading Chile’s 1996 fiscal system (Engel et al., 1999) § Sequen9al contribu9on method: -­‐0.0076 § Marginal contribu9on method: 0.009 Nora Lus9g 44 Fiscal Policy and Inequality Four Key Ques/ons § Does the net fiscal system decrease inequality? § Is a par9cular tax or transfer equalizing or unequalizing? § What is the contribu9on of a par9cular tax or transfer (or any combina9on of them) to the change in inequality? § What is the inequality impact if one increases the size of a tax (transfer) or its progressivity? Nora Lus9g Progressivity vs. Size of Interven/on: A System with One Tax and One Transfer • In a system with one tax and one transfer: MC = G T X +B − G X −T + B = ... = g KT + b K B 1− g + b b − 1+ b K B • Geung the par9al deriva9ves: ∂ MC T (1 + b) K T + b K B = 2 ∂g (1− g +b) ∂ MC T g = ∂ KT 1− g + b Nora Lus9g 46 Next Steps: Path Dependency § Shapley Value § Where the Shapley value is the weighted average of all posible cases so that we can demostrate the effect of adding one source to the value func9on Nora Lus9g 47 Next Steps: Relaxing Assump/ons § Reranking: individuals can swap posi9ons in the post-­‐fiscal income ordering; true of all systems in the real world § No dominance: post-­‐fiscal Lorenz curve crosses the pre-­‐fiscal Lorenz curve; norma9ve parameter must be explicitly introduced (will not be covered today) § Different pre-­‐fiscal (original) distribu/ons: comparing the inequality-­‐ and poverty-­‐reducing capacity of fiscal systems across countries and over 9me (will not be covered today) Nora Lus9g 48 Methodological Highlights: Poverty and Impoverishment Based on Higgins & Lus9g (2015) Can a poverty-­‐reducing and progressive tax and transfer system hurt the poor? ECINEQ Working Paper No. 363, April. Nora Lus9g Main messages 3. Analyzing the impact on inequality only can be misleading Ø Fiscal systems can be equalizing but poverty increasing Lus9g (2015a and b) 50 Higgins & Lus9g (2015) 51 Main messages 4. Analyzing the impact on tradi9onal poverty indicators can be misleading Ø Fiscal systems can show a reduc9on in poverty for all possible poverty lines and yet a substan9al share of the poor could have been impoverished by the combined effect of taxes and transfers Higgins & Lus9g (2015) 52 Higgins and Lus9g, 2015 Higgins & Lus9g (2015) 53 Higgins & Lus9g (2015) 54 Higgins & Lus9g (2015) 55 Higgins & Lus9g (2015) 56 57 Higgins & Lus9g (2015) Nora Lus9g 58 Higgins & Lus9g (2015) 59 Main messages: summing up Ø To determine whether a fiscal interven9on is equalizing or not, one must assess its contribu9on with the other interven9ons in place Ø A regressive tax, for example, can exert an equalizing force that is over and above a system without that regressive tax Ø To measure the size of the contribu9on, use the marginal contribu9on method but remember that adding the marginal contribu9ons will not be equal to the total change Ø The impact of a tax on inequality and poverty can go in opposite direc9ons: e.g., equalizing and poverty increasing Ø An important propor9on of the poor may be lev poorer (in cash) by the fiscal system, and current measures may not alert us to this: new measure of fiscal impoverishment does 60 Lus9g, Enami and Aranda, forthcoming; Higgins & Lus9g (2015) Methodological Highlights: Fiscal Incidence Analysis in the (current) Commitment to Equity Assessments Based on Lus9g, Nora and Sean Higgins. 2013 Commitment to Equity Assessment (CEQ): Es9ma9ng the Incidence of Social Spending, Subsidies andTaxes. Handbook. CEQ Working Paper No. 1, Center for Inter-­‐American Policy and Research and Department of Economics, Tulane University, New Orleans, Lousiana and Inter-­‐American Dialogue, Washington, DC, Revised, September. Nora Lus9g CEQ Assessment: Method § Relies on state-­‐of-­‐the art tax and benefit incidence analysis • Ongoing consulta9on with experts to improve economic incidence es9mates § Uses conven9onal and newly developed indicators to assess progressivity, pro-­‐poorness and effec9veness of taxes and transfers § Allows to iden9fy the contribu9on of individual fiscal interven9ons to equity and poverty reduc9on objec9ves Lus9g & Higgins (2013) 62 CEQ Assessment: Fiscal Incidence Analysis Income aler taxes and transfers Taxes Transfers Yh = Ih -­‐ ∑i TiSih + ∑j BjSjh Income before taxes and transfers Lus9g & Higgins (2013) Share of tax i paid by unit h Share of transfer j received by unit h 63 CEQ Assessment: Fiscal Interven/ons • Currently included: – Direct taxes – Direct cash transfers – Non-­‐cash direct transfers such as school uniforms and breakfast – Contribu9ons to pensions and social insurance systems – Indirect taxes on consump9on – Indirect subsidies – In-­‐kind transfers such as spending on educa9on and health • Working on: – Corporate taxes – Housing subsidies Lus9g & Higgins (2013) 64 CEQ Assessment: Income Concepts MARKET INCOME PLUS DIRECT TRANSFERS MINUS DIRECT TAXES DISPOSABLE INCOME PLUS INDIRECT SUBSIDIES MINUS INDIRECT TAXES POST-­‐FISCAL or CONSUMABLE INCOME PLUS MONETIZED VALUE OF PUBLIC SERVICES: EDUCATION & HEALTH Lus9g & Higgins (2013) FINAL INCOME 65 Fiscal Incidence in CEQ Assessments § Accoun9ng approach • no behavioral responses • no general equilibrium effects and • no intertemporal effects • but it incorporates assump9ons to obtain economic incidence (not statutory) § Point-­‐in-­‐9me § Mainly average incidence; a few cases with marginal incidence Lus9g & Higgins (2013) 66 Fiscal Incidence in CEQ Assessments § Comprehensive standard fiscal incidence analysis of current systems: direct personal and indirect taxes (no corporate taxes); cash and in-­‐kind transfers (public services); indirect subsidies § Harmonized defini9ons and methodological approaches to facilitate cross-­‐country comparisons § Uses income/consump9on per capita as the welfare indicator § Allocators vary => full transparency in the method used for each category, tax shiving assump9ons, tax evasion § Secondary sources are used to a minimum Lus9g & Higgins (2013) 67 Alloca/on Methods § Direct Iden9fica9on in microdata § However, results must be checked: how realis9c are they? § If informa9on not directly available in microdata, then: § Simula9on § Imputa9on § Inference § Predic9on § Alternate Survey § Secondary Sources Lus9g & Higgins (2013) 68 Tax Shiling Assump/ons • Economic burden of direct personal income taxes is borne by the recipient of income • Burden of payroll and social security taxes is assumed to fall en9rely on workers • Consump9on taxes are assumed to be shived forward to consumers. • These assump9ons are strong because they imply that labor supply is perfectly inelas9c and that consumers have perfectly inelas9c demand • In prac9ce, they provide a reasonable approxima9on (with important excep9ons such as when examining effect of VAT reforms), and they are commonly used Lus9g & Higgins (2013) 69 Tax Evasion Assump/ons: Case Specific § Income taxes and contribu9ons to SS: § Individuals who do not par9cipate in the contributory social security system are assumed not to pay them § Consump9on taxes § Place of purchase: informal markets are assumed not to charge them § Some country teams assumed small towns in rural areas do not to pay them Lus9g & Higgins (2013) 70 Mone/zing in-­‐kind transfers § Incidence of public spending on educa9on and health followed so-­‐ called “benefit or expenditure incidence” or the “government cost” approach. § In essence, we use per beneficiary input costs obtained from administra9ve data as the measure of average benefits. § This approach amounts to asking the following ques9on: Ø How much would the income of a household have to be increased if it had to pay for the free or subsidized public service at the full cost to the government? Lus9g & Higgins (2013) 71 Treatment of Contributory Social Insurance Pensions • Deferred income in actuarially fair systems: pensions included in market income and contribu9ons treated as mandatory savings • Government transfer: pensions included among direct transfers and contribu9ons treated as a direct tax Lus9g & Higgins (2013) 72 Indicators § Inequality and poverty: • Gini, Theil, Kuznetz ra9os, ineq of opportunity • Headcount, poverty gap, squared poverty gap (interna9onal and na9onal poverty lines) • Impoverishment and fiscal mobility • Inequality of Opportunity § Effec9veness and Efficiency • Change in inequality or poverty divided by corresponding budget share or total spent • Poverty-­‐reduc9on efficiency indicators • Tax produc9vity indicators Lus9g & Higgins (2013) 73 Indicators § Progressivity • Incidence by quan9le or income group • Concentra9on Shares • Concentra9on Curves • Concentra9on Coefficients, Kakwani, and Reynolds-­‐Smolensky Index § Marginal contribu9ons and their deriva9ves § Ver9cal Equity and Reranking Effects Lus9g & Higgins (2013) 74 Indicators § Measuring Contribu9on to Redistribu9on and Poverty-­‐ reduc9on • Classifying interven9ons by whether they are equalizing or unequalizing • Classifying interven9ons by whether they are epoverty increasing or poverty reducing • Ranking interven9ons by their marginal contribu9on to changes in inequality • Ranking interven9ons by their marginal contribu9on to changes in poverty Lus9g & Higgins (2013) 75 Indicators § Coverage of social programs by quan9le and income group § Average per capita transfer received by the poor § Share of benefits going to the nonpoor § Average per capita transfer received by the nonpoor § Gross and net enrollment indicators by income group Lus9g & Higgins (2013) 76 Scenarios and Robustness Checks § Benchmark scenario § Sensi9vity to: • Changing the original income by which hh are ranked: e.g., market income plus contributory pensions and disposable income • Using consump9on vs. income • Per capita vs. equivalized income or consump9on • Different assump9ons on scaling-­‐down or up • Different assump9ons on take-­‐up of transfers and tax shiving and evasion • Alterna9ve valua9ons of in-­‐kind services • Other sensi9vity scenarios: country-­‐specific Lus9g & Higgins (2013) 77 Robustness Check Example from South Africa: Income vs. Consump/on-­‐based Analysis South Africa Gini estimates Market income Disposable income Post-fiscal income Final income Lus9g & Higgins (2013) Income based scenario 0.771 0.704 0.700 0.601 Consumption based scenario 0.723 0.634 0.628 0.514 78 Fiscal Policy, Inequality and Poverty in Middle Income Countries: Brazil, Chile, Colombia, Indonesia, Mexico, Peru and South Africa Lus9g, Nora. 2015b. “Fiscal Policy and Income Redistribu9on in Brazil, Chile, Colombia, Indonesia, Mexico, Peru and South Africa.” Chapter 7, Sec9on 7.3 in OECD In It Together. Why Less Inequality Benefits All. Cita/ons by country: (Year of Survey; C=consump/on & I=income) (Master Workbook, MWB, Version #) 1. 2. 3. 4. 5. 6. Armenia (2011; I): Stephen Younger and Artsvi Khachatryan (March 12, 2014) Bolivia (2009; I): Paz Arauco, Verónica, George Gray Molina, Wilson Jiménez Pozo, and Ernesto Yáñez Aguilar. 2014. “Explaining Low Redistribu9ve Impact in Bolivia.” In Lus9g, Nora, Carola Pessino and John Sco}. 2014. Editors. The Redistribu4ve Impact of Taxes and Social Spending in La4n America. Special Issue. Public Finance Review, May, Volume 42, Issue 3. (September 22, 2014) Brazil (2009; I): Higgins, Sean and Claudiney Pereira. 2014. “The Effects of Brazil’s Taxa9on and Social Spending on the Distribu9on of Household Income.” In Lus9g, Nora, Carola Pessino and John Sco}. 2014. Editors. The Redistribu4ve Impact of Taxes and Social Spending in La4n America. Special Issue. Public Finance Review, May, Volume 42, Issue 3. (November 4, 2014) Chile (2009, I): Ruiz-­‐Tagle, Jaime and Dante Contreras. 2014. CEQ Masterworkbook, Tulane University (August 27, 2014) Colombia (2010, I): Melendez, Marcela and Nora Lus9g. 2014. CEQ Masterworkbook, Tulane University (November 21, 2014) Costa Rica (2010; I): Sauma, Juan and Diego Trejos. 2014. Social Public Spending, Taxes, Redistribu4on of Income, and Poverty in Costa. CEQ Working Paper No. 18, Center for Inter-­‐American Policy and Research and Department of Economics, Tulane University and Inter-­‐American Dialogue, January. (February 2014) 80 7. 8. 9. 10. 11. 12. El Salvador (2011; I): Beneke, Margarita, Nora Lus9g y José Andrés Oliva. 2015. El impacto de los impuestos y el gasto social en la desigualdad y la pobreza en El Salvador. CEQ Working Paper No. 26, Center for Inter-­‐American Policy and Research and Department of Economics, Tulane University and Inter-­‐American Dialogue, February. (March 11, 2014) Ethiopia (2010/11; C): Tassew Woldehanna, Ruth Hill, Gabriela Inchauste, EyasuTsehaye, and Nora Lus9g. 2014. Chapter 5, Ethiopia Poverty Assessment, World Bank (April 30, 2014) Guatemala (2011; I): Cabrera, Maynor, Nora Lus9g and Hilcías Morán. 2014. Fiscal Policy, Inequality and the Ethnic Divide in Guatemala. CEQ Working Paper No. 20, Center for Inter-­‐American Policy and Research and Department of Economics, Tulane University and Inter-­‐American Dialogue, October. (April 13, 2014) Indonesia (2012; C) : Jon Jellema and Ma}hew Wai-­‐Poi. 2014. CEQ Master Workbook, Tulane University and The World Bank (February 18, 2014) Mexico (2010; I):Sco}, John. 2014. “Redistribu9ve Impact and Efficiency of Mexico’s Fiscal System.” In Lus9g, Nora, Carola Pessino and John Sco}. 2014. Editors. The Redistribu4ve Impact of Taxes and Social Spending in La4n America. Special Issue. Public Finance Review, May, Volume 42, Issue 3. (September 2013) Peru (2009; I): Jaramillo, Miguel. 2014. “The Incidence of Social Spending and Taxes in Peru.” In Lus9g, Nora, Carola Pessino and John Sco}. 2014. Editors. The Redistribu4ve Impact of Taxes and Social Spending in La4n America. Special Issue. Public Finance Review, May, Volume 42, Issue 3. (May 1, 2013) 81 13. 14. 15. South Africa (2010; I): Inchauste, Gabriela, Nora Lus9g, Mashekwa Maboshe, Catriona Purfield and Ingrid Wollard. 2015. The Distribu4onal Impact of Fiscal Policy in South Africa. Policy Research Working Paper 7194, The World Bank, February. (May 5, 2014) United States (2011; I): Higgins, Sean, Nora Lus9g, Whitney Ruble and Timothy Smeeding (forthcoming) Comparing the Incidence of Taxes and Social Spending in Brazil and the United States, Review of Income and Wealth Uruguay (2009; I): Bucheli, Marisa, Nora Lus9g, Máximo Rossi, and Florencia Amábile. 2014. “Social Spending, Taxes and Income Redistribu9on in Uruguay.” In Lus9g, Nora, Carola Pessino and John Sco}. 2014. Editors. The Redistribu4ve Impact of Taxes and Social Spending in La4n America. Special Issue. Public Finance Review, May, Volume 42, Issue 3. (August 18, 2014) 82 Household Surveys Used in Country Studies 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. 11. 12. 13. 14. 15. Armenia: Integrated Living Condi9ons Survey, 2011 (I) Bolivia: Encuesta de Hogares, 2009 (I) Brazil: Pesquisa de Orçamentos Familiares, 2009 (I) Chile: Encuesta de Caracterización Social (CASEN), 2009 (I) Colombia: Encuesta de Calidad de Vida, 2010 (I) Costa Rica: Encuesta Nacional de Hogares, 2010 (I) Ecuador: Encuesta Nacional de Ingresos y Gastos de los Hogares Urbano y Rural, 2011-­‐2012 (I) El Salvador: Encuesta De Hogares De Propositos Mul9ples, 2011 (I) Ethiopia: Ethiopia Household Consump9on Expediture Survey and Ethiopia Welfare Monitoring survey, 2011 (C) Guatemala: Encuesta Nacional de Ingresos y Gastos Familiares, 2010 (I) Indonesia: Survei Sosial-­‐Ekonomi Nasional, 2012 (C) Mexico: Encuesta Nacional de Ingreso y Gasto de los Hogares, 2010 (I) Peru: Encuesta Nacional de Hogares, 2009 (I) South Africa: Income and Expenditure Survey and Na9onal Income Dynamics Study, 2010-­‐2011 (I) Uruguay: Encuesta Con9nua de Hogares, 2009 (I) Note: The le}ers "I" and "C" indicate that the study used income or consump9on data, respec9vely. 83 Figure 1: Size and composition of government budgets (circa 2010) Panel a: Composition of Social Spending as a Share of GDP (rankedNbyNsocialNspending/GDP) 30.0% 20,000 18,000 16,000 14,000 12,000 10,000 8,000 6,000 4,000 2,000 0 25.0% 20.0% 15.0% 10.0% DirectNTransfers Education Health ContributoryNPensions OtherNSocialNSpending OECD Seven Countries Brazil(2009) South Africa***(2010) Mexico(2010) Colombia(2010) Peru(2009) Indonesia*(2012) 0.0% Chile**(2009) 5.0% GNINperNcapitaN(2011NPPP) 84 Panel b: Composition of Total Government Revenues as a Share of GDP (rankedJbyJtotalJgovernmentJrevenue/GDP) 60.00% 20,000 18,000 16,000 14,000 12,000 10,000 8,000 6,000 4,000 2,000 0 50.00% 40.00% 30.00% 20.00% DirectJTaxes IndirectJandJOtherJTaxes OtherJRevenues GNIJperJcapitaJ(2011JPPP) Brazil(2009) South Africa***(2010) Peru(2009) Mexico(2010) Chile**(2009) Indonesia*(2012) 0.00% Colombia(2010) 10.00% SocialJSecurityJContributions 85 0.8000 0.2000 0.7000 0.6000 0.1500 0.5000 0.4000 0.1000 0.3000 Market'Income'Gini Redistributive'Effect:'Market'to'Disposable Redistributive Effect: Brazil, Chile, Colombia, Indonesia, Mexico, Peru, South Africa, EU and the United States (Change in Gini Points: Market to Disposable Income; circa 2010) 0.2000 0.0500 0.1000 0.0000 0.0000 Pension1as1Market1Income Pension1as1Transfer Market1Income1Gini,1Pensions1Mkt1Inc Market1Income1Gini,1Pensions1as1Transf 86 Redistributive Effect from Market to Post-Fiscal AND Marginal Contributions by Fiscal Component 0.0900% 0.0789% 0.0800% 0.0700% 0.0600% 0.0500% 0.0446% 0.0370% 0.0400% 0.0308% 0.0300% 0.0151% 0.0200% 0.0100% 0.0073% 0.0061% Colombia% Indonesia**% 0.0000% Brazil% Chile*% Mexico%% Peru%% SA***% ,0.0100% Direct%taxes% Direct%transfers% Indirect%taxes% Indirect%subsidies% RedistribuJve%Effect% 87 Table&4:&Marginal&Contribution&of&Taxes&and&Transfers&(circa&2010) (Pensions&as&Market&Income) Brazil Chile* Colombia Indonesia** Mexico& Peru& SA*** Average Redistributive&Effect 0.0453 0.0340 0.0075 0.0044 0.0236 0.0099 0.0788 0.0291 Direct2taxes 0.0148 0.0154 0.0018 6 0.0131 0.0055 0.0269 0.0129 Direct2transfers 0.0320 0.0190 0.0057 0.0044 0.0109 0.0045 0.0593 0.0194 Redistributive&Effect 0.0446 0.0370 0.0073 0.0061 0.0308 0.0151 0.0789 0.0314 Direct2taxes 0.0171 0.0179 0.0019 6 0.0140 0.0060 0.0311 0.0147 Direct2transfers 0.0382 0.0220 0.0057 0.0043 0.0113 0.0048 0.0711 0.0225 Indirect2taxes 60.0014 0.0027 60.0017 60.0028 0.0027 0.0052 0.0000 0.0007 Indirect2subsidies 0.0008 0.0004 0.0015 0.0052 0.0047 6 6 0.0025 Direct2taxes 0.1738 0.3481 0.1373 0.0000 0.2411 0.3853 0.1109 0.1995 Direct2transfers2 0.5310 0.9064 0.9233 0.6248 0.7931 0.9612 1.0165 0.8223 Indirect2taxes 60.0536 60.0172 60.1986 60.0513 0.0129 0.0527 60.0788 60.0477 Indirect2subsidies 0.8295 0.7978 0.5034 0.0645 0.2457 0.0000 0.0000 0.3487 Marginal&Contributions From&Market&to&Disposable&Income From&Market&&to&PostLfiscal&Income Kakwani 88 Fiscal Policy and Poverty Reduction (circa 2010) (Change in Headcount Ratio from Market to Post-fiscal Income for Pensions in Market Income and Pensions in Transfers; in %) a 15.0% 10.0% 5.0% 0.0% !5.0% !10.0% !15.0% !20.0% !25.0% !30.0% !35.0% Brazil/(2009) Colombia (2010) Indonesia* (2012) Peru/(2009) Mexico/(2010) South/Africa** (2010) Pensions/as/Market/Income Chile*** (2009) Pensions/as/Transfer 89 Net Payers to the Fiscal System (circa 2010) Panel a: Pensions as Market Income NetBReceivers NetBPayers Indonesia*(2012) Chile**(2009) Colombia(2010) Mexico(2010) Peru(2009) South Africa***(2010) Brazil(2009) y<1.25 1.25<=y<2.5 2.5<=y<4 4<=y<10 10<=y<50 y>=50 90 0'''''''''''Cumulative'share'of'income'and'transfers'''''''''''1' Progressivity+of+Transfers:+A+Diagrammatic+Representation! ! Globally'progressive'transfer'in'absolute'terms' ! (pro5poor):'per'capita'benefit'declines'with'pre5 transfer'income'(not'necessarily'everywhere)'' ! Concentration*Curve*lies*above*the*diagonal* ! Concentration*Coefficient*<*0* ! ! Kakwani*Index*>*0* ! * Globally'progressive'transfer:'benefit'as'a'share'of' pre5transfer'income'declines'with'income'(not' ! necessarily'everywhere)' Concentration*Curve*lies*above*pre>transfers**Lorenz* ! curve* ! ! Concentration*Coefficient*<*Gini*for*pre>transfer* income* ! ! Kakwani*Index*>*0* Transfer'neutral'in'absolute'terms:'per'capita' benefit'is'equal'for'everyone.' Concentration*Curve*coincides*with*the* diagonal* ! Concentration*Coefficient*=*0* ! Kakwani**>*0* Pre5transfer'Lorenz' curve ! ! Proportional'transfer:'benefit'as'a' share'of'pre5transfer'income'is'the' ! same'for'everyone' Concentration*Curve*coincides*with* ! the*pre>transfer*Lorenz*curve* ! Concentration*Coefficient*=*Gini* ! for*pre>transfer*income* ! Kakwani*Index*=*0* ! ! Globally'regressive'transfer:'benefit'as'a'share'of' pre5transfer'income'increases'with'income'(not' necessarily'everywhere)' Concentration*Curve*lies*below*market*income* Lorenz*curve* ! Concentration*Coefficient*>*Gini*for*pre> transfer*income* ! Kakwani*Index*<*0* * ! 0'''''Cumulative'share'of'population'(ordered'by'market'income)'''''''''''''''' ' ! '''1' 91 Progressivity and Pro-poorness of Education and Health Spending. Summary of Results Educ&Total Pre$school Pro$poor&CC&is& Same&per& Progressive&CC& Pro$poor&CC&is& Same&per& negative capita&for&al ;& positive&but& negative capita&for&al ;& CC&=0 lower&than& CC&=0 market& income&Gini Primary Progressive&CC& Pro$poor&CC&is& Same&per& positive&but& negative capita&for&al ;& lower&than& CC&=0 market& income&Gini Brazil&(2009) + + + &Chile&(2009) + + + Colombia&(2010) + + + Indonesia&(2012) + na + Mexico&(2010) + + + Peru&(2009) + + + South&Africa&(2010) + + + *CC&is&almost&equal&to&market&income&Gini&coefficient If&the&Concentration&Coefficient&is&higher&or&equal&to&$0.5&but&not&higher&than&0.5,&it&was&considered&equal&to&0. Secondary Progressive&CC& Pro$poor&CC&is& Same&per& positive&but& negative capita&for&al ;& lower&than& CC&=0 market& income&Gini + + + Tertiary Progressive&CC& Pro$poor&CC&is& Same&per& positive&but& negative capita&for&al ;& lower&than& CC&=0 market& income&Gini Health Progressive&CC& Regressive&CC& Pro$poor&CC&is& Same&per& positive&but& positive&AND& negative capita&for&al ;& lower&than& higher&than& CC&=0 market& market& income&Gini income&Gini + + + + + + + + + + + + + + Progressive&CC& positive&but& lower&than& market& income&Gini + + + + 92 Figure 4. Redistribution and social spending, 2010 0.2000 0.1800 ZAF RestributiveCEffect 0.1600 0.1400 BRA 0.1200 CHL 0.1000 MEX 0.0800 0.0600 COL 0.0400 IDN 0.0200 0.0000 0.0% 5.0% PER 10.0% 15.0% 20.0% 25.0% 30.0% SocialCSpending 93 A. Redistribution and market income inequality 0.2000 0.1800 ZAF 0.1600 RedistribuiveDEffect 0.1400 BRA CHL 0.1200 0.1000 MEX 0.0800 0.0600 0.0400 0.0200 PER COL IDN 0.0000 0.3800 0.4300 0.4800 0.5300 0.5800 0.6300 0.6800 0.7300 0.7800 0.8300 GiniDMarketDIncome 94 B. Final income inequality and market income inequality 0.60 ZAF 0.55 Gini<Final<Income COL 0.50 PER 0.45 MEX BRA CHL 0.40 IDN 0.35 0.38 0.43 0.48 0.53 0.58 0.63 0.68 0.73 0.78 0.83 Gini<Market<Income 95 Fiscal Policy, Inequality and Poverty in Low Income Countries: Ethiopia Based on: Lus9g, Nora. 2015a. “The Redistribu9ve Impact of Government Spending on Educa9on and Health Evidence from Thirteen Developing Countries.” Chapter 17 in Inequality and the Role of Fiscal Policy: Trends and Policy Op9ons, edited by Benedict Clements, Ruud de Mooij, Sanjeev Gupta, and Michael Keen (Washington: Interna9onal Monetary Fund, forthcoming) World Bank. 2014. Ethiopia. Poverty Assessment, Chapter 5. (Based on CEQ Assessment for Ethiopia) Primary'and'Social'Spending/GDP'vs'GNI/capita 45%$ BRA$ 40%$ BOL$ 35%$ ZAF$ 30%$ URY$ AMR$ PER$ 25%$ 20%$ ZAF$ SLV$ COL$ 15%$ ETH$ 10%$ SLV$ ETH$ 5%$ GTM$ IND$ BOL$ GTM$ MEX$ CHL$ BRA$$ URY$ PER$ AMR$ IND$ MEX$ COL$ CHL$ 0%$ 0$ 2000$ Source: Lus9g (2015a) 4000$ 6000$ 8000$ 10000$ 12000$ 14000$ 16000$ 18000$ 20000$ GNI/Capita$(2011$PPP) Primary$Spending/GDP$ Social$Spending/GDP$ 97 CEQ Assessment for Ethiopia (World Bank, 2014, Ch. 5) 98 In Ethiopia, post-­‐fiscal poverty is higher than pre-­‐fisc poverty even when using the official US $1.24 (daily ppp) moderate poverty (black line) Ethiopia: Headcount Ra/os 50% 45% Source: Lus9g (2015a) 40% 35% 30% 25% 20% 15% 10% 5% 0% Market Income Net Market Income Source: World Bank (2014) Na9onal Moderate PL $1.24 PPP Disposable Income Post-­‐fiscal Income Na9onal Extreme PL $0.65 PPP 99 However, except for the boyom 10 percent, all deciles are neutral (2nd) or net payers to the fisc… Ethiopia: Net Payers to the Fiscal System Start at Decile... 0.15 0.10 0.05 0.00 0 1 2 3 4 5 6 7 8 9 10 -­‐0.05 -­‐0.10 -­‐0.15 Source: Lus9g (2015a) 100 Except for the boyom income category (<US$1.25/day), the rest are net payers to the fisc… Ethiopia: Net Payers to the Fiscal System Start at Income Category... 0.05 0.00 y < 1.25 1.25 < = y < 2.50 2.50 <= y < 4.00 4.00 <= y < 10.00 10.00 <= y < 50.00 50.00 <= y -­‐0.05 -­‐0.10 -­‐0.15 -­‐0.20 Source: Lus9g (2015a) -­‐0.25 101 Note that Net Indirect Taxes can be equalizing and yet poverty increasing: Ethiopia Change'in'Gini:'Marginal'Contribu2on'of'Net'Indirect' Taxes' Change'in'Headcount'Ra0o'($2.5'PPP/Day):'Marginal'Contribu0on'from'Net'Indirect'Taxes''' Gu a 8%% 6%% 4%% 2%% 0.045% 0.026% 0.036% 0%% &2%% 0.006% &0.015% &0.007% 0.006% &0.012% &0.016% &0.024% &4%% 0.012% 0.006% &0.002% &0.019% &0.028% &6%% &8%% &0.072% ContribuUon%from%Net%Indirect%Taxes% Change%in%Headcount:%Post&Fiscal%vs%Mkt% Bo l Lan te m al a (2 ivi 01 a( 0) 2 00 %% In do 9) %% ne Sr sia(2 i %L an 012 k ) %% Co a(2 00 lo m 9) bi % a El % Sa (201 lva 0) Pe dor % %( 2 ru (2 01 00 1) Et 9) %% hi % % op ia( Co 20 st a%R 11)% ic Jo rd a(20 an 10 (2 01 )%% M ex 0) ico %% ( 2 Ar 0 1 m en 0)%% i Ur a(20 ug 11 ua ) %% y( Br az 200 9) il( %% 2 Ch 009 ) %% ile (2 00 So u t 9)% h% A ia(2 012 ) %% ka( 200 9)% Per u(2 009 )% Co l om bia (20 10) % Gu ate ma la(2 010 Co s ) %% ta%R ica (20 10) Chi %% le(2 009 )% E l %S alv ado r%(2 011 Jor ) %% dan (20 10) %% Me xi c o (2 010 ) %% Bol ivia (20 09) %% Arm eni a(2 011 ) %% Uru gua y(2 009 ) %% Bra zil( 200 9)% S ou th% Afr ica (20 10) %% (in%GINI%points) Sri% nes Ind o Eth i op ia(2 011 )% (in%percentage%points)%% 0.01% 0.00% !0.01% !0.02% !0.03% !0.04% !0.05% !0.06% !0.07% !0.08% !0.09% ContribuUon%from%Net%Indirect%Tax% Gini%Change:%Post!fiscal%vs%Mkt% Source: Lus9g (2015a) 102 Pro-­‐poorness of Educa/on Spending Primary Pro$poor&CC&is& Same&per& negative capita&for&all;& CC&=0 Armenia&(2011) Bolivia&(2009) Brazil&(2009) &Chile&(2009) Colombia&(2010) El&Salvador&(2011) Ethiopia&(2011) Guatemala&(2010) Indonesia&(2012) Mexico&(2010) Peru&(2009) South&Africa&(2010) Uruguay&(2009) Source: Lus9g (2015a) + + + + + + Secondary Progressive&CC& Pro$poor&CC&is& Same&per& positive&but& negative capita&for&all;& lower&than& CC&=0 market& income&Gini + + + + + Progressive&CC& positive&but& lower&than& market& income&Gini + + + + + + + + + + Regressive&CC& positive&AND& higher&than& market& income&Gini + + + + + +* + + + + + + + + Tertiary Progressive&CC& Pro$poor&CC&is& Same&per& positive&but& negative capita&for&all;& lower&than& CC&=0 market& income&Gini + + + +* 103 Pro-­‐poorness of Health Spending Health Pro$poor&CC&is& Same&per& negative capita&for&all;& CC&=0 Source: Lus9g (2015a) Armenia&(2011) Bolivia&(2009) Brazil&(2009) &Chile&(2009) Colombia&(2010) El&Salvador&(2011) Ethiopia&(2011) Guatemala&(2010) Indonesia&(2012) Mexico&(2010) Peru&(2009) South&Africa&(2010) Uruguay&(2009) Progressive&CC& positive&but& lower&than& market& income&Gini + + + + + + + + + + + + + 104 • • • • • References Duclos, Jean-­‐Yves and Abdelkrim Araar. 2007. Poverty and Equity: Measurement, Policy and Es4ma4on with DAD (Vol. 2). Springer. Chapters 7 and 8. (available online) Higgins, Sean and Nora Lus9g. 2015. Can a poverty-­‐reducing and progressive tax and transfer system hurt the poor? ECINEQ Working Paper No. 363, April. Lambert, Peter J. (2001). The Distribu4on and Redistribu4on of Income: A Mathema4cal Analysis. Manchester University Press. Third Edi9on. Chapter 11. (not available online) Lus9g, Nora, Ali Enami and Rodrigo Aranda. “The Analy9cs of Fiscal Redistribu9on.” Chapter in Lus9g, Nora and Sean Higgins, editors, Commitment to Equity Handbook: Es9ma9ng the Redistribu9ve Impact of Fiscal Policy. (Forthcoming) Lus9g, Nora and Sean Higgins. 2013 Commitment to Equity Assessment (CEQ): Es9ma9ng the Incidence of Social Spending, Subsidies andTaxes. Handbook. CEQ Working Paper No. 1, Center for Inter-­‐American Policy and Research and Department of Economics, Tulane University, New Orleans, Lousiana and Inter-­‐American Dialogue, Washington, DC, Revised, September. § Lus9g, Nora. 2015a. “The Redistribu9ve Impact of Government Spending on Educa9on and Health Evidence from Thirteen Developing Countries.” Chapter 17 in Inequality and the Role of Fiscal Policy: Trends and Policy Op9ons, edited by Benedict Clements, Ruud de Mooij, Sanjeev Gupta, and Michael Keen (Washington: Interna9onal Monetary Fund, forthcoming) § Lus9g, Nora. 2015b. “Fiscal Policy and Income Redistribu9on in Brazil, Chile, Colombia, Indonesia, Mexico, Peru and South Africa.” Chapter 7, Sec9on 7.3 in OECD In It Together. Why Less Inequality Benefits All. § World Bank. 2014. Ethiopia. Poverty Assessment, Chapter 5. (Based on CEQ Assessment for Ethiopia) 105 Thank you! 106